Yardeni vs. Burry – The Bull vs. the Bear

Red Corner (Bull) Ed Yardeni

I have written about and referenced both gents for years, and if you’d like to hear from them first-hand, you can subscribe to their musings on Substack. In the red corner is Ed Yardeni, founder of Yardeni Research and in the blue (bearish corner) is Michael Burry.

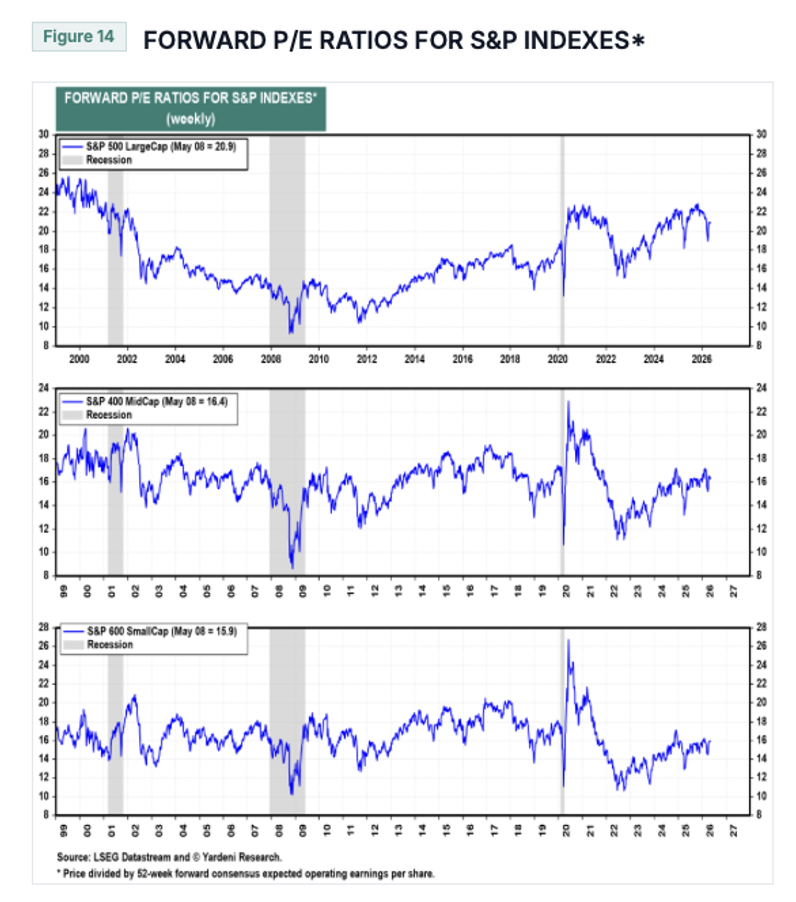

Figure 1. Yardeni Research price-to-earnings (P/E) chart.

Source: LSEG Datastream, Yardeni Research

Dr. Ed Yardeni (born March 15, 1950) is an American economist and investment strategist, formerly for EF Hutton, Prudential Securities, and C. J. Lawrence before founding Yardeni Research.

Yardeni invented the disputed “Fed model” of equity valuation and coined the term “bond vigilante”. He is generally bullish, and his often optimistic outlook on economic expansion, particularly regarding technology’s impact on productivity, has earned him the nickname “Dr Boom”.

In 1999, while an economist for Deutsche Bank, Yardeni – one of the most outspoken Y2K “doomsayers” leading up to the year 2000 – predicted a 70 per cent chance that Y2K computer bugs would cause a severe global recession and a 5 per cent chance of a depression.

In December 1999’s Y2K Reporter, due in part to companies that had preannounced a reduction in earnings during the first and possibly second quarters of 2000 because of Y2K computer glitches, Yardeni was quoted, “there should be some signs that the worst is over and that a recovery is on the way.”

In the same article, and just prior to the Tech Wreck stock market crash, which began in March 2000 and ended the DotCom bubble, Yardeni told Y2K Reporter that he sees lower stock prices over the next six months and a rebound to new highs next year (2000) with the Dow Jones Industrial Average topping 15,000 by 2005.

From the Dow’s monthly closing high of 11,497 points, the index fell 34 per cent by September 2002. At the end of 2005, the Dow Jones closed at 10,717.50

Blue Corner (Bear) Michael Burry

Michael Burry earned a bachelor’s degree in economics from UCLA and an M.D. from Vanderbilt University School of Medicine. While working as a neurology resident at Stanford and later at Lucile Packard Children’s Hospital, Burry practised investing in his spare time. He gained a reputation on online forums (Silicon Investor) for his analysis of value stocks, which led him to leave medicine and start his own hedge fund, Scion Capital, in 2000.

Burry analysed mortgage-backed securities ahead of the Global Financial Crisis (GFC), determining they were highly unstable. As popularised by the book and subsequent film The Big Short, Burry purchased credit default swaps against MBS, allowing him to profit when the housing market collapsed. He reportedly made over US$100 million for himself and roughly US$700 million for his investors.

Scion Capital was closed in 2008, and Scion Asset Management was opened in 2013 and subsequently closed in November 2025. He has since launched a Substack subscription-based newsletter called Cassandra Unchained, where he shares his investment insights.

Burry’s bearish calls have been criticised by observers for being frequently wrong, to which Burry has recently responded, “I got it right in 2000, got it right in 2007,” adding, “Got it right in 2019, helped by COVID, and I called the meme stock crash in mid-2021. I called the bank stock run in 2023. In 2017, I had trouble finding good stocks, and I discussed the passive investing bubble for the first time. I did not say it meant that we would crash any time soon. My case was that crashes would become more correlated and more acute, and 2020’s COVID crash was the most acute, correlated stock market crash in history.”

What are they saying now?

Yardeni v Burry

Yardeni (Bullish)

In economics, the wealth of a nation is built and sustained through production, and that production requires three ingredients: Land, Labour, and Capital. These are the finite building blocks of prosperity. Land provides the raw materials, Labour provides the muscle and the mind to transform them, and Capital represents the tools.

The primary challenge for every society has always been the efficient allocation of, and between, these inherently scarce resources. If you run out of one, growth grinds to a halt. You need all three. That was, it seems, up until recently, when a fourth ingredient – data – was proposed.

The transformative aspect of this fourth ingredient is that, unlike the physical limitations of land or the finite hours of the human workforce, data is a resource that is functionally unlimited. And importantly, it’s the only factor of production that actually grows more abundant the more we use it. Meanwhile, today, artificial intelligence (AI) appears to be an engine that turns raw information into a productive force. One that can boost the efficiency of each of the other ingredients, making workers smarter and capital more effective.

The logic is that because every interaction with AI generates more data, which in turn requires more memory and processing power to analyse, what’s been created is a self-reinforcing growth loop.

While the adoption and embrace of this new way of looking at AI – as a fourth force in production – won’t make the market immune to setbacks, it could very well mean the current stock market rally isn’t just a speculative bubble driven by hype, but a reflection of a structural rebuilding of the global economy.

As of May 11, 2026, in a forecast eerily similar to his 1999 prediction for 2000, Yardeni has raised his 2026 year-end S&P 500 target to 8,250 (up from 7,700), predicting an “earnings-led melt-up” driven by strong corporate profits and artificial intelligence. He remains highly bullish, seeing nearly 12 per cent further upside from early May levels and projecting the S&P 500 will reach 10,000 by 2029.

Burry (Bearish)

Burry is warning that the U.S. stock market – particularly the technology and semiconductor sectors – is experiencing a “parabolic” surge similar to the final months of the 1999-2000 dot-com bubble.

Noting that massive infrastructure spending is occurring despite slowing growth in big tech cloud services, Burry believes the AI-driven, narrow rally has propelled valuations to unsustainable heights, with market concentration mirroring that of early 2000.

Writing on his Substack last Friday, after listening to financial television and radio coverage during a long drive, “Absolutely non-stop AI. Nobody is talking about anything else all day.”

“Stocks are not up or down because of jobs or consumer sentiment,” Burry wrote. “They are going straight up because they have been going straight up…On a two letter [AI] thesis that everyone thinks they understand. … Feeling like the last months of the 1999-2000 bubble.”

Noting the SOX Index is up more than 10 per cent in a week, pushing its 2026 gains to 65 per cent, Burry compared the recent performance of the Philadelphia Semiconductor Index (SOX) with the run-up that preceded the collapse of tech stocks in March 2000.

Burry further contends that tech companies are using accounting tricks to understate depreciation on Graphic Processing Unit (GPU) and server assets, thereby artificially inflating profits. In his Substack in May 2026, he acknowledged his reputation as the “boy who cried wolf” regarding market crashes but stands by his mean reversion framework, saying, “ALL the silliness must go”, and believes a prolonged market-wide selloff is imminent.

Backing his view with his own money, Burry has disclosed that he has recently ramped up bearish bets against the semiconductor sector, specifically buying well-out-of-the-money 2027 put options on the iShares Semiconductor ETF (SOXX). He also holds substantial put options against Nvidia (NVDA) and Palantir (PLTR), betting these high-growth, AI-focused companies will also fall significantly.

A Postscript

It’s worth noting that, based on historical data up to early 2026, the S&P 500 has delivered four consecutive years of greater-than-20 per cent annual returns only once in its history (1995–1998). Were 2026 to deliver the bullish end Yardeni predicts, the 2023-2026 bull run would be the second historical occurrence of four consecutive greater-than-20 per cent annual total returns.

Following the Federal Reserve’s rate-hiking campaign in 2022, both the S&P 500 and Dow Jones posted massive back-to-back gains in 2023 and 2024, but this only marked the first time in two and a half decades that back-to-back 20 per cent+ years occurred. And while back-to-back 20 per cent years have occurred roughly three to four times since 1950 (such as 1954-55, 1995-96, 1996-97, 1997-98, and 2023-24), stretching that performance to four consecutive years is an exceptionally rare event.

For the S&P 500 in 2026, analysts are forecasting an average return of 12 per cent, citing continued earnings growth and resilient consumer demand.

Multiple investment firms, including Goldman Sachs and JP Morgan, expect momentum in tech, AI, and small-cap sectors to drive performance this year.

Goldman Sachs writes, “In 2026, equity markets are expected to deliver positive but more moderate returns, with greater dispersion across sectors and stocks.”

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

Hello Roger

Surely the current US share market can’t be compared to the 2000 tech wreck. The financials of all the big companies look strong, with not excessive PEs. So, we aren’t talking about companies with no revenue or profits, with a vague idea of how they’re going to make money.

The one thing that concerns me is the talk about capital spending. I don’t believe this has ever been used as a measure to buy shares. Yet we continue to hear about how much the big tech companies are spending, as if this should reinforce and reassure everyone that it’s safe to buy. The big question could be: Are they overspending where they end up destroying capital? We’ve seen it before in the resource industry.

Rgds

Wes Horn.