Is SpaceX burning up on re-entry?

I wonder whether there’s a more fundamental reason for SpaceX crashing 16 per cent overnight and 30 per cent since its June 16 high of US$225.64, beyond the headlines.

SpaceX (NASDAQ:SPCX) shares plunged roughly 16 per cent overnight after disclosing a massive US$20 billion bond offering to fund its artificial intelligence (AI) ambitions, amid growing dilution concerns stemming from a US$60 billion stock acquisition of the AI coding platform Cursor.

SpaceX has disclosed plans to sell US$20 billion in investment-grade senior unsecured bonds to repay bridge financing and fund its aggressive artificial intelligence ambitions.

Meanwhile, the company’s agreement to acquire Anysphere (the developer of the Cursor AI coding platform) for US$60 billion in stock will dilute existing stakes.

It’s worth noting that because approximately 96 per cent of SpaceX shares remain escrowed for now, the tiny 4 per cent of publicly traded stock has resulted in extreme price volatility. The small public float was designed to help push the price higher after the Initial Public Offering (IPO), especially when index funds are forced to buy, but it also magnifies any downward slides.

Table 1. SpaceX insider share sale timeline

| Milestone / Day | Allocation eligible to sell | Condition / Trigger |

| Q2 earnings release (Est. Mid-July to Sept 2026) | Up to 20 per cent of restricted shares | Triggers immediately following the release of SpaceX’s first post-IPO quarterly earnings. |

| Performance booster | An additional 10 per cent of shares | Unlocks early only if the stock trades >30 per cent above the IPO price for 5 out of 10 consecutive trading days following the Q2 earnings release. |

| Day 70 | 7 per cent of shares | Time-based tranche. |

| Day 90 | 7 per cent of shares | Time-based tranche. |

| Day 105 | 7 per cent of shares | Time-based tranche. |

| Day 120 | 7 per cent of shares | Time-based tranche. |

| Day 135 | 7 per cent of shares | Time-based tranche. |

| Q3 Earnings Release (Est. Mid-Oct to Dec 2026) | An additional 28 per cent of shares | Triggers immediately following the release of the Q3 earnings call. |

| Day 180 (Est. December 2026) | 100 per cent of remaining regular shares | Full expiry of the standard lock-up window for all regular shareholders and employees. |

| Day 366 (June 2027) | Elon Musk’s stake | The major unlock point where Musk’s non-milestone shares (~5.45 billion shares) become contractually eligible to sell. |

The timeline is measured from the June 11, 2026 prospectus date. It gradually releases chunks of equity into the market based on a mix of time, corporate earnings, and stock price performance:

Much of the investor focus has been on the IPO’s structure and the requirement for NASDAQ index funds to buy stock 15 days after the IPO. With less than five per cent of the company’s stock available the narrative has been that index buying will drive the shares higher.

The flipside, however, is the conga line of backers who have supported Musk since he purchased Twitter (now X) for US$44 billion in 2022. Twitter was subsequently ‘merged’ into xAI (the owner of Grok), which was then merged into SpaceX. The billionaire individuals and private equity firms that have been locked into X and xAI will soon have an opening to reduce their stake or even exit completely.

And why might they want to?

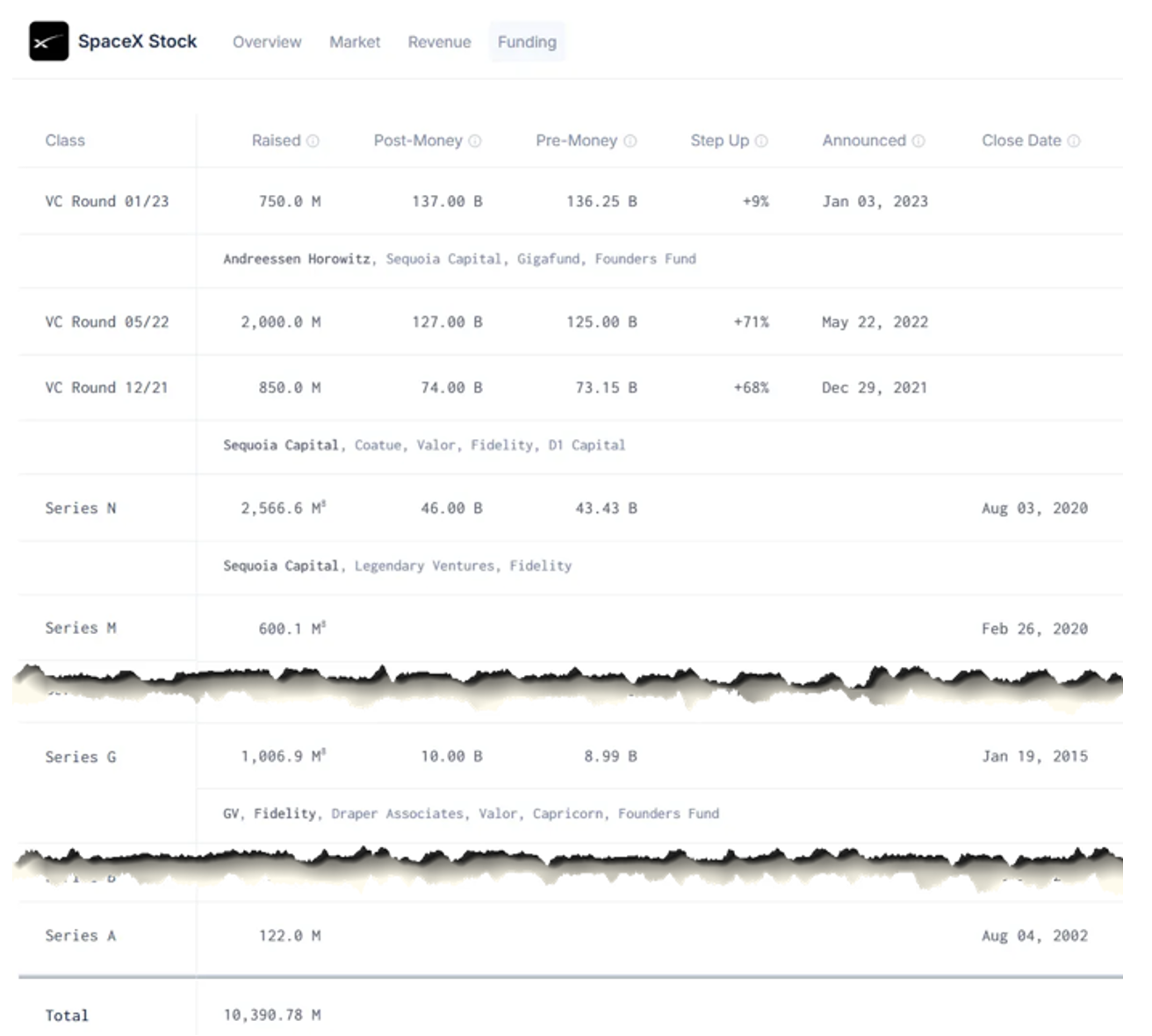

In the first instance, according to an abbreviated fundraising history (Figure 1.), early investors have invested less than US$11 billion and are now enjoying a market ‘paper’ valuation of US$2 reillion. A 20-bagger seems like motivation enough to want to crystalise some of those share gains.

Figure 1. SpaceX fundraising history

Source: BlindSMacro

This week, in a CNBC interview, Yann LeCun, a pioneer of AI, founder of AMI Labs, and former chief AI scientist at Meta, criticised the business models and technology of major AI firms, warning of a potential industry correction.

He specifically highlighted Elon Musk’s xAI as a company that might encounter significant issues, saying, “xAI is kind of a failure, frankly, because the founding team has departed,” adding, “Elon is now in a position that is very, very difficult for him to kind of hire top people in AI, because he’s kind of, you know, not behaved in sort of very good ways toward the … previous team.”

LeCun also noted that xAI’s strategy has been heavy investment in computing infrastructure, particularly the Colossus 1 and Colossus 2 data centres in Memphis. But while the facilities were built to support large-scale AI training, they’re now being rented out to other companies, “because that’s the only way he [Musk] can recoup the cost.”

In the first quarter, SpaceX’s AI division posted a US$2.5 billion operating loss. Building and running advanced AI systems costs a fortune, and despite this AI companies are still rushing to deploy them.

The bottom line is that even though the cost of running AI systems is falling, it’s not falling fast enough. At the same time, the price AI companies need to charge to make a buck has to rise, but customers won’t stomach it. The consequence is large ongoing losses, meaning our enjoyment and use of AI tools is being funded by investors.

The question is, for how long? At some point, either prices have to rise, costs have to plunge, or the bubble has to burst.

Tell him he’s dreamin’

Amid the recent share price correction, sceptics are returning to SpaceX’s S-1 IPO document, scouring it for hints of hubris and hope.

According to the S-1, 80 per cent of the company’s total addressable market (TAM) has nothing to do with Starlink or rockets. Instead;

“We believe we have identified the largest actionable total addressable market (“TAM”) in human history. We estimate that our quantifiable TAM is $28.5 trillion, consisting of $370 billion in Space from space-enabled solutions; $1.6 trillion in Connectivity across $870 billion in Starlink Broadband and $740 billion in Starlink Mobile as well as additional opportunities in enterprise and government; $26.5 trillion in AI across $2.4 trillion in AI infrastructure, $760 billion in consumer subscriptions, $600 billion in digital advertising, and $22.7 trillion in enterprise applications. For illustrative purposes of sizing our addressable market opportunity, we exclude China and Russia from our global estimates.” Page 11, SpaceX S-1

The problem is that non-Musk estimates for ‘AI Enterprise Applications’ range between US$50 and US$300 billion, not the US$22.7 trillion in the S-1.

And then there’s the related party transactions. By way of example, SpaceX purchased US$690 million worth of Tesla Cyber trucks at full retail price and US$700 million of batteries.

The idea that SpaceX can be worth 100 times related party transaction revenue is an absurd one (albeit the sale of the trucks benefits Tesla).

Finally, the biggest question might be just who is left to buy after the index funds and retail investors have their fill?

Figure 1 reveals SpaceX has been paraded before investors since its Series A funding round in 2002. If hedge funds, sovereign wealth funds, and pension funds had the chance to invest at much lower prices but declined, why would they now buy at US$2 trillion?

It will be as much fun to watch SpaceX and the broader AI trade unfold over the next few months as it has been for many of my peers to watch the football World Cup.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.