Buffett vs. Musk

“You cannot be afraid of new technologies. I think that this tenet passed Warren Buffett by. As he is the greatest investor of all time, I think it’s important to recognise that if he were not afraid of product cycles and obsolescence, he would have made much more these last few years than he did. Now, I know we shouldn’t criticise someone of his unbelievable prowess, but we must also recognise that it was wrong not to include technology stocks in the portfolio…[they] are creating too much wealth to ignore.”

With Musk now the world’s first recorded trillionaire after SpaceX’s float last Friday, you might be thinking the above quote has merit, especially as 60 per cent of Berkshire Hathaway’s portfolio is sitting in cash.

But the above quote, by Jim Cramer, was made in January 2000, just three months before the Dot.Com crash wiped 76.81 per cent from the tech-heavy NASDAQ Composite index and investors saw an estimated US$5 trillion in paper wealth evaporate between 2000 and 2002.

AU$400 Billion reality check

Wall Street is currently drunk on the “New Era/Artifical Intelligence (AI)” narrative. Between the unrelenting surge in AI chip stocks (Figure 1.) and the blinding, multi-trillion-dollar, 100x-revenue hype surrounding the highly anticipated SpaceX Initial Public Offering (IPO), everyday investors are throwing valuation models out the window.

Figure 1: South Korea KOSPI index, up 89 per cent since December 31st.

Source: Google Finance

But while Fear Of Missing Out (FOMO)-driven retail and professional investors alike frantically bid up anything with an AI label or a rocket logo, the savviest money manager in history continues to build the largest bunker in financial history.

So, what does Berkshire Hathaway’s cash pile actually mean for this AI boom, and why wouldn’t Warren Buffett touch the SpaceX IPO?

The US$400 billion elephant in the room

If you want to know what Warren Buffett and his newly minted CEO Greg Abel actually think, look at what they’re doing.

In Berkshire’s Q1 2026 earnings report, early last month during their annual shareholder weekend, the company revealed that its cash and short-term U.S. Treasury bills had swollen to a record-breaking US$397.4 billion.

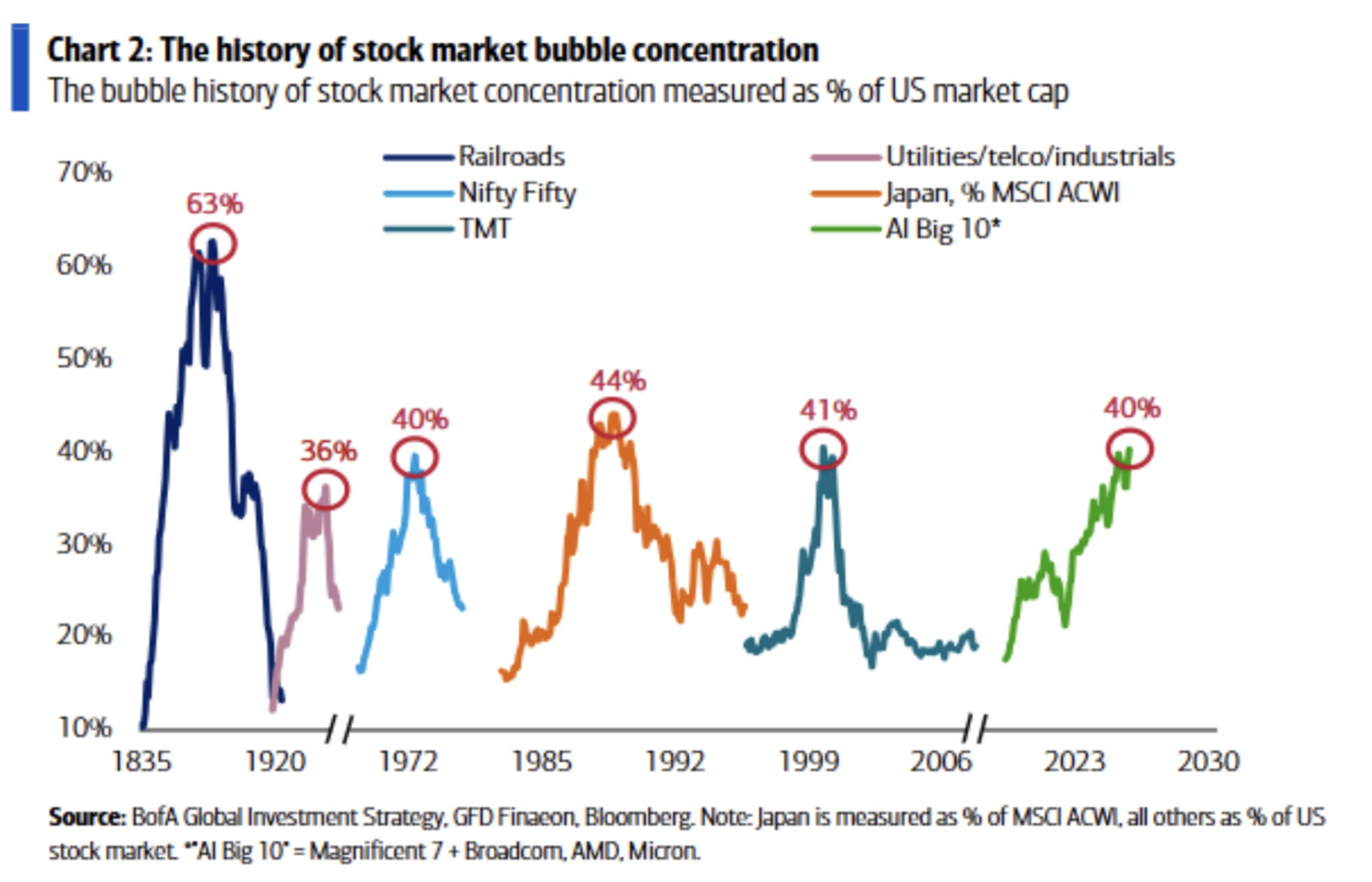

Berkshire is sitting on a hoard of dry powder that’s US$100 billion larger than New Zealand’s entire annual Gross Domestic Product (GDP). And it represents nearly 60 per cent of Berkshire’s total investable assets. While the S&P 500 has rallied nearly 10 per cent in 2026, driven almost entirely by the narrow, historic concentration of the Magnificent Seven (Figure 2.) and AI hardware plays, Berkshire deliberately chose to sit on its hands, net-selling US$8.1 billion in equities during the first quarter alone.

Figure 2. Past and current major thematic concentrations

Source: BofA Global Investment Strategy, GFD Finaeon, Bloomberg.

The Oracle of Omaha and Greg Abel aren’t buying this market.

At the annual meeting in May, the 95-year-old Buffett reminded the crowd of his two rules of investing: Rule No. 1 is never lose money; Rule No. 2 is never forget Rule No. 1. When the market can’t find cheap assets, Buffett noted, holding cash isn’t a drag – it’s a competitive edge. And with U.S. Treasury bills yielding 4 per cent to 5 per cent, Berkshire is happily pulling in US$15 billion to US$20 billion a year in risk-free interest just for waiting. They can afford to be patient. With cash sitting in Aura’s Core Income Fund, a private credit fund with an externally S&P Equivalent Portfolio Credit rating of AA and generating 7.20 per cent per annum since inception on 4 October 2022 to 30 April 2026, I also have an allocation to ‘patience’. *Returns are net of fees and assumes reinvestment of distributions. Past performance is not a reliable indication of future performance.

AI: The “Digital Atomic Bomb”

But what about AI? Like Jim Cramer in 2000, investors today are criticising Berkshire in the short term for its “old economy” tilt toward railroads, insurance, and energy, noting that it has largely sat out the AI-driven tech surge.

Buffett remarked that while AI has the potential to double operational efficiency, it will also allow sophisticated scams and misinformation to flourish at an unprecedented scale. More importantly, he reiterated his timeless rule: When faced with unfamiliar technology, he steers clear.

I believe Buffett and Abel recognise that while AI will undoubtedly change the world, predicting which hyper-valued tech company will sustain a competitive advantage for the next twenty years is impossible right now. They’d rather hold US$397 billion in cash and wait for the bubble to burst than gamble shareholder capital on unproven ‘moats’.

The SpaceX IPO: Rocket science valuations

SpaceX violates the circle-of-competence rule that Buffett has adhered to for decades. For an analyst looking for predictable, boring cash flows, SpaceX’s S-1 filing reads less like a financial prospectus and more like a sci-fi manifesto. “AI” is mentioned 1200 times in the IPO’s S-1 filing, alongside a maze of shifting narratives ranging from satellite internet constellations to multiplanetary missions and existential side-quests.

The first ten pages are pictures of rockets, and the S-1 includes quotes like, “we do not want humans to have the same fate as dinosaurs,” and “we believe the next paradigm shift for humanity is the creation of a resilient, perpetually expanding, spacefaring civilisation, ultimately preparing us to Kardashev type 2 status.”

I am not making this up, and I’m reminded of the shared workspace provider, WeWork, which went bust but was once worth US$47 billion. It said its mission was to “elevate the world’s consciousness.”

Of course none of that matters now the stock is listed and closed it’s first day at a 20 per cent premium to the IPO price.

I expect the stock will remain supported as index funds have to buy ahead of the stock’s inclusion in the NASDAQ index in 15 days. It will also remain supported at least until the quarterly results for the June quarter are released, after which 20 per cent of insider stock is released from escrow.

For SpaceX, the standard 180-day lock-up is replaced with a dynamic, multi-stage release valve:

- First post-earnings release: Two trading days after reporting its first financial results (covering April–June), up to 20 per cent of eligible insider shares unlock. An additional 10 per cent unlocks if the stock trades at least 30 per cent above the IPO offering price for at least 5 of 10 consecutive trading days.

- Rolling time-based tranches: At 70, 90, 105, 120, and 135 days post-listing, another 7 per cent of eligible shares are released in each tranche.

- Second post-earnings release: Upon reporting its second quarterly earnings (for the three months through September), a further 28 per cent of shares can be sold.

- The 180-day cliff: At the 180-day mark, any remaining locked shares are fully released.

Let’s not forget the company makes more revenue from renting its Nvidia chips out to Anthropic than it does from space and rockets, and its Starlink telco business generated US$11 billion of the US$18 billion in revenue reported in 2025.

Meanwhile, the company swung from a modest net income of US$791 million in 2024 to a bruising US$4.9 billion net loss in 2025 thanks to spending on the Ai infrastructure landgrab.

The bottom line for investors

We’re living through another “this time is different” market. The tech sector now commands nearly a third of the S&P 500’s total market value, and while it feels like a party that will never end and it’s safe to jump aboard, just remember Warren Buffett isn’t.

The smartest, most experienced capital allocator on the planet is sitting in a room stuffed with US$397 billion in cash, refusing to buy. That’s telling you everything is overpriced. Berkshire’s cash hoard is telling you that AI hype is a terrible justification for an investment.

You don’t have to agree with Buffett’s cautious stance, and you might even make a quick buck riding the momentum of the AI wave or the SpaceX IPO. But history tells us that when the music stops, the investors holding the cash are the ones who get to buy up the wreckage at a discount.

Disclaimer:

You should read the relevant Product Disclosure Statement (PDS) or Information Memorandum (IM) before deciding to acquire any investment products.

Past performance is not a reliable indicator of future performance. Returns are not guaranteed and so the value of an investment may rise or fall.

This information is provided by Montgomery Investment Management Pty Ltd (ACN 139 161 701 | AFSL 354564) (Montgomery) as authorised distributor of the Aura Core Income Fund (ARSN 658 462 652) (Fund). As authorised distributor, Montgomery is entitled to earn distribution fees paid by the investment manager and may be issued equity in the investment manager or entities associated with the investment manager.

The Aura Core Income Fund (ARSN 658 462 652)(Fund) is issued by One Managed Investment Funds Limited (ACN 117 400 987 | AFSL 297042) (OMIFL) as responsible entity for the Fund. Aura Credit Holdings Pty Ltd (ACN 656 261 200) (ACH) is the investment manager of the Fund and operates as a Corporate Authorised Representative (CAR 1297296) of Aura Capital Pty Ltd (ACN 143 700 887 | AFSL 366230).

You should obtain and carefully consider the Product Disclosure Statement (PDS) and Target Market Determination (TMD) for the Aura Core Income Fund before making any decision about whether to acquire or continue to hold an interest in the Fund. Applications for units in the Fund can only be made through the online application form that accompanies the PDS. The PDS, TMD, continuous disclosure notices and relevant application form may be obtained from www.oneinvestment.com.au/auracoreincomefund or from Montgomery.

The Aura Private Credit Income Fund is an unregistered managed investment scheme for wholesale clients only and is issued under an Information Memorandum by Aura Funds Management Pty Ltd (ABN 96 607 158 814, Authorised Representative No. 1233893 of Aura Capital Pty Ltd AFSL No. 366 230, ABN 48 143 700 887).

Any financial product advice given is of a general nature only. The information has been provided without taking into account the investment objectives, financial situation or needs of any particular investor. Therefore, before acting on the information contained in this report you should seek professional advice and consider whether the information is appropriate in light of your objectives, financial situation and needs.

Montgomery, ACH and OMIFL do not guarantee the performance of the Fund, the repayment of any capital or any rate of return. Investing in any financial product is subject to investment risk including possible loss. Past performance is not a reliable indicator of future performance. Information in this report may be based on information provided by third parties that may not have been verified.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.