When high tech meets low tech – the commodity crunch behind AI

There’s a thesis many investors are now positioning for: The artificial intelligence (AI) infrastructure buildout being led by the hyperscalers can’t proceed without copper, silver, and other critical metals, such as scandium. Their conclusion is that commodity prices will rocket higher if the the A.I. revolution continues.

Current forecasts suggest the combined capital expenditure of Amazon, Google, Meta, and Microsoft will reach US$715 billion in 2026, up 98 per cent on 2025 and nearly three times their combined capital expenditure (capex) in 2024.

The scale of the AI Buildout has evolved from what was only recently an ambitious corporate goal, to what some are describing as the largest industrial mobilisation in human history.

To give the spending some sense of scale, Amazon’s US$200 billion annual capex is roughly equivalent to the entire Gross Domestic Product (GDP) of countries like Greece or New Zealand. And this is being injected into silicon and steel every twelve months.

In fact, it’s not an exaggeration to say the hyperscalers are treating capex as their new economic ‘Moat’ or competitive advantage.

“I’m willing to go bankrupt rather than lose this race.”- Larry Page, Google Founder

Now, as an aside, there are some accounting shenanigans one should be aware of.

The huge cash sums being injected into data centres and chips will be capitalised and then depreciated over time. The revenues, however, will be booked immediately. So, the profits will look epic and will drive rising earnings per share estimates for the Nasdaq and S&P500 in 2026 and 2027. Behind it, of course, a massive amount of cash is being burned. But no matter.

For now, it all looks great, and the most validating sign for that conclusion is the explosive revenue growth of AI models like Anthropic. Anthropic recently reported US$44 billion in annual recurring revenue (ARR), up from US$9 billion in less than a year, representing a 46.6 per cent month-on-month increase, and roughly US$96 million in new revenue per day.

And keep in mind a significant portion of Hyperscaler spending isn’t just buying NVIDIA H200s or Blackwells; it’s building proprietary silicon too. Microsoft’s Maia 200 (a breakthrough inference accelerator engineered to dramatically improve the economics of artificial intelligence (AI) (token generation) and Amazon’s Trainium3 are now being deployed at “planet-scale” cluster levels to bypass Nvidia silicon margins.

We’re also seeing capex on energy. Microsoft’s deal to restart Three Mile Island and Amazon’s massive nuclear-adjacent data centre acquisitions the spend is expanding to secure the energy grid itself, not just the servers.

Elsewhere, it’s worth noting that US$25 billion of Microsoft’s guidance is attributable solely to component price inflation and supply chain premiums, highlighting how desperate the race for capacity has become.

The old Software-as-a-Service (SaaS) model was built on a ‘per-user, per-month’ pricing and revenue model. That model appears to be under attack by a far superior replacement. Anthropic’s growth, for example, is driven by Agentic AI – autonomous systems like Claude Code that consume tokens at 100x the rate of a human typing into a chat box. But despite the massive compute costs, Anthropic’s inference margins have reportedly hit 70 per cent, suggesting software optimisation and specialised hardware are making AI delivery significantly more profitable as it scales.

That experience probably explains why these companies are comfortable spending more than $600 billion collectively on the transition to Agentic Computing. Unlike Large Language Models (LLMs) that are essentially just smart web searchers, 2026-era agents are performing complex, multi-step workflows (coding entire apps, managing supply chains, conducting research), and 2027-era agents will be apps in the palms of everyone’s hands.

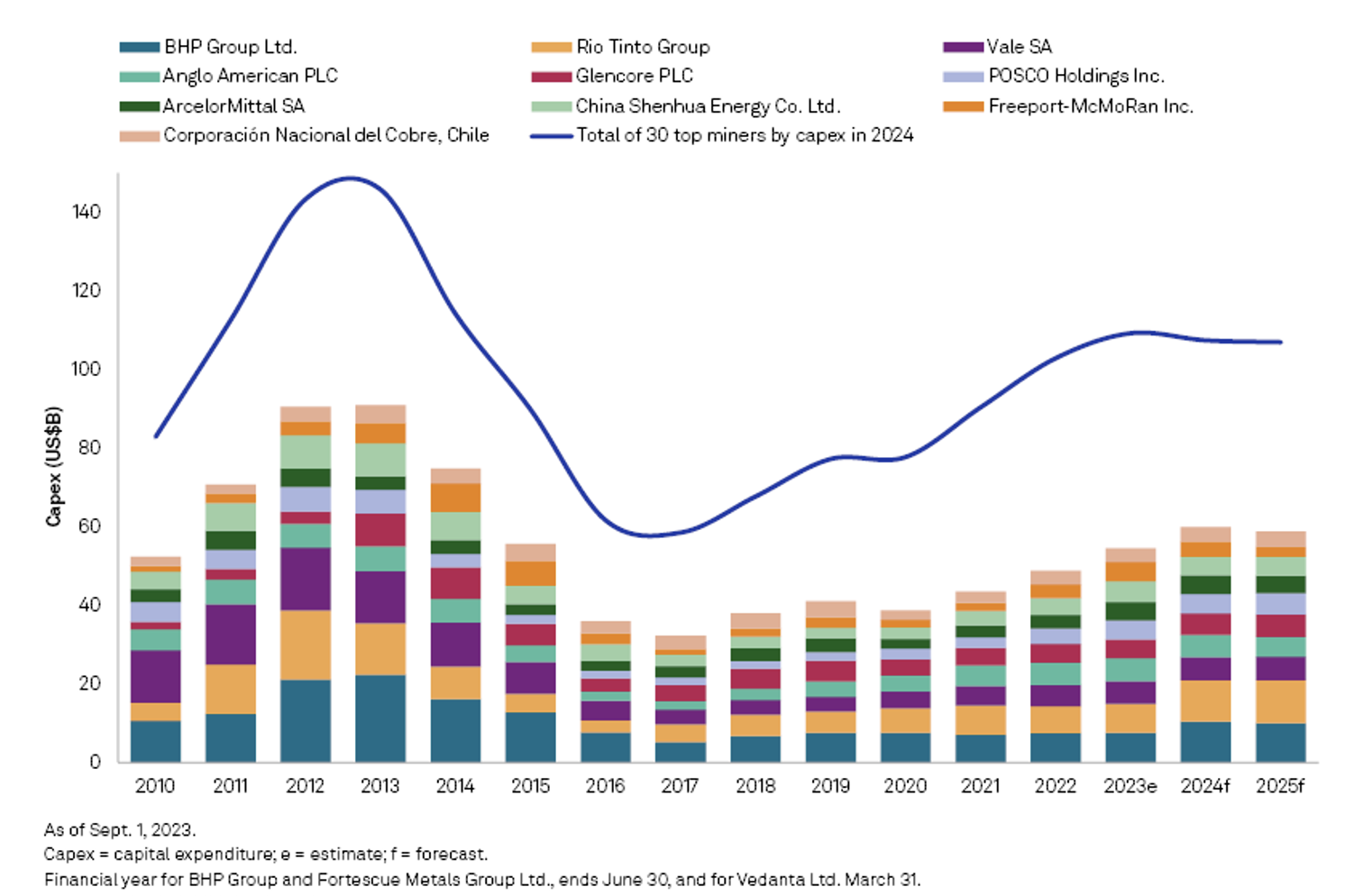

Follow that to its logical conclusion, and a massive bottleneck appears in the supply of copper, silver, and other critical metals because the global mining industry has not been significantly investing in developing new supply for the last 10 to 12 years.

Figure 1. Hey Big Spender, 2010-2025.

Source: S&P Global Market Intelligence

Conclusion

Tech companies are spending hundreds of billions and forecasting hundreds of billions more, but the mining companies they will be relying on to supply the raw materials have not. The only result (if the AI infrastructure boom continues) is for commodity prices to adjust upwards.

And that’s what many investors are positioning for.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.