Property

-

Housing Bubble?

Roger Montgomery

April 15, 2015

My friends Ticky Fullerton and Michael Yanda at the ABC are running a three part series on Sydney’s property market. continue…

by Roger Montgomery Posted in Insightful Insights, Property.

- 2 Comments

- save this article

- POSTED IN Insightful Insights, Property

-

Should interest rates be lower?

Tim Kelley

April 9, 2015

The Reserve Bank of Australia (RBA) surprised the market this week by not lowering official interest rates. While the RBA statement did note that the Board would have a think about lowering rates in the period ahead, the market was pretty sure a cut was in the bag. As a result, a Tuesday morning rally in the equity market made a sudden about face when the news was released. continue…

by Tim Kelley Posted in Economics, Insightful Insights, Property.

- 3 Comments

- save this article

- POSTED IN Economics, Insightful Insights, Property

-

Dear Property Speculator…

Roger Montgomery

March 30, 2015

Concentrate. Money has a price. The price of money is the interest rate. Lower the price and demand increases. It’s the same with credit. The price of credit is the interest rate. Credit is money. Lower the price of credit and more people borrow. But there is a problem for central banks who like to use the price of money and credit as a tool for manipulating or fine tuning the economy. That problem is the bluntness of the tool. continue…

by Roger Montgomery Posted in Insightful Insights, Property.

- 12 Comments

- save this article

- POSTED IN Insightful Insights, Property

-

Missed the Property Boom?

Roger Montgomery

March 17, 2015

Global real estate agents are opening shop in China and becoming “gold digging” tour operators for wealthy Chinese to find and buy property around the world. continue…

by Roger Montgomery Posted in Insightful Insights, Property.

- 15 Comments

- save this article

- POSTED IN Insightful Insights, Property

-

Do Property Prices Ever Fall?

Roger Montgomery

February 11, 2015

It was December 14, 2011. The Australian Resource Boom was in full swing and the Pilbara was ground zero. In Port Hedland the median house price had almost doubled in four years from $600,000 in 2007 to more than $1 million, according to Real Estate Institute of WA figures. In Wedge Street, you needed plenty of ‘wedge’ – $995,000 to be exact – to buy a brand new ‘off the plan’ two-bedroom unit in a multilevel apartment complex.

by Roger Montgomery Posted in Energy / Resources, Insightful Insights, Property.

-

WHITEPAPER

THE PROPERTY RUG PULL

Discover how proposed changes to negative gearing, Capital Gains Tax and holiday home tax rules could reshape property investing, and why investors may consider private credit as property returns become less certain and tax advantages diminish.

READ HERE -

Is it time to look at mining services?

Tim Kelley

January 23, 2015

Among the biggest casualties of falling resources capex have been the various engineering, contracting and construction firms that provide services to the resources sector. Monadelphous (ASX: MND) is a case in point: With strong demand to fuel its growth, the Mondaelphous share price rose 50-fold in the decade leading up to 2012. Over the last few years however, a decline in earnings has seen the share price fall by around 70 per cent – a painful drop in any language. continue…

by Tim Kelley Posted in Energy / Resources, Insightful Insights, Property.

-

What captured your interest in Q2 2014?

Roger Montgomery

January 7, 2015

Over the next few days, we will take a look back at 2014 and highlight the most popular articles based on your views and comments.

The mention of house prices falling and negative gearing was a popular post.

In May, we talked Coca-Cola Amatil share price having declined by 40 per cent, and the duopoly that makes up Australia’s grocery retail landscape has putting the company on a strict diet of shrinking volumes, values and loss of market share to Schweppes and more particularly, the category known as “Private Label” soft drinks.

The forecast Australian population growth from 23 million to 40 million by 2060 bodes well for self-storage providers – and small-cap National Storage is no exception. We take a closer look at how the third-largest self-storage provider is positioned. Note, you will need to log in as a subscriber to see this paper.

by Roger Montgomery Posted in Consumer discretionary, Insightful Insights, Investing Education, Property, Value.able.

-

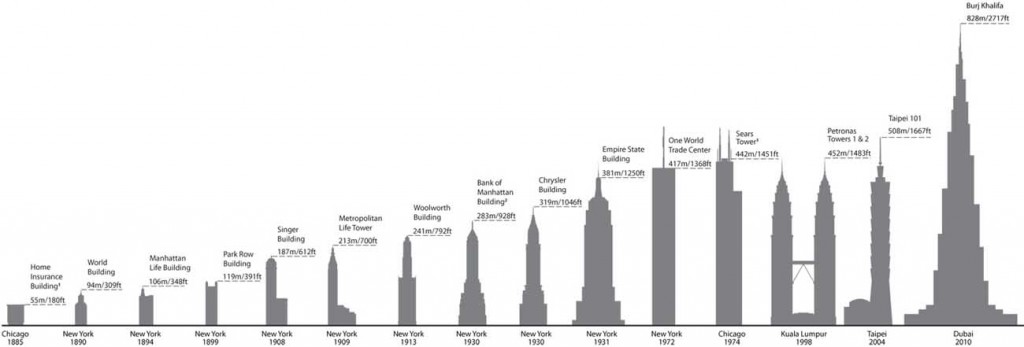

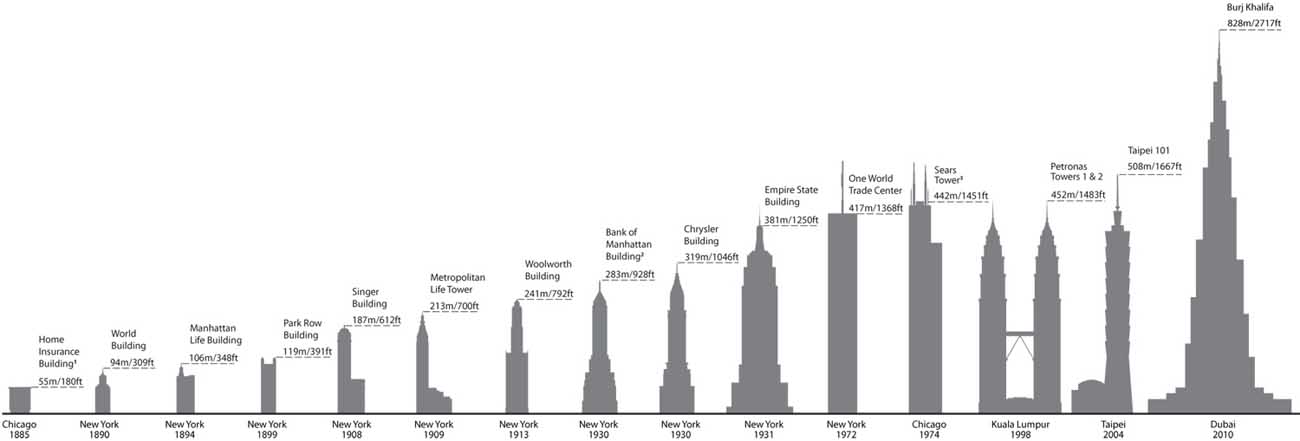

Bubble Watch #18 Tallest Buildings warns of impending stock market crash?

Roger Montgomery

December 7, 2014

There are all sorts of coincidences that can be mistaken for signs that a crash is imminent. We don’t put much store in those, however it is never uninteresting reading about them. One that is gaining a little traction is something known as the Edifice Complex.

In conventional terms, the Edifice Complex is the desire to build lasting edifices or buildings as a legacy to one’s greatness. In today’s context, the Edifice Complex represents the historically coincident construction/completion of these buildings with stock market crashes. continue…

by Roger Montgomery Posted in Insightful Insights, Property, Value.able.

- 3 Comments

- save this article

- POSTED IN Insightful Insights, Property, Value.able

-

Property; be careful! Equities; get ready!

Roger Montgomery

November 17, 2014

It doesn’t seem that long ago, but the Global Financial Crisis-inspired rout in the stock market began in late 2007 and even though it bottomed in March of 2009, the symptoms that triggered the collapse, are even worse today.

But before you go jumping at shadows keep in mind that while interest rates remain low, the status quo is very likely to be maintained. Indeed low or lower rates could trigger an equity bubble before any correction is experienced. continue…

by Roger Montgomery Posted in Economics, Insightful Insights, Investing Education, Property, Value.able.

-

Chinese property prices: it ain’t Sydney or Melbourne

Roger Montgomery

October 31, 2014

Hot on the heels of data showing GDP in China is growing at its slowest rates since the GFC, the Chinese property industry displayed signs of continuing deceleration. Housing sales have declined 10.8 per cent by value from a year earlier in the first nine months of 2014, and average city home prices declined 1.3 per cent in September – the first fall in nearly two years. continue…

by Roger Montgomery Posted in Insightful Insights, Property.

- save this article

- POSTED IN Insightful Insights, Property