Nothing to see here

According to the most bullish investors the current bull market bears little resemblance to the tech bubble of 1999/2000.

That late-90s tech bubble was fueled by a Fear of Missing Out (FOMO), which was reflected in the very high price-to-earnings (P/E) multiples. Today’s bull market is accompanied by much more reasonable valuations suggesting that the rally is merely reflecting an equally steep increase in real earnings.

In early 2000, the tech sector’s forward P/E ratio stood at 55 times, and the broader S&P500 rose to 25 times forward earnings; today, the S&P500 sits on a forward P/E of 20.5 times and the tech sector on 23 times.

The bulls suggest an earnings-driven rally (as reflected in modest P/E ratios) is inherently more sustainable than one built on expanding hope and P/Es.

But it’s worth noting no P/E level precludes a correction.

In 1987 (Black Monday), the forward P/E for the S&P 500 was around 15 times before the market crashed. In 2008 (the Global Financial Crisis), the forward P/E hovered around15 times, confirming the crisis originated from credit/leverage issues rather than pure stock overvaluations. More recently, in February 2020 (COVID-19), the forward P/E was around 19 times just prior to the pandemic sell-off. And, most recently, the 2022 Bear Market began with a forward P/E multiple of 22 times as central banks began to raise rates.

Despite today’s relatively modest P/E ratios compared to the 2000 Dot.Com bubble, there are many worried about an imminent correction.

How can they justify concerns when earnings expectations are rising at double-digit rates? The answer lies in the assumption that those bullish analyst forecasts are reasonable. What if the analysts’ earnings expectations are the heart of the problem? They are indeed extraordinarily bullish. Long-term earnings growth for the S&P 500 tech sector is currently running at a record 38 per cent per annum, eclipsing the 28.7 per cent peak seen during the dot-com boom.

Figure 1. The April 1999 Merrill’s report.

Source: Merrill Lynch

I am reminded of the report published by Merrill Lynch in April 1999. The analysts at ‘Merrills’, where I was working, wrote: “For several reasons, moreover, we believe that even when viewed through the lens of a more rigorous valuation framework, the stocks are worth more than the casual observer might think. These reasons include: 1) that no one knows with any degree of certainty what the future cash flows will be or what the real risk associated with them is (the leading companies have been blowing away expectations from the get-go); 2) the potential for unprecedented returns on invested capital, which will ultimately equate to higher P/E multiples, and 3) benefits from the “network effect,” through which franchises are made more valuable and sustainable with every new customer or supplier they add.”

One cannot help but wonder, whether the same optimism about artificial intelligence (AI) has infected today’s earnings forecasts – remembering these forecasts are the basis for the market’s current bullish condition.

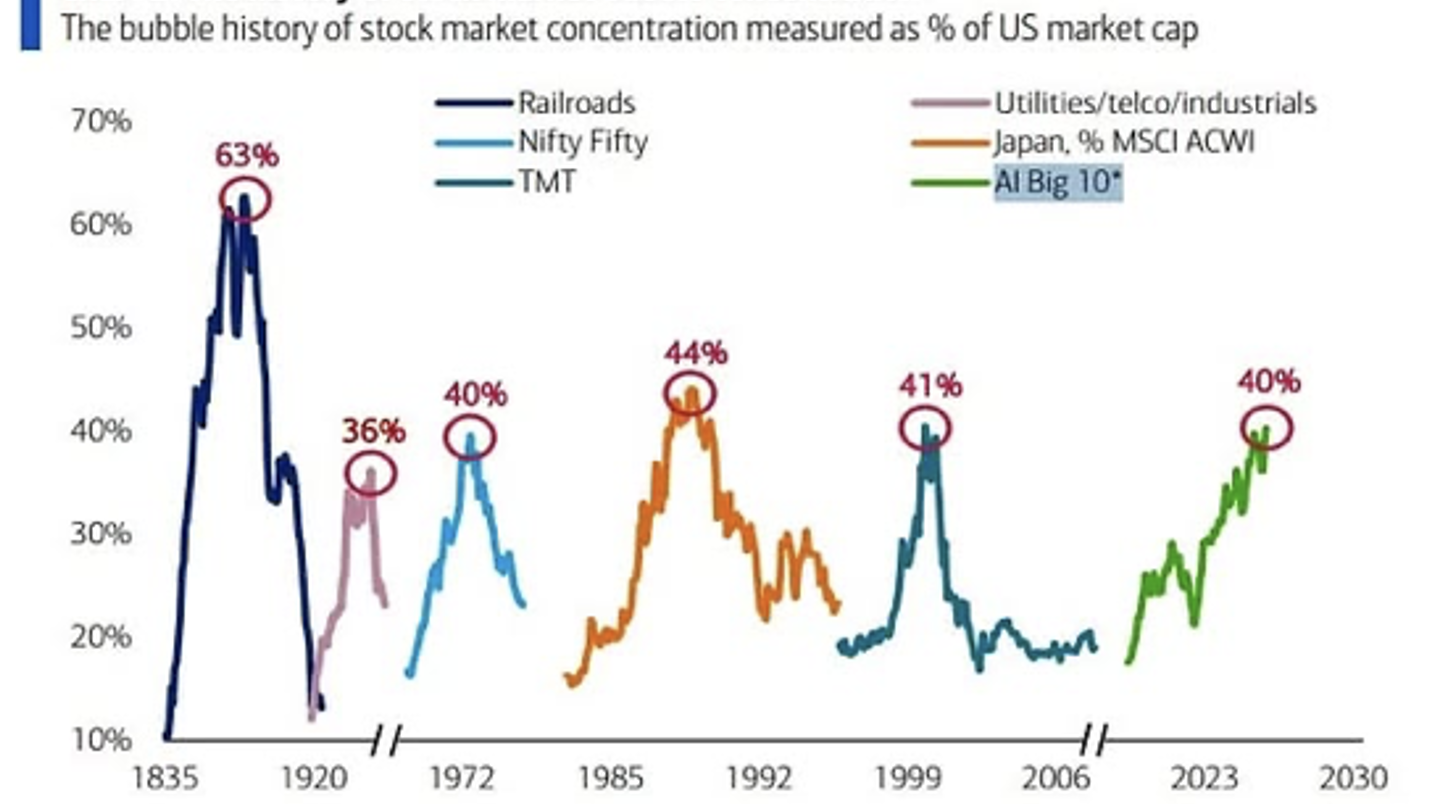

Technology and Communication Services now command a massive 47.2 per cent of the S&P 500’s total market cap. And while this level of concentration has often preceded past corrections (Figure 2), today it is said to be justified by the numbers: their combined share of the index’s ‘forward’ earnings is an equally impressive 43.8 per cent.

But remember that word again; “forward”. It’s an estimate.

Figure 2. History of stock market concentration

Source: BofA Global Investment Strategy, GFD Finaeon, Bloomberg. Note: Japan is measured as a % of MSCI ACWI, all others as % of US stock market. *AI Big 10 = Magnificent 7 + Broadcom, AMD, Micron.

Indeed, a peek under the hood reveals this potential blind spot. A significant portion of recent profits stems from paper gains rather than physical or organic operations. In Q1-2026, mark-to-market gains on equity investments in fellow AI companies accounted for:

- 58 per cent of Alphabet’s net profit

- 52 per cent of Amazon’s net profit

- 27 per cent of Nvidia’s net profit

In other words, Michael Burry’s web of circular financing among AI “hyperscalers” appears to be alive and well and raises valid questions about whether tech giants are artificially inflating one another’s bottom lines.

Beyond tech

The bulls dismiss this as nothing to worry about, noting that the market is no longer a one-trick pony. Even if the “Magnificent 7” (Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Telsa) face earnings-quality questions, the rest of the market – the other 493 stocks in the S&P 500 – has also seen accelerating earnings growth.

According to Yardeni Research, S&P 500 forward earnings-per-share (EPS) rose to US$368.91 last week, with 2027 earnings expected to reach US$399.25. That’s a record high for forward earnings. Meanwhile, S&P 600 SmallCap and S&P 400 MidCap forward earnings also have been rising at faster paces over the past year, to record highs.

Of course, it’s worth remembering that an earnings-quality-triggered sell-off in major AI companies could spread to the broader market. This is because much of the economy’s growth and improved productivity are tied to AI. A deterioration in the outlooks for AI companies could have much broader economic implications – something stock market investors and traders would be acutely attuned to.

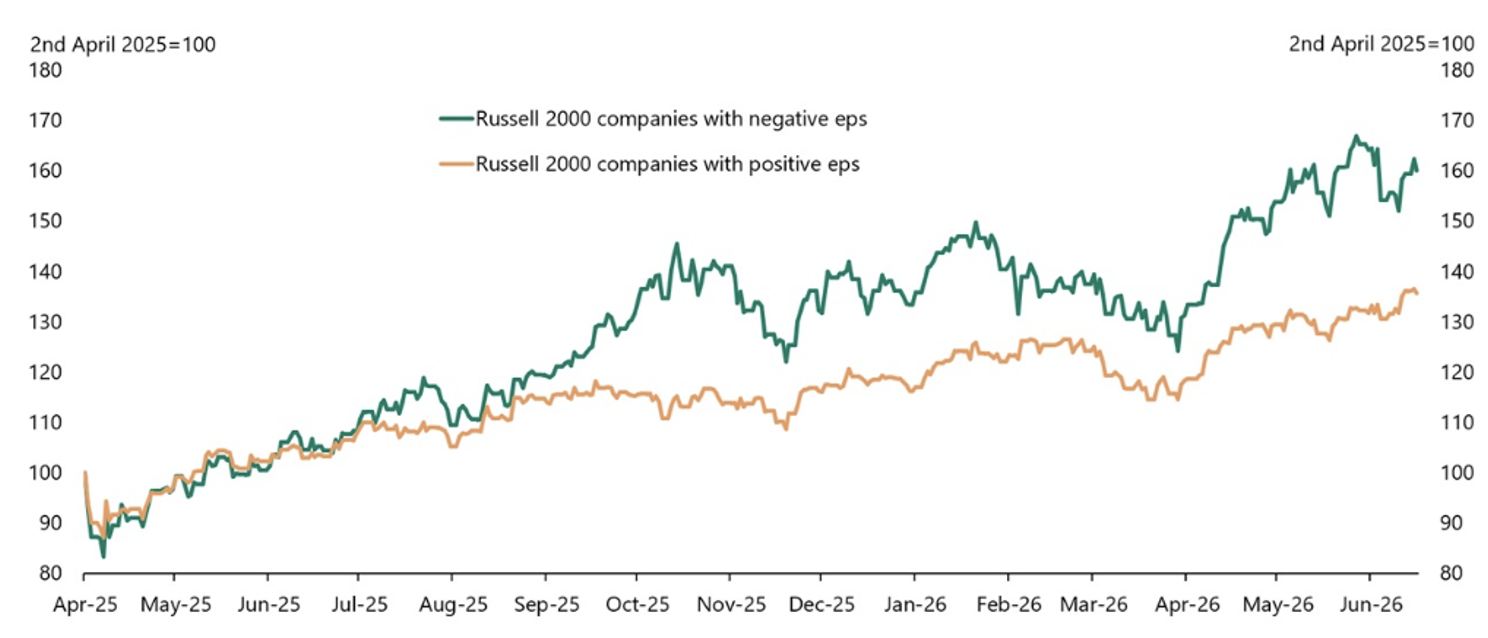

Elsewhere, Tortsen Slok, Apollo Global’s Chief Economist, noted on June 20, “Something is broken in price discovery when companies with negative earnings keep outperforming companies with positive earnings.”

Figure 3. Companies with negative earnings outperform those with positive earnings

Source: Bloomberg, Apollo Global

For all the talk of growing earnings, it’s the companies with no earnings that seem to be doing best – a sign, if there ever was one, of unbridled enthusiasm or irrational exuberance.

Whether it’s irrational or not, the bulls point to encouraging signs in all corners of the market. They note market sentiment, as measured by the AAII, is balanced, rather than overly bullish, while crude oil’s recent drop to US$79.85 a barrel promises to lower corporate input costs and fuel further earnings momentum. Elsewhere, Wall Street has quickly adjusted to the debut press conference of new Fed Chair Kevin Warsh, with the futures market now pricing in just one 25-basis-point rate hike over the next six months, and two over the next year.

And so it seems, the rally is supported by modest multiples and strong earnings growth; the earnings growth is broadening, inflation risks are declining – supporting further earnings growth – and rate rises are likely to be few and far between.

According to the bulls, there’s nothing to worry about, and investors should ‘back the truck up.’

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.