Companies

-

Back to the Future

Roger Montgomery

October 17, 2012

By Russell Muldoon and Roger Montgomery

Growing up in inner Melbourne in the 1970’s I cannot tell you how many post hockey-game lunches my mother trotted out on the ‘Breville’. The original scissor action Breville Sandwich Toaster was released in 1974. It sold 400,000 in its first year and reached 10% of Australian households. It was quickly improved in 1976 with the release of the Breville Snack’n’Sandwich Toaster (pictured) which was the first sandwich toaster to cut and seal sandwiches in half. It was a revelation and became an icon of the appliance world – we could eat a sandwich while riding our BMX’s without the contents of the sandwich spilling everywhere. And Mum was happy because a healthy and warm lunch was done in a few minutes and while it was being made, she could get the carpet sweeper out and do a quick run up and down the hallway or throw a slipper at any kid that was mucking up because they were hungry!

by Roger Montgomery Posted in Companies, Manufacturing.

- 6 Comments

- save this article

- POSTED IN Companies, Manufacturing

-

Iluka confirms all our fears…

Roger Montgomery

October 16, 2012

Didn’t think a free blog could be a valuable use of your time?

Back on 13 July 2012 (read here), we warned that Iluka Resources announced their 2012-2014 Key Physical and Financial Guidance previously released in February 2012 was “now redundant and as such no longer applicable”. Management had said volumes for the December 2012 half-year were indicating “lower ordering patterns or an unwillingness to commit to volumes except on an “as needed” basis”.

As with other miners described here at the blog over the last year, the boom appeared to be over and reports were confirming our earlier appraisal of the likely impact from a China – led slowdown. Iluka’s exposure is both direct and indirect and the grim conditions were confirmed yesterday with the release of the Iuka Resources September Quarterly report. Combined sales volumes of zircon, rutile, synthetic rutile and ilmenite at 306,300 tonnes, were down 29% on the September Quarter 2011. Revenue at $225m was down an extraordinary 58% from $533m recorded in the September Quarter 2011. This means the average selling price for Iluka’s mineral sands declined by 41% year on year. In response, the Iluka share price fell 6.6% to $9.00 and is back to trading where it was in February 2011. Essential reading indeed.

by Roger Montgomery Posted in Companies, Insightful Insights.

- 3 Comments

- save this article

- POSTED IN Companies, Insightful Insights

-

When genius fails?

Roger Montgomery

October 15, 2012

CVC has wrestled with its ownership of Nine ever since it bought the network from James Packer’s PBL Media for $5.3 billion in 2007. And now CVC’s man Adrian McKenzie has quit the nine board and Goldman Sachs as swapped debt for equity.

Equity owners are last in line and its a salient lesson for investors who must always remember that there is a very high risk owning businesses. In this environment of low interest rates its easy to value companies on equally low discount rates to try and produce a valuation close to the current price to justify a purchase. This is the basic lesson for CVC.

Even in an environment such as this we’d be using 10%, 11% even 13% required returns and walking away from anything that is not cheap enough.

With money burning holes in pockets and fees based on the employment of capital the temptation to bit off more than one can chew is ever present.

The late Kerry Packer taught the world a valuable lesson when he said ‘You only get one Alan Bond’. And James was obviously paying attention.

by Roger Montgomery Posted in Companies, Media Companies.

- 4 Comments

- save this article

- POSTED IN Companies, Media Companies

-

MEDIA

What are Tim Kelley’s insights into the Australian Banks?

Tim Kelley

October 10, 2012

Do Ten Network (TEN), Seven West Media (SWM), Aurora Oil (AUT), Origin Energy (ORG), Santos (STO), Cedar Woods (CWP), Slater and Gordon (SGH), IMF (IMF), Roce Oil (ROC), The Reject Shop (TRS), Challenger (CGF), Bluescope (BSL) or Adelaide Brighton (ABC) achieve the coveted A1 grade? Watch this edition of Sky Business’ Your Money Your Call 10 October 2012 program now to find out, and also hear Tim’s thoughts on the big Aussie banks. Watch here.

by Tim Kelley Posted in Companies, Financial Services, Insightful Insights, TV Appearances.

-

What is your best performing stock pick for the next 9 months?

Roger Montgomery

October 5, 2012

September was a challenging month for investors but Montgomery chalked up another outperformance in both The Montgomery [Private] Fund and The Montgomery Fund (see figure 1).

Of course in the short term the performance of share prices can be attributed to noise and randomness and so the bigger question is always; which businesses will be worth substantially more in the future?

What is your suggestion for the best performing stock for the next nine months to June 30, 2012?

Pick the best performing stock in the next nine months and gain fame and notoriety, kudos and credit.

Each month we’ll track the list and present the table until June 30, 2012.

All the best and stay tuned.

by Roger Montgomery Posted in Companies, Intrinsic Value, Investing Education.

-

WHITEPAPER

THE PROPERTY RUG PULL

Discover how proposed changes to negative gearing, Capital Gains Tax and holiday home tax rules could reshape property investing, and why investors may consider private credit as property returns become less certain and tax advantages diminish.

READ HERE -

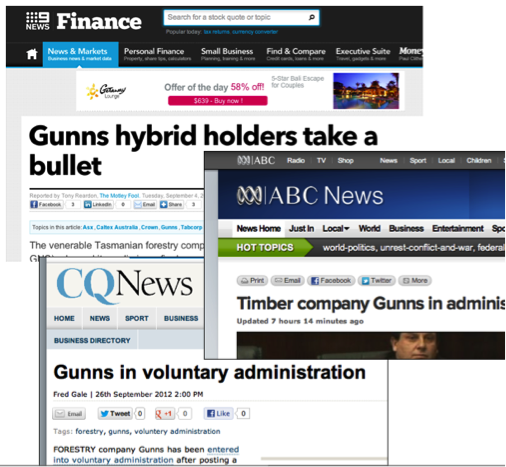

Gunns collapse. If only they’d been Skaffold members!

Roger Montgomery

September 29, 2012

Chalk up another win for Skaffold members.

Substantial capital losses are difficult to make back and irrespective of whether you are still in accumulation mode, retiring or retired it is essential to avoid major losses. One way to do this of course is to diversify and ensure that losses are mitigated through position sizing. Another technique and the one we will discuss here, is to simply avoid the companies most likely to collapse.

This week Gunns (ASX:GNS), was placed into voluntary administration and happily for Skaffold members it is unlikely that anyone owned shares.

Gunn’s was never investment grade. Anyone who purchased the stock from 2003 onwards were taking a massive risk and Skaffold can explain why.

Skaffold’s Verdict (Figure. 1) is a picture of danger.

by Roger Montgomery Posted in Companies, Insightful Insights, Market Valuation, Skaffold, Value.able.

-

MEDIA

What are Tim Kelley’s insights into Cabcharge’s prospects?

Roger Montgomery

September 25, 2012

Do Sedgman (SMD), Decmil Group (DCG), cochlear (COH), Seek (SEK), IAG (IAG), Resolute Mining (RSG), Magellan Financial Group (MFG), Syrah Resources (SYR), ASG (ASZ), Goodman Group (GMG), Silex Systems (SLX), AMP (AMP) or Service Stream (SSM) achieve Roger’s and Tim’s coveted A1 grade? Watch this edition of Sky Business’ Your Money Your Call broadcast 25 September 2012 program now to find out, and also learn Tim’s insights to the outlook for Cabcharge (CAB). Watch here.

by Roger Montgomery Posted in Companies, TV Appearances.

- save this article

- POSTED IN Companies, TV Appearances

-

David Jones: Non retailers distracted by a takeover?

Roger Montgomery

September 21, 2012

This week David Jones announced their 2012 results and reported a 40% decline in profit. The only positive was that 4th quarter sales fell by just 1% on pcp whereas 1st quarter sales had fallen 11% on pcp. Actually there was another positive; the 35% decline in earnings per share was inline with expectations.

Separately the company also provided an update to its property strategy. Investors should understand that anything DJS does with its properties is simply a takeover defence against private equity (or Premier Investments perhaps) pulling off the same stunt that was done on Myer. That is; launch a takeover, succeed, sell off the property portfolio and get the business cheaper. if DJS shows it is proactive in this area it becomes much harder from Private Equity to argue that they are “adding value”.

DJS intrinsic value (see Fig. 1) has now not increased since 2004 and according to Skaffold.com DJS’s intrinsic value is not expected to rise at all over the next two years.

by Roger Montgomery Posted in Companies, Insightful Insights, Intrinsic Value, Takeovers.

-

MEDIA

What are David Buckland’s insights into the future of Australian retail?

Roger Montgomery

September 20, 2012

Do Silex Systems (SLX), Condor Blanco Mines (CDB), Codan (CDA), Webjet (WEB), Tasman Resources (TAS), M2 Telecommunications (MTU), Magellan (MPG), Iluka Resources (ILU), Arrium (ARI), TPG (TPM), ASG Group (ASZ), Incitec Pivot (IPL) and Sirius Resources (SIR) and achieve the Montgomery coveted A1 grade? Watch this edition of Sky Business’ Your Money Your Call broadcast 20 September 2012 now to find out, and also learn David’s insights into the issues facing Australian retail. Watch here.

by Roger Montgomery Posted in Companies, TV Appearances.

- save this article

- POSTED IN Companies, TV Appearances

-

If Only They Had Skaffold

Roger Montgomery

September 20, 2012

Notch up another win for investors who use Skaffold. Back in August last year I was asked by a viewer on Sky Business what I thought of MacMahon Holdings (ASX:MAH).

Notch up another win for investors who use Skaffold. Back in August last year I was asked by a viewer on Sky Business what I thought of MacMahon Holdings (ASX:MAH).You can watch the video here at 5 mins 20 seconds.

When asked the question, I looked at Skaffold.com and noting the very small change in intrinsic value over many years I said “This business is not going to deliver sustainable long-term outperformance”.

Today’s near-40% share price decline, announcement of a cost blowout, a downgrade to previous earnings guidance and the immediate resignation of the CEO Nick Bowen is a blow to those investors who own the shares of MacMahon and do not own Skaffold.

by Roger Montgomery Posted in Companies, Insightful Insights, Investing Education, Skaffold.