Consumer confidence hits a record low (while the NASDAQ Index hits a record high)

Australia and the United States (U.S.) currently have one thing in common.

Consumer confidence is in a world of pain.

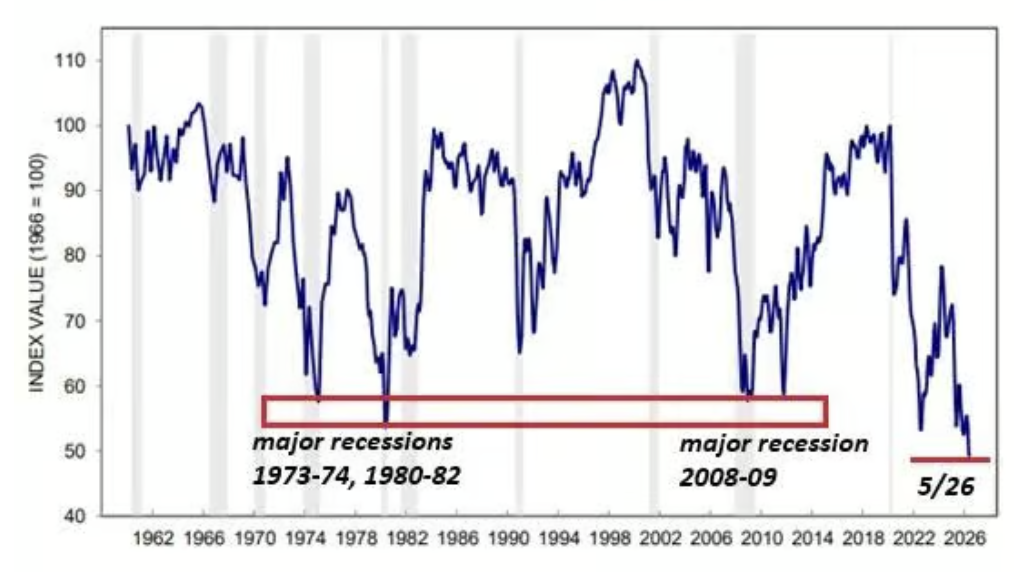

In the U.S., the Consumer Sentiment Index (CSI) has fallen to the lowest level ever recorded since the University of Michigan began tracking the data in 1952.

The Index, see Graph 1. and Table 1. below, hit 44.8 in May 2026, as Americans fear inflation, rising fuel costs, economic instability associated with the Iran War and the worry artificial intelligence (AI) will take white collar jobs.

When I look at the U.S. inflation rate – which was 3.8 per cent for the year to April 2026 – and the U.S. Federal Funds Rate at 3.75 per cent, I again point out a significant anomaly.

That is, the U.S. inflation rate in 1980 hit 13.5 per cent, three and a half times the current rate; and by 1980 the U.S. Federal Funds Rate had hit 20.0 per cent, five times the current rate.

The unemployment rate in the U.S. is currently 4.3 per cent after peaking at 10.8 per cent in 1972.

In March 1984, the University of Michigan Consumer Confidence Index hit 101, more than 56 points above the current level. And in June 2000, the Index reached a peak of 112. As the Americans would say, “go figure”.

Graph 1. The Michigan Index of Consumer Sentiment

Source: Surveys of Consumers, University of Michigan May 2026

Source: Surveys of Consumers, University of Michigan May 2026

Similarly, in Australia. After three consecutive 0.25 per cent increases in the three months to May 2026, the Reserve Bank of Australia (RBA) cash rate is 4.35 per cent, and this compares with 17.5 per cent in January 1990.

Also, in 1982 inflation hit 12.5 per cent. Now it is 4.2 per cent. Unemployment peaked in December 1980 at 11.2 per cent and that compares with the current unemployment rate of 4.5 per cent.

And meanwhile the ANZ/Roy Morgan Consumer Confidence Index has, over recent weeks, hit the lowest level since the data collection began in 1972.

Table 1. U.S. and Australian economic indicators

|

United States |

Current* |

Peak |

Peak year |

|

Unemployment rate |

4.3 per cent |

10.8 per cent |

1972 |

|

Cash rate |

3.75 per cent |

20.0 per cent |

1980 |

|

Inflation rate |

3.8 per cent |

13.5 per cent |

1980 |

|

University of Michigan Consumer Confidence Index |

44.8 |

112.0 |

2000 |

|

|

|

|

|

|

Australia |

Current |

Peak |

Peak year |

|

Unemployment rate |

4.5 per cent |

11.2 per cent |

1980 |

|

Cash rate |

4.35 per cent |

17.5 per cent |

1990 |

|

Inflation rate |

4.2 per cent |

12.5 per cent |

1982 |

|

ANZ/Roy Morgan Consumer Confidence Index |

66.1 |

131.4 |

2005 |

*All data at 27 May 2026 with exception of the inflation data at 30 April 2026

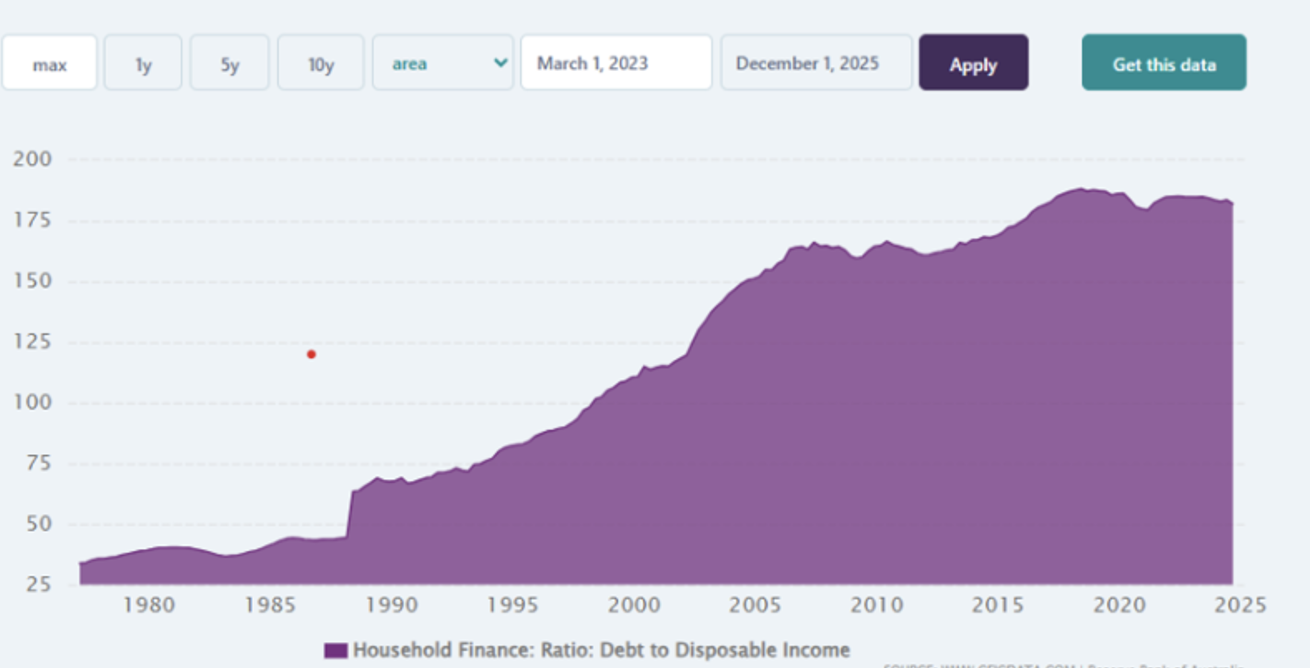

I believe this is a story of debt and hope, or lack thereof.

In Australia, for example consumer indebtedness as a proportion of disposable income, has jumped more than four-fold since 1980 from sub 40 per cent to 180 per cent.

Graph 2. Australia’s household finance: Ratio: Debt to disposable income from March 1977 to December 2025

Source: RBA, CEICDATA.com

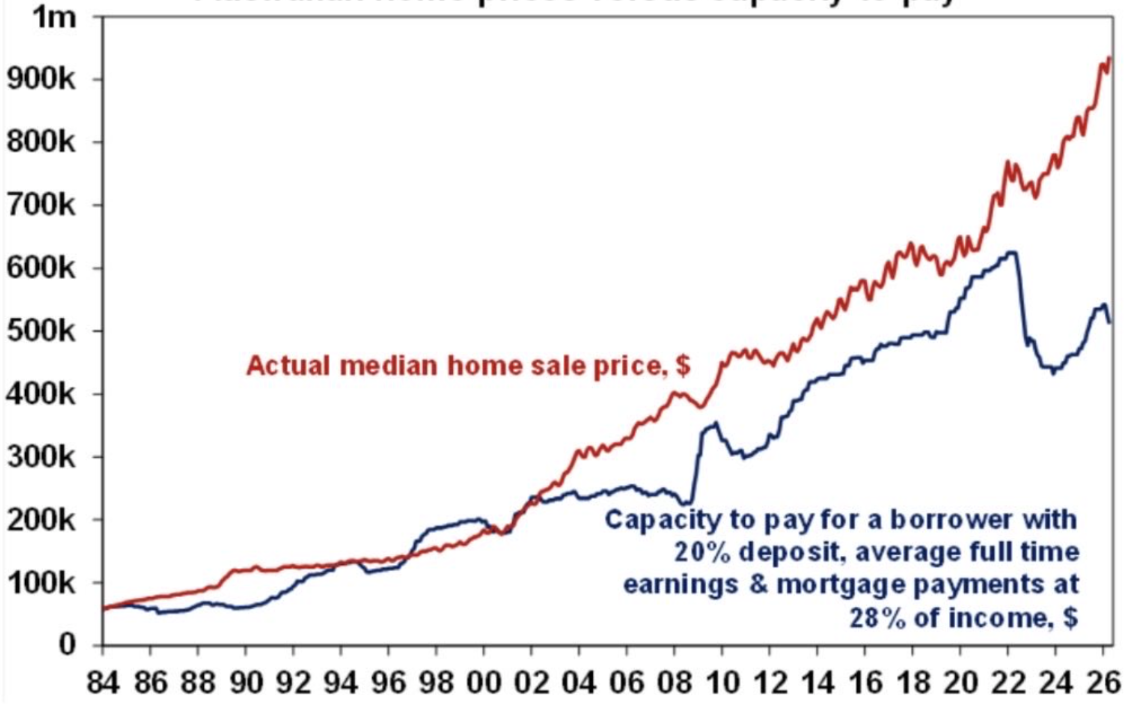

The national unemployment rate has also risen to its highest level since November 2021 and is expected to worsen as the RBA tightens monetary policy, governments rein in spending, AI takes some white collar jobs and the global energy shock takes its toll. Australian home values have grown well beyond what buyers can afford at current interest rates – and as rates rise further, prices must fall to close that gap.

The dilemma facing home prices is summarised by the following chart from Shane Oliver, Economist at AMP:

Graph 3. Australian home prices versus capacity to pay

Source: Cotality, ABS, AMP

So, unless you’re lucky to have rich parents or grandparents, good luck with buying a house, or even renting an apartment.

Adding to this anxiety is the fear of falling property prices. Investment bank Morgan Stanley has warned that the 2026 Federal Budget’s changes to negative gearing and capital gains tax could trigger a national decline in home values of as much as 10 per cent – the sharpest fall in at least 40 years.

With investors making up one-third of marginal housing demand, the tax changes carry a huge impact on potential demand. Auction clearance rates have recently declined to multi-year lows in Sydney and Melbourne, while new listings are tracking above the five-year average. For the millions of Australians whose wealth is tied to their home, this is likely another source of uncertainty eroding consumer confidence.

Consumer sentiment measures confidence, and despite historically low unemployment, cash rates and inflation, this confidence is currently in short supply.

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.