Consumer confidence – A gentle uptrend after a 53-year low

Consumer confidence appears to be slowly improving after hitting its lowest level in 53 years in April 2026. While the recent uptrend is encouraging, confidence remains fragile, with household debt, cost-of-living pressures and recent interest rate increases still weighing heavily on consumers. The question now is whether this rebound marks the beginning of a genuine recovery, or simply a modest lift from extremely depressed levels.

Signs of recovery

The ANZ Roy Morgan Consumer Confidence Survey fell sharply in January and February 2026 (with the monthly average still above 80.5), before plunging to a record low of 63.6 in April 2026 during the middle of the U.S.-Iran War. For context, this survey dates back to 1973.

Since then, the ANZ Roy Morgan Consumer Confidence Survey has entered a gentle uptrend recording 66.0 in May, 71.4 in June and 74.7 in the first week of July.

Are we out of the woods?

Firstly, we need to ask the question, “Why has the ANZ Roy Morgan Consumer Confidence survey recently hit the lowest level on record in 53 years, when most important economic indicators all appear in reasonable shape?”

For example, the Reserve Bank of Australia (RBA) cash rate, inflation rate and the unemployment rate are all approximately four (odd) percentage points at present. This compares with the peak RBA cash rate of 17.5 per cent in 1990, the peak inflation rate of 17.7 per cent in 1975, and the peak unemployment rate of 11.1 per cent in 1992.

The big difference, of course, is consumer debt and the ramifications from a cost-of-living crisis, three RBA cash rate increases in the three months to May 2026, and a relatively unfriendly Fiscal 2027 Federal Government Budget.

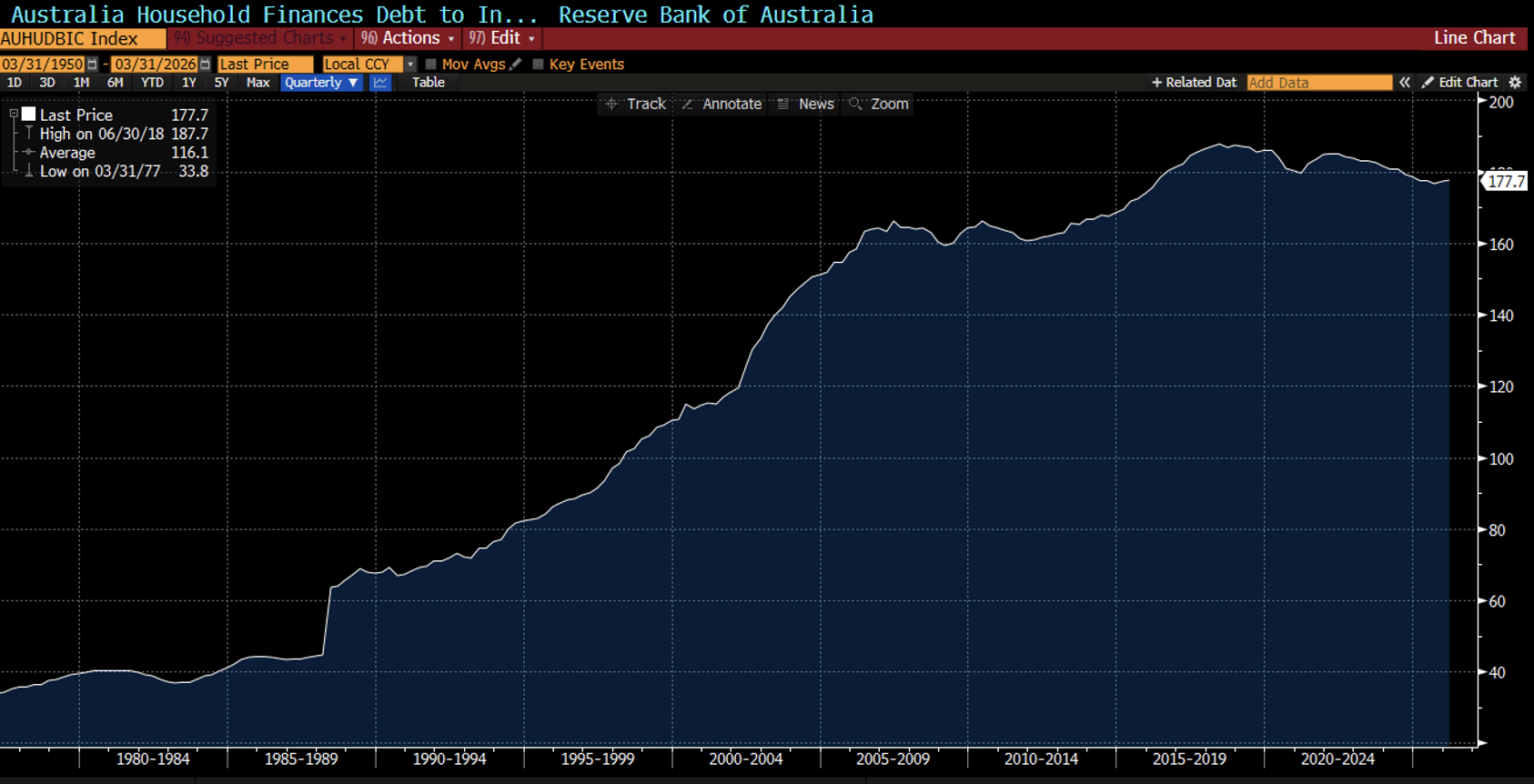

As illustrated in Graph 1. below, at nearly 180 per cent, Australia’s consumer debt to disposable income ratio is running at over five times the level recorded 50 years ago (35 per cent).

Graph 1. Australia’s consumer debt to disposable income ratio

Source: Bloomberg

A nation under pressure

Currently, only 15 per cent of those surveyed say their families are “better off” financially than this time last year; whilst 51 per cent say their families are “worse off”. In terms of the twelve months to July 2027, only 22 per cent expect to be “better off” and 40 per cent expect to be “worse off”.

Just 19 per cent of respondents are saying now is a “good time to buy” a major household item compared to 42 per cent who say now is a “bad time to buy a major household item”.

With the negative noise coming out of the residential property cycle, I believe the RBA will likely sit on its hands until data for the September 2026 Quarter becomes available, especially given the annual household consumption growth is expected to ease further.

What do we make of this?

In yesterday’s Fear and Greed newsletter, there was a piece on the number of people in various countries with net assets exceeding US$1 million. Thanks largely to the price of housing and our Superannuation Guarantee, Australia ranks seventh in the world, with 1.6 million people holding net assets exceeding US$1 million – that’s nearly 6 per cent of our population.

But Australia’s wealth statistics tell only part of the story. The pain is very unevenly spread, with the bottom two quintiles in Australia (lowest 40 per cent of households with an annual disposable income of up to $70,000) under significant financial pressure.

Many households continue to struggle with the combined pressures of debt, higher interest rates and the rising cost of living. The recent improvement in consumer confidence is encouraging, but it is too early to conclude that Australian consumers are out of the woods.

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.