Why house prices won’t fall 40 per cent

There’s been a conga line of prognosticators who have forecast falling house prices. All of them have faded into history as house prices have grown since the 1970s, first at the rate of inflation, then at the rate of wage growth, then at the rate of Artemis II launch.

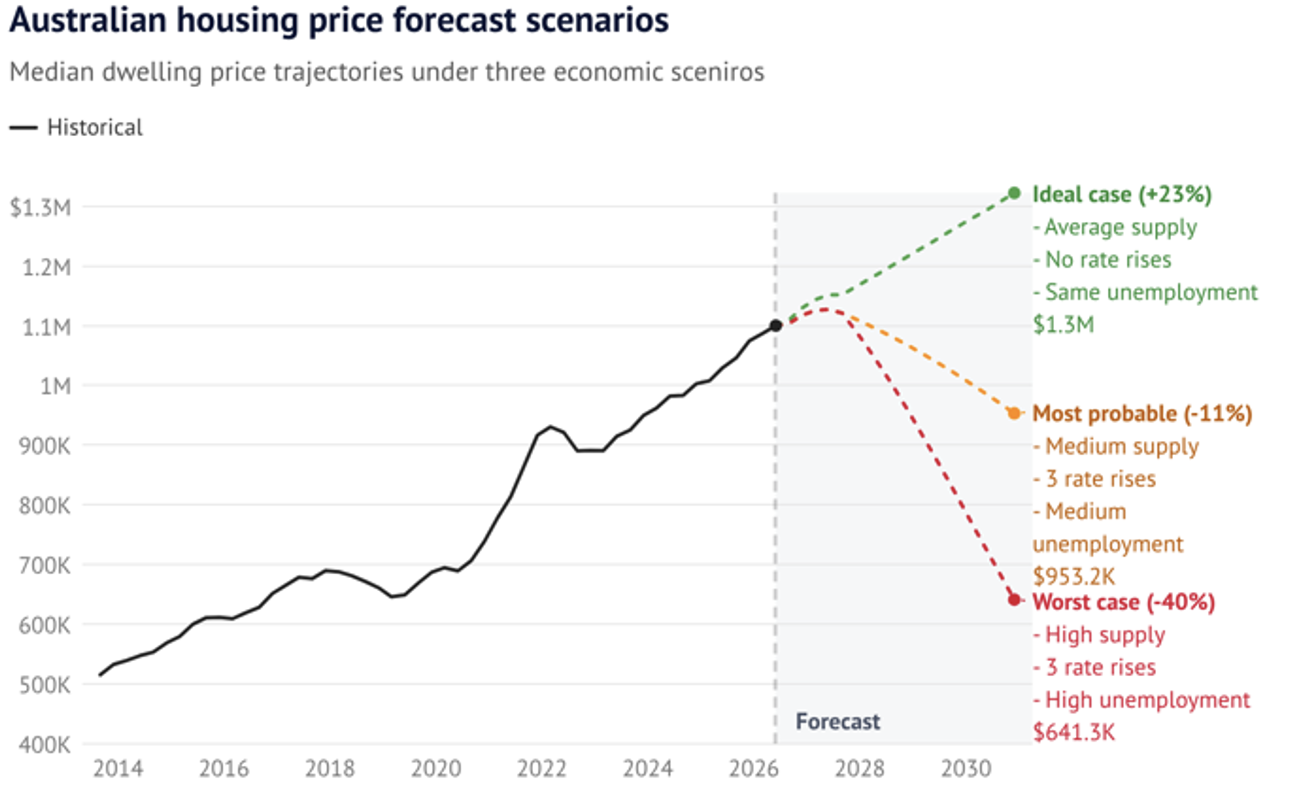

Recently, Money.com.au contracted Primara Research to produce a forecast of Aussie house prices for 2030 under a variety of interest rate, supply, and unemployment scenarios.

Figure 1. Primara’s forecasts

Source: ABS, Labour Force, RBA, Money.com.au

According to Primara’s “most probable” scenario, Australia’s average national house price will rise by just under five per cent to June 2026 and then start falling. By 2030, the Australian average house price will be 15.4 per cent lower than that peak, falling to $953,000, which is not far from its level in March 2024. In other words, no price growth between March 2024 and June 2030.

Because it is an ‘average’ figure and averages are made up of highs and lows, for that 15 per cent average decline to occur, there will have to be properties that fall a lot more, because there will be properties that decline a lot less.

Primara has also published a worst-case scenario for Money.com.au, projecting a 40 per cent average house price decline from June next year to 2030, which would send the average house price back to 2017 levels.

Of course, anything is possible, but let me tell you who will work to prevent either of those scenarios. Then you can decide whether there is plausibility or merit in the worst case or even the ‘most probable’ forecast.

- The Government

Every government has incentivised people to buy houses. From the current Help to Buy shared equity scheme, the 5 per cent Deposit Scheme, and the First Home Super Saver Scheme, to the Covid-era HomeBuilder Grant, the First Home Owners Boost of 2008-2010, the First Home Owner Grant of 2000, and back to the First Home Owners Scheme of 1983, the Home Deposit Assistance Grant of 1982 and the Home Savings Grant Scheme of 1964, successive governments from Menzies to Albanese have encouraged people to buy real estate.

And you’ll notice that despite the cries of unaffordability by the third of Australians who don’t own a home, not once has any government ever said: “let’s bring down house prices”. No, instead, they give people more money they’re able to afford higher prices. Bringing down house prices would offend the one-third of Australian households who own their own their home outright and the other third who have a mortgage – all of whom were incentivised by the government of the day to buy.

The government won’t want to put offside the two-thirds of households who own or are on their way to owning. It’s not in the re-election interests of the government to see house prices falling, and it would not be in their interest to effect any strategy that caused house prices to fall.

- The Government (again)

Add to point 1., the impact of the wealth effect on the economy. When people see their home value rising on paper, they feel wealthier and are more likely to take out personal loans, car loans, or credit cards. They are more likely to spend, and that’s good for the economy. Any government presiding over a recession is less likely to be re-elected.

My conclusion is that were house prices to begin sliding more than 10 per cent, you can bet the government of the day would do what it can to reverse the decline.

- Banks

To understand why Australian banks are also sensitive to house price declines, you have to look at them less like deposit stores and more like mortgage businesses. In Australia, the big four banks (CBA, Westpac, ANZ, and NAB) are essentially massive portfolios of residential property debt with a small banking business attached.

Under the Australian Prudential Regulation Authority (APRA) regulations, the amount of capital a bank has to set aside (which it can’t use to make money) is tied to the risk of its loans. Loans with a Loan-to-Value Ratio (LVR) of 80 per cent or less are considered ‘safe’ and require less capital. If house prices fall by, say, 10 per cent, a borrower who originally had an 80 per cent LVR suddenly has an 88.88 per cent LVR, and when a loan moves into a higher LVR bracket, the ‘risk weight’ increases.

In other words, the bank is forced by law to set aside more of its own capital to back that loan. This reduces the bank’s Return on Equity (ROE) and its ability to pay out dividends to shareholders.

Meanwhile, rising prices allow homeowners to refinance and top up their loans to renovate or buy investment properties. This creates new debt, which is the primary product banks sell. If house prices rise, the average loan size increases. Since banks charge interest as a percentage, a $1m loan at 6 per cent generates much more profit than a $500k loan at 6 per cent, and the work to manage the loan is exactly the same.

So, banks do not want to see widespread declines in house prices.

By the way, they’re just some of the reasons why, during COVID, even though millions of people were out of work, the banks gave everyone a repayment ‘holiday’, and why we didn’t see a wave of Mortgagee in Possession sales. Banks do not want house prices to decline and will also do everything they can to prevent it.

- The regulators. APRA and the RBA

While neither regulator has a formal mandate to raise house prices – and they often publicly state they don’t target house prices at all – their core responsibilities for Financial Stability and Economic Growth potentially turn them into something of a safety net for the housing market.

Another way to think about APRA is as the Bank Police. Their primary job is to ensure that your bank doesn’t disappear with your savings if the world ends.

Roughly 60-65 per cent of the assets on Australian bank balance sheets are residential mortgages. If house prices drop by 20 per cent, the collateral backing those hundreds of billions of dollars in loans shrinks, and if house prices fall significantly – as Primara suggest – the ‘Loss Given Default’ (how much money the bank loses when a borrower fails) skyrockets.

In that scenario, banks would protect themselves and their shareholders by ceasing to lend to everyone – businesses, personal borrowers, and new buyers. This is called a credit squeeze, and it would cause house prices to fall even further because fewer people would qualify for a loan to buy them.

APRA’s mandate is effectively a license to stop this doom spiral before it starts.

The Reserve Bank of Australia (RBA), on the other hand, has an incentive similar to the government’s – to maintain economic growth. Thanks to the reverse wealth effect from falling house prices, they would cut rates aggressively and provide emergency, low-cost funding to get credit growth going again. Indeed, they would do it long before prices fell anything even approximating Primara’s worst scenarios.

Conclusion.

House prices cannot crash because it would break the banking system, roll the government and smash the economy. Everyone has an incentive to see stable price increases. So, don’t bet on house prices falling.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.