Companies

-

AFR: Just how good are our banks

David Buckland

November 13, 2014

The Australian Financial Review’s Jeremy Chunn published an excellent piece this week taking a look at the major banks. With full-year results for three of the four major banks delivered in the past two weeks, Jeremy asked five professional investors for their outlook on the sector. This included a London-based analyst for perspective on the value of Australian banks relative to international peers.

The Montgomery team has generated meaningful insights from our research and analysis of the banking space and the impact of the changes emanating from the Financial System Inquiry. Read the article to below to find out which bank is the stand out pick in an industry facing increasing challenges.

Click here to read the article on the AFR’s site.

Please note, you may need to be an AFR subscriber to view this article.

by David Buckland Posted in Companies, Financial Services, Insightful Insights, Montgomery News and Updates.

-

Stress Testing The Banks

David Buckland

November 12, 2014

Wayne Byres, Chairman of Australian Prudential Regulation Authority (APRA) recently made a mockery of the Banks’ self-administered stress tests. continue…

by David Buckland Posted in Companies, Financial Services, Insightful Insights, Montgomery News and Updates.

-

Darth Veda

Russell Muldoon

November 7, 2014

Veda Group Limited (VED) is one of the more successful IPO’s we have participated in recently. Listing in early December 2013 at $1.25 the stock went on to subsequently double in price hitting a high of $2.55 just a few months later.

Adding to this success was the exceptional 2014 full year results that came in ahead of the prospectus guidance, producing one of the best reports over the August reporting season. continue…

by Russell Muldoon Posted in Companies, Insightful Insights, Market Valuation.

-

The Financial System Inquiry

David Buckland

November 5, 2014

I sat next to David Murray AO, Chairman of the Financial Services Inquiry (FSI), at a breakfast meeting yesterday and I understand his final report is scheduled for presentation to Treasurer Hockey before the end of the month.

David is a quiet and very thoughtful guy and with a chuckle he said, “I have been trying to leak the recommendations of the FSI but no one seems to be listening”. continue…

by David Buckland Posted in Companies, Financial Services, Insightful Insights, Value.able.

-

Sirtex: A bright future

Russell Muldoon

October 29, 2014

Yesterday, Sirtex (ASX: SRX) held their AGM, where CEO Gilman Wong provided an excellent address containing a lot of quality information for investors. We thought it was worth sharing some of his insights here.

Among other things, he provided an update on how the business is travelling year-to-date (YTD). Given they are no longer providing quarterly updates, this was a nice-to-have – especially when others speak of key trials, management expectations and future business prospects.

Also, for the first time Gilman presented some information surrounding completely new treatments SRX has been developing in conjunction with universities (some of which we, even after following the business closely for many years) were unaware of.

From the 26-page presentation, these are the comments and slides that caught our attention.

- The 2014 financial year was a highly productive period for Sirtex, as we recorded our 40th consecutive quarter of growth in sales of SIR-Spheres microspheres. We are proud of our growth record and I am pleased to say this trend is continuing and at close of business yesterday YTD dose sales were up 28.7 per cent on the same period last year. Our goal now is to launch our business higher into new levels of growth.

- More and more medical professionals around the world are beginning to realise the enormous potential of our targeted liver cancer therapy to treat a wide range of patients and are hence making the decision to use SIR-Spheres microspheres.

- It is worth noting the news announced a few weeks ago that ESMO, the European Society for Medical Oncology, has identified SIR-Spheres Y90 resin microspheres as an appropriate treatment for patients with colorectal liver metastases that have failed to respond to chemotherapy. We believe the new ESMO clinical guidelines will have a positive effect on improving patient access to SIR-Spheres microspheres across Europe.

- Sirtex’s business in the Asia Pacific is still very much in its infancy but has enormous potential and we continue to create a foothold in new markets.

- Sirtex believes the SIRFLOX result should be positive. This is an evidence based view, founded on the results of six previously completed, albeit smaller clinical studies and the results of two large scale retrospective analyses which were all positive. Indeed, to date there has not been a failed study of SIR-Spheres microspheres.

- A positive result however, should see an acceleration in dose sales growth rates, and potentially a step change in growth in terms of multiples of our current dose sales. Growth is not expected to be instantaneous, but rather a ramp up over ensuing years.

- Several years ago we initiated a clinical study strategy involving five major studies. Unlike many companies that rely on one study, Sirtex has covered many bases and the results of each of our studies can provide significant impact. As our large global studies in metastatic colorectal cancer and hepatocellular carcinoma progress towards completion, we are broadening our focus beyond the liver towards the potential use of SIR-Spheres microspheres to treat cancers in other organs. Leading this program is our RESIRT study investigating the use of SIR-Spheres microspheres in kidney cancer patients. Other studies are planned and we will be providing details once these are confirmed.

- During the year, two new hot cells have been installed in our expanded US facility in Wilmington and the fit-out of our new German manufacturing plant in Frankfurt is on time and on budget. We are well prepared to meet the anticipated sales growth in our current market and new markets.

- Looking to the future, we are working on some highly promising technologies. A good example is the Carbon Cage Nanotechnology that we are developing with the Australian National University. Carbon Cage Nanoparticles can carry a high internal payload of radioactive material which is encapsulated in an outer carbon shell. This carbon shell is chemically inert and possesses ideal properties for the attachment of coatings for a variety of purposes, for example to target specific cancers or to impart stealth-like properties, thereby enhancing their ability to evade detection by the immune system. Carbon Cage Technology could be used in a range of new diagnostic or therapeutic agents with unique characteristics compared to the current state of the art. Our collaboration with the National Cancer Centre of Singapore is to investigate the application of the Carbon Cage Nanotechnology to prevent spread of metastasis after surgery to treat ovarian cancer.

- All of our research programs have the potential to equal or exceed the market potential for SIR-Spheres microspheres.

And perhaps the most important of all of these is the following:

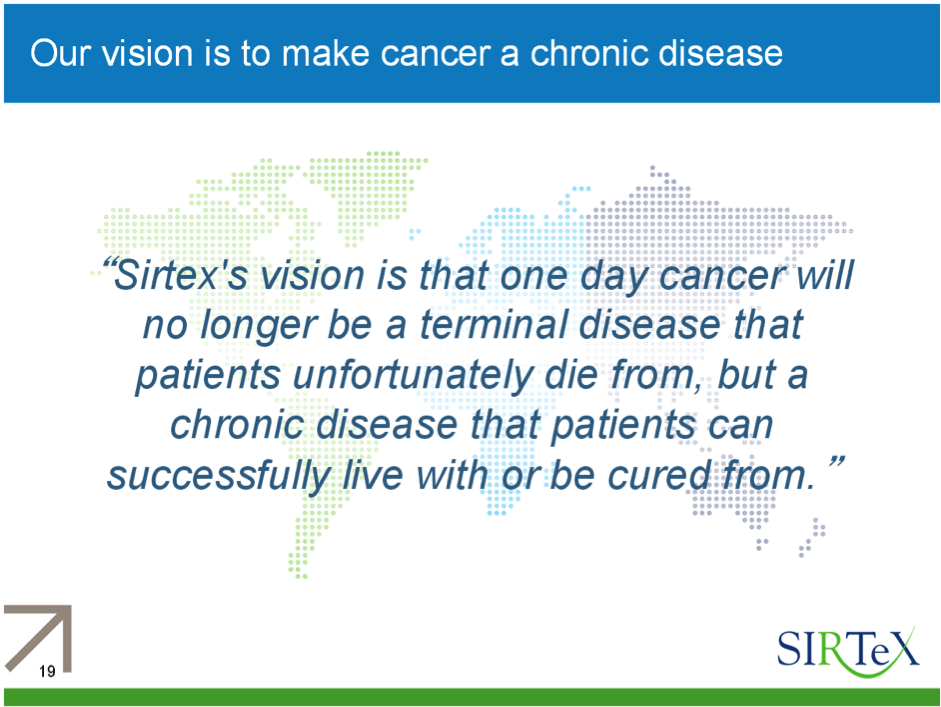

- Together with our customers and collaborators in the medical community, Sirtex shares a common vision where cancer is a treatable chronic condition that patients can successfully live with or be cured from. It is an ambitious goal but one for which there are many precedents. Diseases like HIV, diabetes and heart disease were all considered terminal conditions a few decades ago. Advances in medicine have seen these conditions become chronic conditions people can successfully live with. With liver cancer, we are witnessing a growing body of independent medical evidence that indicates an increasing number of patients are now able to live with their disease. These good outcomes are due to a number of medical innovations which includes SIR-Spheres microspheres.

- To date we have supplied more than 45,000 doses of SIR-Spheres microspheres globally. One of the people to have been treated with SIR-Spheres microspheres is a woman in Melbourne, Elizabeth Deylen. In 2012, Elizabeth was told she had stage four bowel cancer with metastases to her liver and that she had only a few months to live. She was treated with SIR-Spheres microspheres prescribed by medical oncologist Professor Peter Gibbs and his team at the Royal Melbourne Hospital. Two years on and Elizabeth no longer has signs of cancer in her liver and she recently celebrated her 50th birthday in Bali with her family.

What an exciting, Australian-made medical device.

by Russell Muldoon Posted in Companies, Health Care, Insightful Insights.

-

WHITEPAPER

THE PROPERTY RUG PULL

Discover how proposed changes to negative gearing, Capital Gains Tax and holiday home tax rules could reshape property investing, and why investors may consider private credit as property returns become less certain and tax advantages diminish.

READ HERE -

If you can’t beat ’em… join ’em

Scott Shuttleworth

October 17, 2014

The Hong Kong business of REA Group Limited’s (ASX: REA) Realestate.com has been one of a few dull spots on an otherwise bright canvas for quite some time. Through a well-executed move, they seem to have changed their prospects in the country. continue…

by Scott Shuttleworth Posted in Companies, Insightful Insights.

- 2 Comments

- save this article

- POSTED IN Companies, Insightful Insights

-

Don’t let a catastrophe sneak into your portfolio

Scott Shuttleworth

October 13, 2014

The rewards in the stock market can be vast – why else would we spend so much time on it? But the risks can often go overlooked as we dream of retiring down at the beach tomorrow. One risk I’d like to highlight is catastrophe risk. continue…

by Scott Shuttleworth Posted in Companies, Insightful Insights.

- 2 Comments

- save this article

- POSTED IN Companies, Insightful Insights

-

CSL plans for expansion

Ben MacNevin

October 10, 2014

CSL has announced a $450 million investment to expand its global production capacity. continue…

by Ben MacNevin Posted in Companies, Health Care, Insightful Insights, Value.able.

- save this article

- POSTED IN Companies, Health Care, Insightful Insights, Value.able

-

Looking at: Vocus Communications

David Buckland

September 3, 2014

I was reading the Independent Report on the merits of the proposed acquisition of FX Networks by Vocus Communications Ltd (ASX: VOC), and thought I would provide the following points made by KPMG, that haven’t previously been articulated in past posts. continue…

by David Buckland Posted in Companies, Technology & Telecommunications, Value.able.

-

Super Ambitious Group

Scott Shuttleworth

August 29, 2014

Last week, Super Retail Group Limited (ASX: SUL) reported to an uncertain retail sector. Having a flick through their investor presentation and the group’s financials – and considering some of the headwinds over the last financial year – it’s quite a fair result. continue…

by Scott Shuttleworth Posted in Companies, Consumer discretionary, Insightful Insights.