Watching Hyperscaler debt

Many years ago, I was asked by an AFR journalist whether I would revise my valuation of ABC Learning Centres, which was a tiny fraction of the traded price at the time, given the Singaporean Sovereign Wealth Fund (Temasek) had just invested in the company’s then-latest capital raise at a much higher market valuation.

Full of youthful confidence, I responded: “stupid people live in all different countries.”

A familiar pattern of fundraising and deployment was playing out at ABC Learning. It was one I had seen before and one which often resulted in pear-shaped returns for equity investors. That was certainly the case at ABC, which subsequently blew up spectacularly.

When a company’s share price is high – usually because investors are excited about the company or the theme it’s exposed to, and the cost of equity is low, managers aggressively issue stock to raise funds. However, as conditions shift – often because the equity returns demanded are unrealistic, the business matures, growth slows, macro interest rates rise, or the share price drops – the cost of equity increases, prompting a strategic pivot to debt.

The corporate playbook is well documented in academic literature.

Back in 1984, Myers & Majluf’s Pecking Order Theory revealed that when a company stops issuing equity and switches to debt, it signals to the market that management believes the stock is no longer premium. This depresses the stock price.

In another study published in the Journal of Finance in 2006, How Persistent Is the Impact of Market Timing on Capital Structure?, the author looked closely at companies that timed the market by going public or raising massive equity during ‘hot’ market windows (when share prices were highly inflated). The research found that while these firms initially enjoyed very low leverage due to the influx of cheap equity, the effect completely reversed within two years. As the ‘hot’ equity market cooled and share prices deflated, these companies pivoted sharply to issuing debt rather than equity. Because they had over-expanded during the boom years, their subsequent rush into the debt markets quickly resulted in over-leveraged capital structures, increasing their risk of insolvency.

The playbook’s failure boils down to oft-seen simple steps:

- High share price – the firm issues cheap equity and expands aggressively

- Cost of capital rises – further share issues are too dilutive, so company switches to debt raises.

- If returns on equity decline/cash flows deteriorate, it collides with debt repayments. Meanwhile, any ability to save the company with further equity issues vaporises alongside the appetite for equity risk.

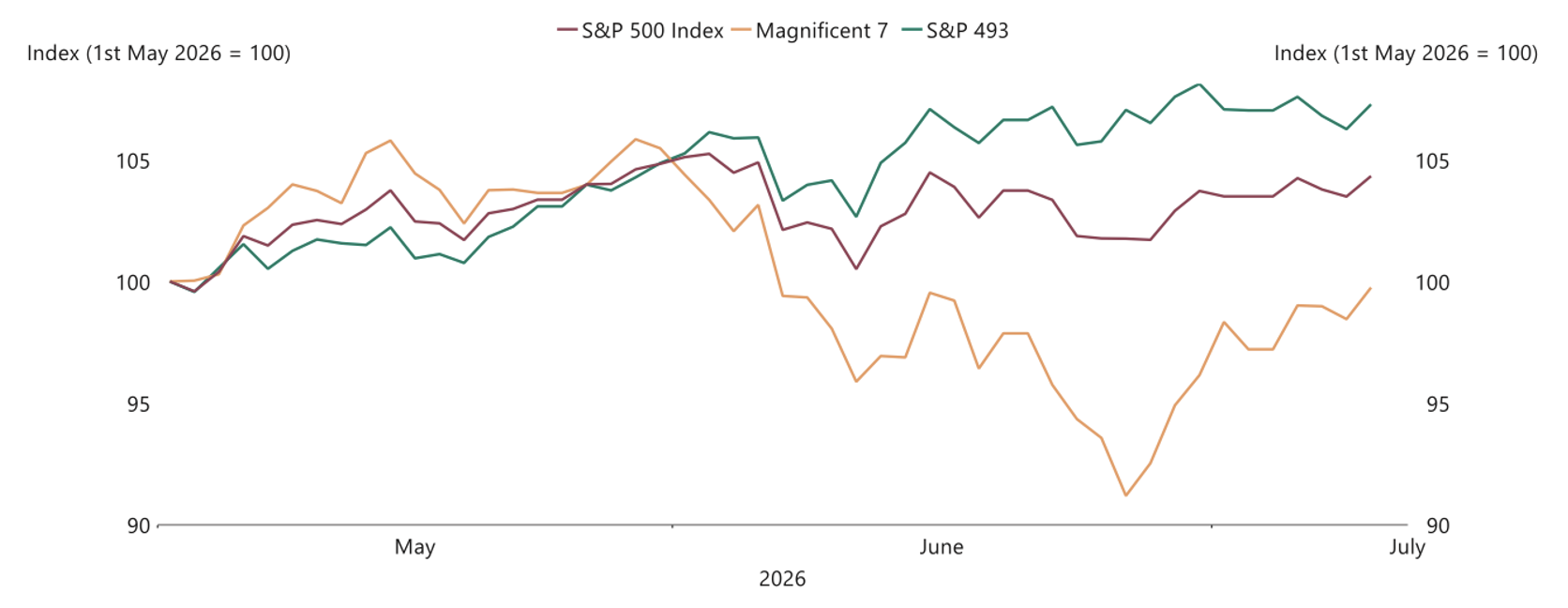

Figure 1. Magnificent Seven (Mag 7) stocks are underperforming (share price drop)

Source: Bloomberg, Macrobond, Apollo Chief Economist. Note: Bloomberg Magnificent 7 and Bloomberg 500 ex Mag 7 indices used

*Mag 7: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla.

A sentiment shift towards the artificial intelligence (AI) Hyperscalers is underway. This is reflected in the Mag 7’s relative underperformance since May 1, 2026.

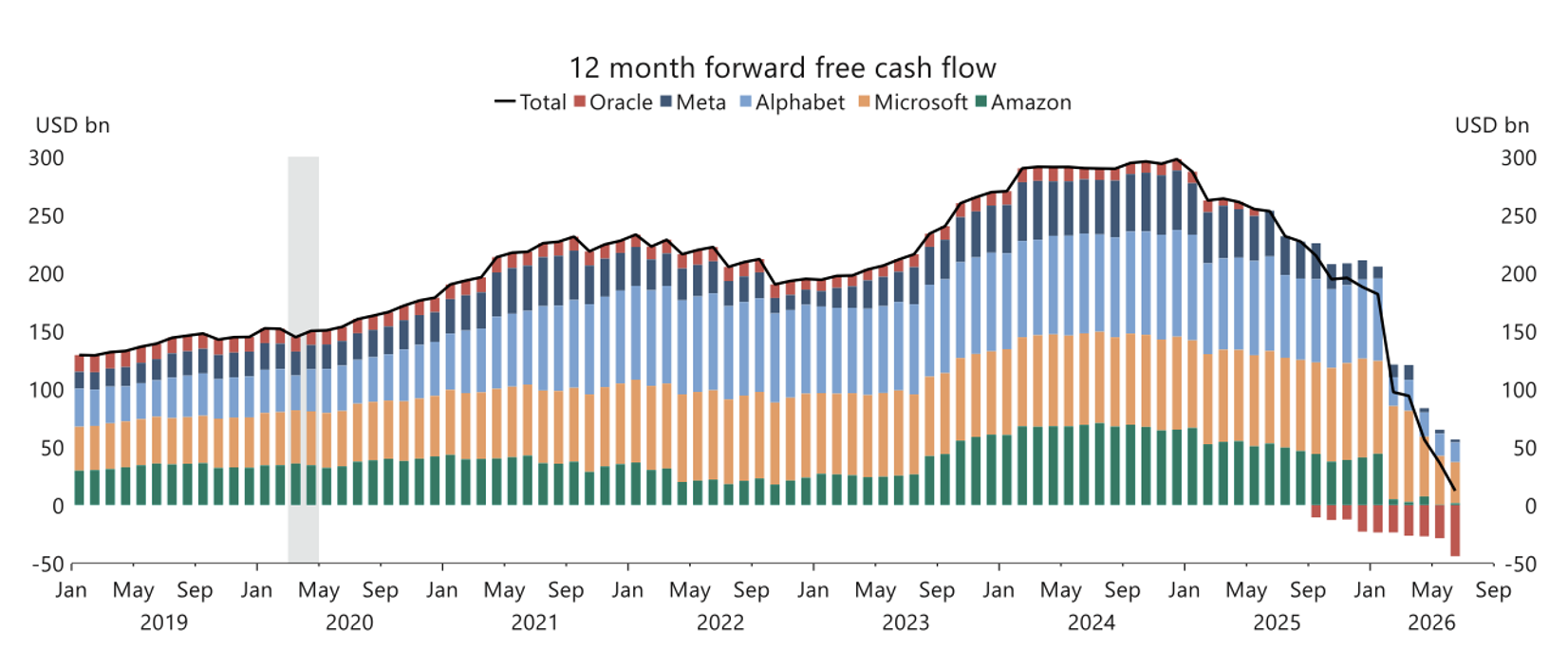

Meanwhile, the cash flows of the Hyperscalers is declining, some might say precipitously (note forecasts is that it will start rising again beyond 2027).

Figure 2. Falling Hyperscaler free cash flow

Source: Bloomberg, Macrobond, Apollo Chief Economist

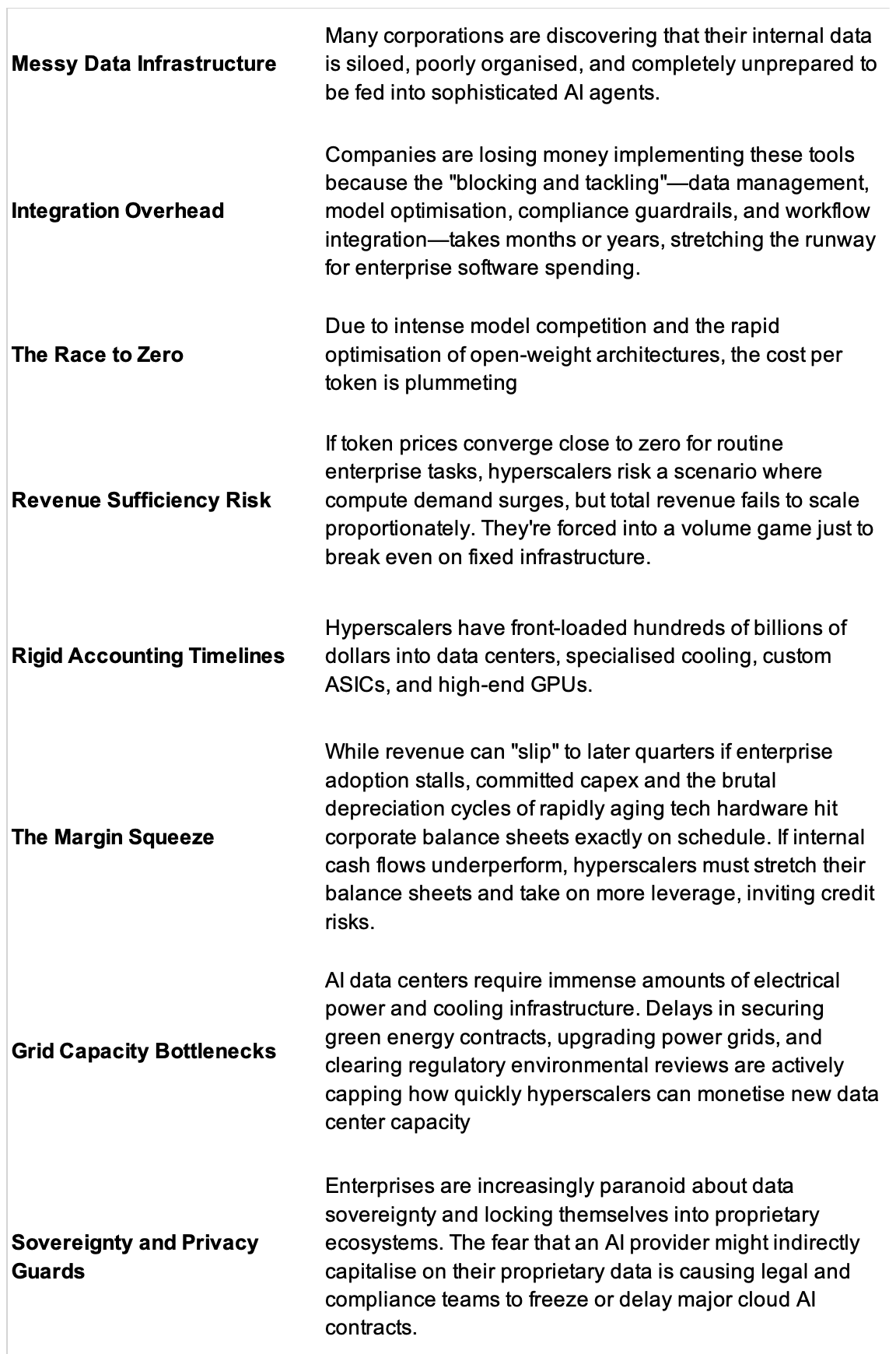

Token prices are declining and Chinese Large Language Models (LLMs) are gaining ground. If those trends continue, Hyperscaler cash flows will face ongoing pressures and analyst forecasts may prove too optimistic. So, if the payoff takes longer than investors are pricing in – which is entirely possible (see table below) – share prices will decline further, the cost of equity will rise, and the cost associated with the already-accumulated debt will collide with falling cash flows.

Table 1. Sources of possible delay for Hyperscaler payoffs

As an aside, because the broader stock market is heavily concentrated in the Mag 7 and allied tech infrastructure names, a material delay in the AI payoff wouldn’t just be an isolated tech sector issue. A prolonged revenue lag could trigger a market-wide equity re-rating, impacting chip manufacturers, energy grids, and eventually the wider economy.

In addition to index concentration, Hyperscaler leverage and bond issuance have also surged. While the AI hype-cycle was initially funded by a handful of mega tech companies and their own cash flows, Oracle, CoreWeave and other infrastructure players began borrowing to build the physical backbone of the AI boom through a rapidly expanding mountain of debt that some say is beginning to test the capacity of the investment-grade market.

Of course, just as the mounting debt initially began to worry investors back in May, Goldman Sachs issued a report about Agentic AI called, Decoding the Agentic Economy: The Coming Inflection in AI Usage and Margins, that returned market enthusiasm for the next wave of AI demand, which included estimates of monthly token usage rising toward 120 quadrillion tokens.

But that reality hasn’t manifested, not yet anyway, and meanwhile, share prices are underperforming and the mountain of debt remains.

Tick Tock, Tick Tock.

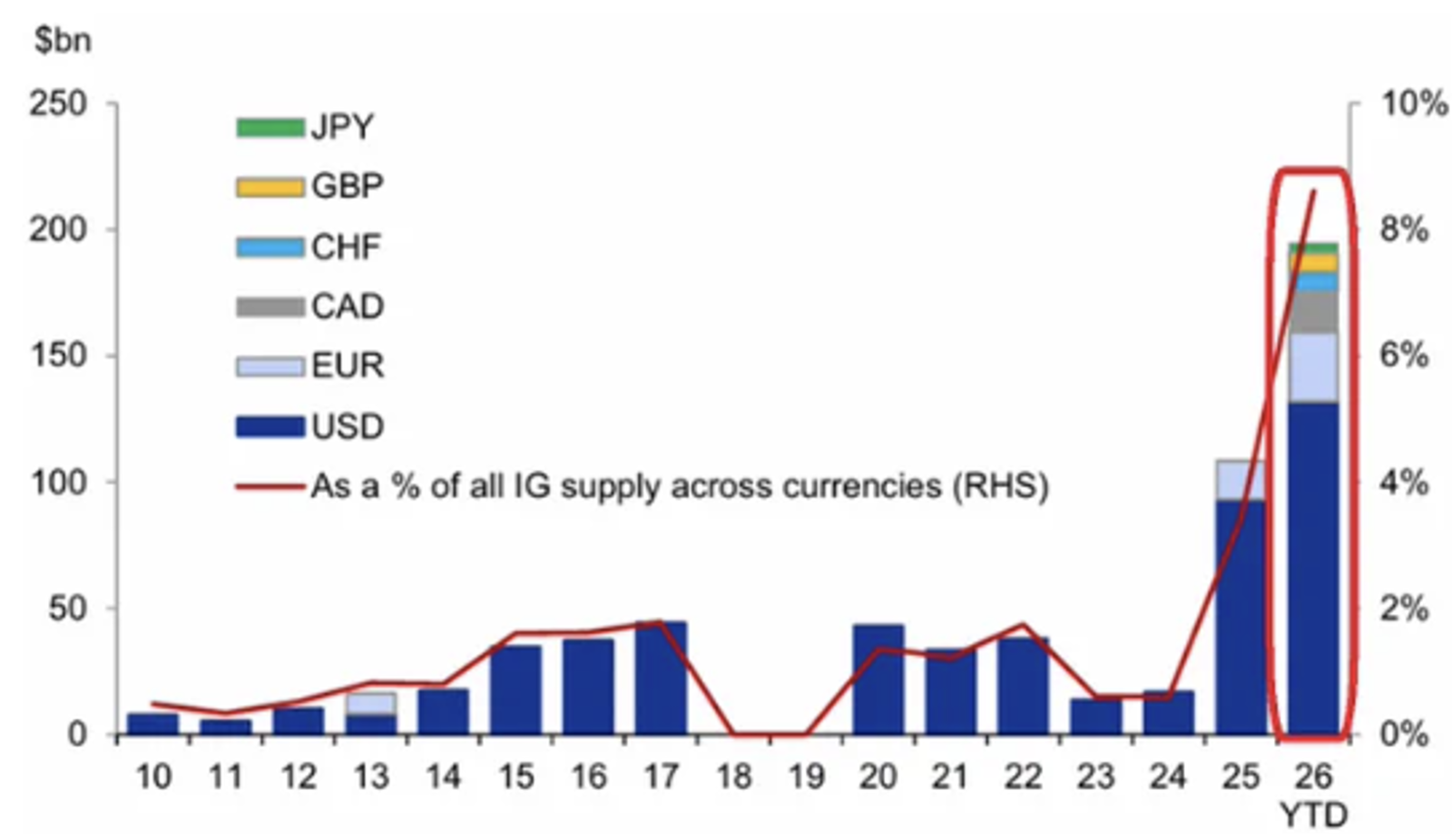

Figure 3. Hyperscaler debt issuance YTD (July 9, 2026). 9 per cent of investment grade supply

Source: Dealogic, Goldman Sachs

As Figure 3, shows, hyperscalers have issued US$194 billion in debt so far this year across currencies, already accounting for a record nine per cent of all U.S. investment-grade (IG) bond supply.

Notably, this share has quadrupled since 2022 and more than doubled in the last 12 months. And in terms of issuance, AI-related debt, which was one per cent of IG supply in 2024 has been 18 per cent of supply in the first half of 2026. It’s also worth noting the gross leverage of the hyperscalers has doubled from 0.9x to 1.8x in just the last six months and is now above the entire energy sector’s leverage.

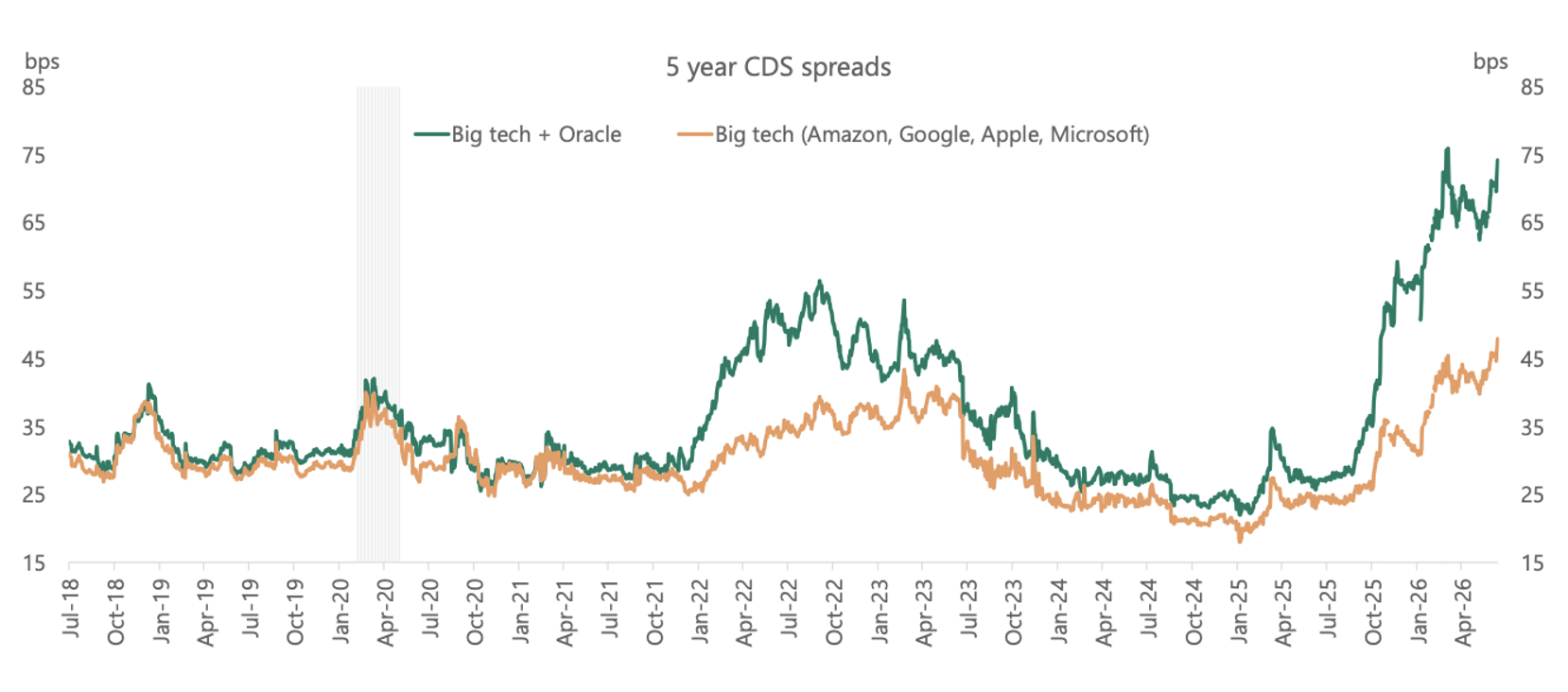

Perhaps understandably, as ‘Big Tech’ continues to issue debt to finance AI spending, the first cracks are appearing with investors seeking more protection against rising credit risk exposure, which is reflected in widening credit default swap spreads.

Figure 4. CDS spreads are widening.

Source: Bloomberg, Appollo Chief Economist

According to Apollo Global, 5-year credit default swap (CDS) spreads on hyperscalers have surged over +50 basis points since the start of 2025, to around 75 basis points. That’s about 20 basis points above levels seen during the 2022 bear market.

As one observer noted, “the AI CAPEX boom is increasingly fueled by debt, and credit markets are starting to push back.”

Conclusion

The AI boom has entered a critical phase. Hyperscalers aren’t just reinvesting cash flows – those have plunged. And as they spend more than they earn, they’re massively increasing leverage to maintain their lead in the AI-infrastructure race. But they’re building ‘on spec,’ banking on growing token demand and agentic AI revenues to justify the borrowing.

While credit investors are currently continuing to support the AI-spin-cycle, the quick doubling of leverage significantly increases the risk.

I’ve seen this playbook before.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.