Market’s foetal position – A gift for investors

While Israel pursues a high-stakes military campaign and President Trump plays ‘Deal or No Deal” with an Iranian regime that might not even have a leader in charge, investors are doing the only sensible thing left: Hiding.

With the Islamic Revolutionary Guard Corps (IRGC)’s ‘asymmetric’ threat to the Strait of Hormuz continuing and the U.S. increasing its on-the-ground footprint as America’s 31st Marine Expeditionary Unit arrives in the Middle East, the risk of a recession has also risen.

I’ve been warning of a bubble and pullback for a while now, not because I predicted a war but because market values were elevated and the return on investment (ROI) on artificial intelligence (AI) was unknowable and possibly questionable. But now, as the ‘fog of war’ turns into Trump’s ‘bog of war,’ the current 8.7 per cent dip in the S&P 500 looks more like the start of a 10 per cent-15 per cent slide, which, importantly, is already delivering some mouth-watering opportunity, as you will see in a moment.

Trump, Israel, and the IRGC

Market visibility is dropping rapidly as the likelihood of direct U.S. ground involvement grows. With the Pentagon dispatching roughly 15,000 troops, the risk of a protracted conflict with escalating American casualties adds another layer of uncertainty because it will almost certainly trigger a political backlash back in the U.S.

Trump’s wavering ultimatum to cripple Iran’s energy grid and power infrastructure, as well as his five-minute rant about pens and a meeting to customise a Sharpie pen (of which the pen manufacturer says never occurred) has investors, as well as voters, on edge again, at least until Monday, April 6 at 8:00 PM EST which is the new Obliteration Day deadline.

A significant issue is that while Israel focuses on dismantling localised threats, American diplomats are hunting for a credible negotiating partner in Tehran. And even if they find someone in the Islamic Revolutionary Guard Corps (IRGC) with any authority, the fractured nature of Iran’s leadership means rogue factions of the IRGC might simply ignore any brokered peace deal. Moreover, any deal made with Tehran must also account for its proxies, including Hezbollah in Lebanon and the Houthis in Yemen, who themselves have proven capable of disrupting global trade.

I don’t know if this turns into a full-blown bear market – nobody does – but the probability is non-zero and rising at the moment. If the IRGC continues to deploy its asymmetric playbook of drones and fast-attack boats to throttle transit through the Strait of Hormuz, the magnitude of any potential further slide in markets rises.

Some analysts have projected the probability of a full-blown bear market and economic recession at 35 per cent, and noted markets cannot truly stabilise until global energy corridors are guaranteed safe and open.

The Strait of Hormuz is the world’s most important oil transit chokepoint. Roughly 21 million barrels of oil pass through it daily, accounting for about 20 per cent of global petroleum consumption. During previous flares impacting Middle Eastern maritime trade, war-risk insurance premiums for oil tankers spiked, as they have done again, a cost directly passed on to consumers, which also forces Treasury bond yields to remain elevated.

Figure 1. U.S. 10-year bond yield

Source: Trading Economics

The S&P 500 is now 8.7 per cent below its all-time peak, reached on January 27. A 15 per cent slide will drag the index down to 5,930. Adding to concerns among some investors, the S&P 500 equal-weighted index is also sliding, indicating the weakness is broad-based and not confined to mega tech stocks.

Table 1. Scenarios

|

Market Scenario |

S&P 500 Level (Approx.) |

Driver |

|

Current Drawdown (8.7 per cent) |

Hovering around 6,370 |

Anxiety over U.S. troop deployments and failed diplomacy. |

|

Projected Correction (15 per cent) |

5,930.81 |

Successful IRGC blockade or drone strikes in the Strait. |

|

Bear Market Threshold (20 per cent) |

5,580.00 |

Full-scale regional war involving energy infrastructure destruction. |

The good news

While everyone is focused on the major indices being less than 10 per cent off their highs and pontificating about more to come. There are high-quality companies whose share prices have already declined 50 per cent, 60 per cent, and even 75 per cent. That is a cataclysmic crash in anyone’s language.

There are many software companies trading around the world that were already struggling before this conflict began. Businesses assumed to be cannon fodder for AI are now trading on single-digit price-to-earnings (P/E) ratios. Companies that were once trading at high double-digit P/Es – think 300 times – because they were considered to be the owners of impenetrable competitive advantages are now trading on mid-teen P/E ratios.

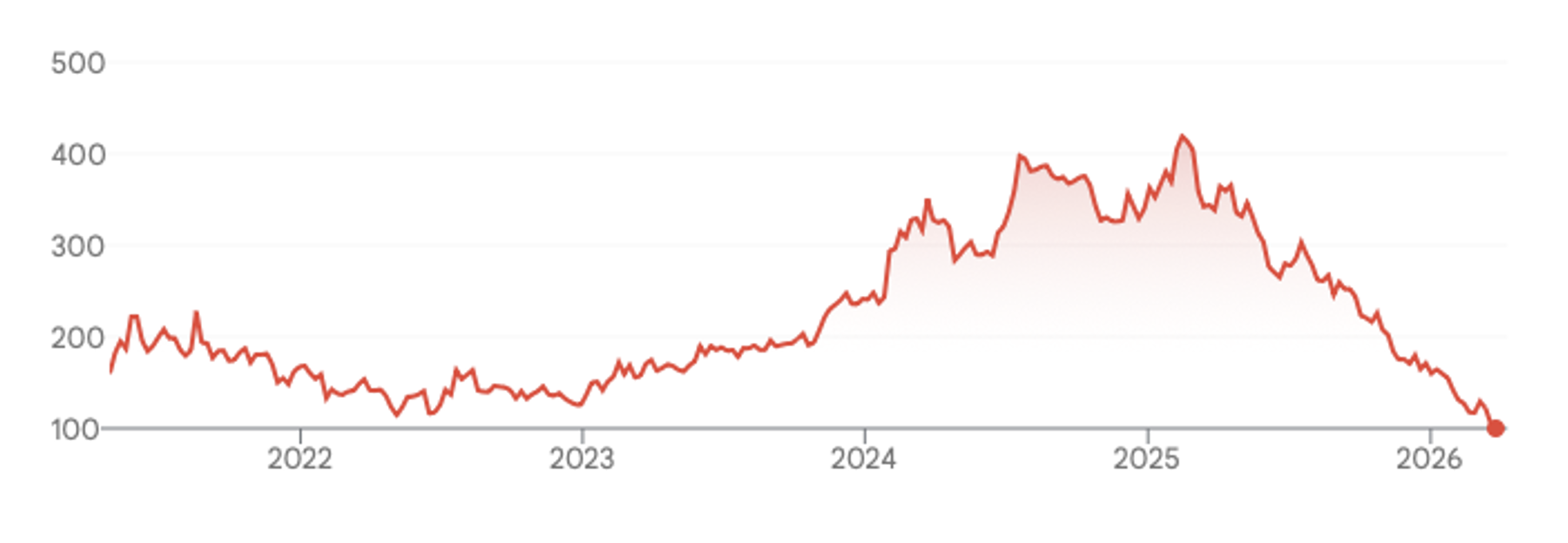

By way of example, Hemnet (OSTO:HEM) is Sweden’s leading, dominant online property platform, featuring over 90 per cent of all residential listings. Founded in 1998, it serves as the primary marketplace for buyers, sellers, and agents, attracting over 42 million monthly visits. It operates on a ‘vendor-pays’ model, and lists homes solely through real estate agents.

Figure 2. Hemnet (STO:HEM) Share Price (Swedish Krona SEK)

Source: Google Finance

At its most popular, Hemnet traded at 328 times trailing twelve months earnings. It’s median P/E over ten years is 67.80 times and today it trades at less than 20 times after a 76 per cent slide from its highs.

Long-term investors who believe AI won’t stop people searching for homes by looking at listings themselves may find bargains among these sorts of stories.

Here in Australia, there have been equally dramatic falls among the good, the bad, and the ugly. For example, Accent Group is down 60 per cent in the last year, Beacon Lighting Group has fallen 52 per cent, Guzman y Gomez is off 50 per cent, and Seek is down 41 per cent. Meanwhile, REA Group is down 34 per cent, Car Group is 32 per cent lower than a year ago and Flight Centre is down 25 per cent.

Will AI kill all these companies? Will the war in the Middle East do likewise?

To be fair, there should be no surprise in last week’s market panic. But if you are a contrarian investor, there’s a silver lining in all this chaos. For time immemorial, extreme bearish sentiment has been fertile ground for quality-based value investors. Remember, investors tend to overreact on both the positive and negative sides.

Fear drives weak holders out of the market. When institutional cash sits on the sidelines with its managers curled up in a foetal position, any positive headline will ignite a massive relief rally. Of course, before stocks can mount a sustained recovery and then another bull market, the heavy fog of geopolitical uncertainty must first begin to dissipate. But if you wait for that, spring has already sprung.

The time to turn over stones is fast approaching, if it’s not already begun.

Disclaimer:

The Australian Eagle Trust holds a short position in Seek, and REA Group. This article was prepared 30 March 2026 with the information we have today, and our view may change. It does not constitute formal advice or professional investment advice. If you wish to trade Seek and REA Group, you should seek financial advice.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.