Planting the seeds: Is this the best high-yield option for 2026?

How to maximise your savings with higher-yield funds with competitive returns and risk.

Looking to make your money work harder this year? Whether you’re looking to fund a better lifestyle, build your nest egg or simply grow some savings, you may want to read this article.

For many retirees – and particularly people who may be navigating their finances independently for the first time – the stock market can feel less like an ‘opportunity’, and more like a rollercoaster you never asked to board. When you are at a stage in life where preserving what you’ve built is as important as growing it, the daily ups and downs of the stock market can keep anyone awake at night.

The traditional “safe” bets, like term deposits, often fail to keep pace with the lifestyle you’ve worked so hard to earn. So, where do you turn when you want the yield of a high-performer but the stability of a fortress?

The answer, I believe, may lie in an asset class that was once the exclusive playground of ultra-high-net-worth families and institutional giants: Private Credit.

Why the “Old Rules” of investing are changing

For decades, the recipe for retirement was simple: a mix of blue-chip stocks and government bonds. But the world has shifted. Banks have become increasingly beholden to conservative regulators, prompting them to scale back lending to high-quality Australian businesses.

This “retreat” by the big banks has created a massive opportunity for savvy investors. By stepping into the shoes of the lender through the Aura Private Credit Income Fund, you aren’t betting on whether a stock price goes up or down tomorrow. Instead, you are earning a consistent “rent” on your money.

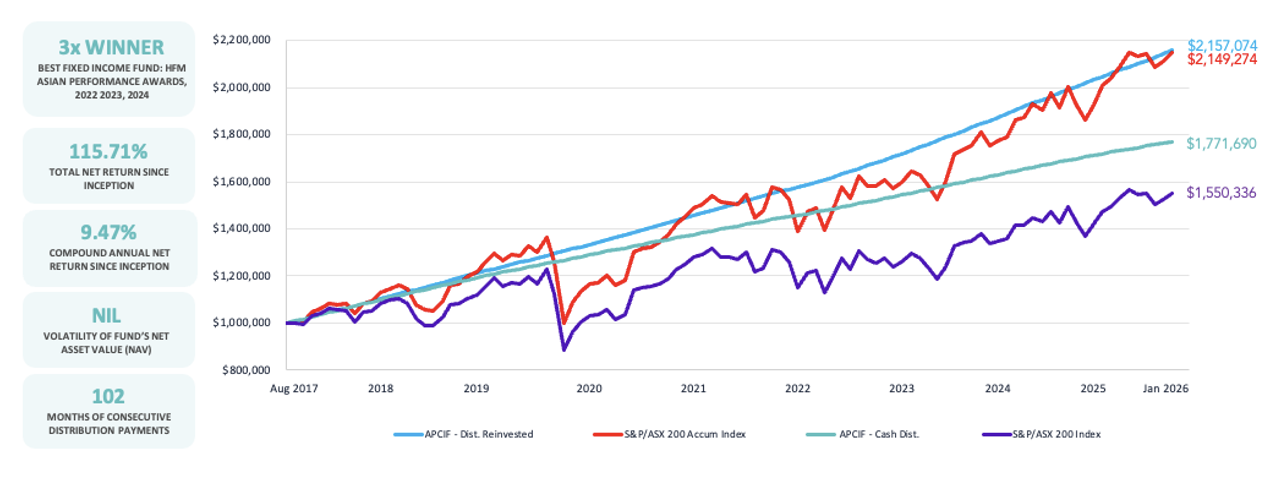

Figure 1. Aura Private Credit Income Fund performance.

Source: S&P/ASX 200 Accumulation Index (^AXJOA) Adjusted Close Historical Data

Source: S&P Global – S&P Australia High Yield Corporate Bond Index Historical Data

Fund inception date 1 August 2017. Returns calculated to 31 January 2026 with all returns calculated net of fees and expenses. Benchmark is RBA Cash Rate + 5%.

Past performance is not a reliable indicator of future performance. Returns and distributions are not guaranteed. The Cash Distribution shown in the chart above represents initial capital invested plus the sum of each of the monthly cash distributions paid to an investor who elected not to reinvest. It does not reflect an investment balance and does not take into account a number of variables such as time value of money or how an investor chooses to use the cash distribution.

The power of being the “Lender,” not the “Owner”

When you buy a share in a company, you are at the mercy of market sentiment. If the market panics, your portfolio drops.

When you invest in Private Credit, you are effectively the bank. Here is why this is particularly compelling for those who value peace of mind:

- Priority of payment: As a lender, you are higher up in the “capital stack” than shareholders. You’re paid your interest before shareholders see a cent of profit.

- Reduced volatility: Unlike stocks, which are priced every second of the day based on emotion, private credit is valued on the underlying strength of the loans. It as the ability to stay steady when the market gets shaky.

- Monthly income: For retirees, cash flow is king. The Aura Private Credit Income Fund and the Aura Core Income Fund aim to provide regular, reliable distributions.

The benefits of including private credit in your portfolio

Adding private credit to a diversified portfolio unlocks a host of benefits that make it an attractive option for investors seeking both stability and income:

- Attractive yields: Private credit offers the potential for strong, enhanced yields, providing a compelling income stream compared to traditional fixed-income investments. Our wholesale offering has generated a compounded annual return of 9.47 per cent per annum over eight and a half years, with no negative months and no capital loss.* Our retail offering has returned 7.26 per cent per annum compounded over a little more than three years, also with no negative months and no capital loss.**

*Aura Private Credit Income Fund returns since its inception on 1 August 2017 to 31 January 2026. Net returns after fees and expenses as at 31 January 2026 and assumes reinvestment of distributions.

**Aura Core Income Fund returns since inception on 4 October 2022 to 31 January 2026. Net returns after fees and expenses as at 31 January 2026 and assumes reinvestment of distributions.

Past performance is not a reliable indicator of future performance.

- Low correlation, resilient returns: Historical data shows private credit returns have low to negative correlation with other asset classes, making it a powerful tool for diversification and resilience in turbulent markets. Our private credit offerings have generated positive returns in all months, including those when the S&P 500 and other stock markets declined.

- Regular income: Through contractual borrower agreements, private credit can offer consistent income, offering investors peace of mind.

- High quality: Not all private credit funds are the same. The retail private credit fund holds an externally assessed S&P Equivalent Portfolio Credit Rating of AA. The wholesale private credit fund holds an externally assessed S&P Equivalent Portfolio Credit Rating of BB+.***

***Portfolio Credit Quality includes cash and is provided by a third-party risk consultant and subject to change. The Fund’s assets are not rated by S&P.

- Low volatility: Because returns are contractually agreed upon, private credit investments are generally less volatile than equities.

- Diversification: Private credit portfolios are highly granular, with exposure to a wide variety of borrowers, assets, industries, and geographies, reducing concentration risk. Each of our funds holds over 10,000 loans across 19 sectors of the economy.

- Robust fundamentals: Unlike public markets, which can be influenced by sentiment-driven momentum, private credit prioritises borrower quality, collateral strength, and repayment likelihood, ensuring a capital preservation-first approach.

Expertise in private credit

With deep expertise in credit, non-bank lending, and specialty finance, the investment philosophy centres first on aiming to protect investor capital while, secondly, generating regular income. The proven track record speaks for itself: with an unbroken history of positive monthly returns.

Why the Aura Private Credit Income Fund and the Aura Core Income Fund?

At Montgomery, we look for investments that offer a “margin of safety.” The Aura funds embody this through highly diversified portfolios of small- and medium-sized enterprise (SME) loans.

But Aura don’t just lend to anyone. The funds focus on senior secured debt. This means the loans are secured by assets, providing a buffer that protects your initial investment. For someone navigating their financial future alone or a couple looking to protect their nest egg, this layer of protection, along with diversification, is vital.

“You don’t need to be a stock market wizard to achieve professional-grade returns. You just need to shift your perspective from the volatility of ‘ownership’ to the steadiness of ‘lending’.”

Is 2026 the time to simplify your strategy?

If you are tired of checking the financial news with a sense of dread, it might be time to look beyond the stock market. Private credit offers the opportunity to generate a target return that could potentially outperform cash and bonds, without the stomach-churning swings of public markets.

We believe the Aura Private Credit Income Fund and the Aura Private Credit Income Fund aren’t just investments; They’re strategies for financial independence and, more importantly, for a good night’s sleep.

Interested in learning more? Enter your details below to speak to a member of our team:

Disclaimer:

You should read the relevant Product Disclosure Statement (PDS) or Information Memorandum (IM) before deciding to acquire any investment products.

Past performance is not a reliable indicator of future performance. Returns are not guaranteed and so the value of an investment may rise or fall.

This information is provided by Montgomery Investment Management Pty Ltd (ACN 139 161 701 | AFSL 354564) (Montgomery) as authorised distributor of the Aura Core Income Fund (ARSN 658 462 652) (Fund). As authorised distributor, Montgomery is entitled to earn distribution fees paid by the investment manager and may be issued equity in the investment manager or entities associated with the investment manager.

The Aura Core Income Fund (ARSN 658 462 652)(Fund) is issued by One Managed Investment Funds Limited (ACN 117 400 987 | AFSL 297042) (OMIFL) as responsible entity for the Fund. Aura Credit Holdings Pty Ltd (ACN 656 261 200) (ACH) is the investment manager of the Fund and operates as a Corporate Authorised Representative (CAR 1297296) of Aura Capital Pty Ltd (ACN 143 700 887 | AFSL 366230).

You should obtain and carefully consider the Product Disclosure Statement (PDS) and Target Market Determination (TMD) for the Aura Core Income Fund before making any decision about whether to acquire or continue to hold an interest in the Fund. Applications for units in the Fund can only be made through the online application form that accompanies the PDS. The PDS, TMD, continuous disclosure notices and relevant application form may be obtained from www.oneinvestment.com.au/auracoreincomefund or from Montgomery.

The Aura Private Credit Income Fund is an unregistered managed investment scheme for wholesale clients only and is issued under an Information Memorandum by Aura Funds Management Pty Ltd (ABN 96 607 158 814, Authorised Representative No. 1233893 of Aura Capital Pty Ltd AFSL No. 366 230, ABN 48 143 700 887).

Any financial product advice given is of a general nature only. The information has been provided without taking into account the investment objectives, financial situation or needs of any particular investor. Therefore, before acting on the information contained in this report you should seek professional advice and consider whether the information is appropriate in light of your objectives, financial situation and needs.

Montgomery, ACH and OMIFL do not guarantee the performance of the Fund, the repayment of any capital or any rate of return. Investing in any financial product is subject to investment risk including possible loss. Past performance is not a reliable indicator of future performance. Information in this report may be based on information provided by third parties that may not have been verified.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.