Does a lower price mean the shares are cheap?

Following on from our recent blog post here and our Head of Research, Tim Kelley’s video blog – on the changing supermarket industry landscape – we are naturally watching the developments in the sector closely (from the sidelines), taking a keen interest in the half year result reported this week by Metcash Limited (ASX:MTS).

To quickly summarise: their half year results showed continued deterioration to which the market has reacted accordingly, with their share price down circa 27 per cent since.

What was perhaps most surprising was the rate of the structural decline. And if it wasn’t before, it is now clear for all to see that that being stuck between the two large Aussie retailers (Woolworths and Coles) and the new German operators in Aldi, is an unpleasant place to be.

At the top-line, sales revenue increased just 1 per cent on the prior corresponding period, a relatively poor showing especially given the contributions from MTS’ liquor, Mitre 10 and Autobarn divisions which all showed pleasing sales results. These segments however contribute just 32 per cent of sales revenue to the overall group, and whilst their trends are positive they are not material enough to make a difference to performance.

The other 68 per cent and the more meaningful contributor is MTS’s Food & Grocery (MFG) division and its here that it becomes uncertain as to how far earnings need to fall before they rebase and stabilise.

On a stand-alone basis, MFG reported a sub-par 0.5 per cent increase in total sales despite category inflation of +3 per cent. Further, this was a period in which IGA in particular had two key tailwinds – a significant reduction in fuel discounting by the majors and higher price inflation in tobacco given an increase in Government excise (taxes).

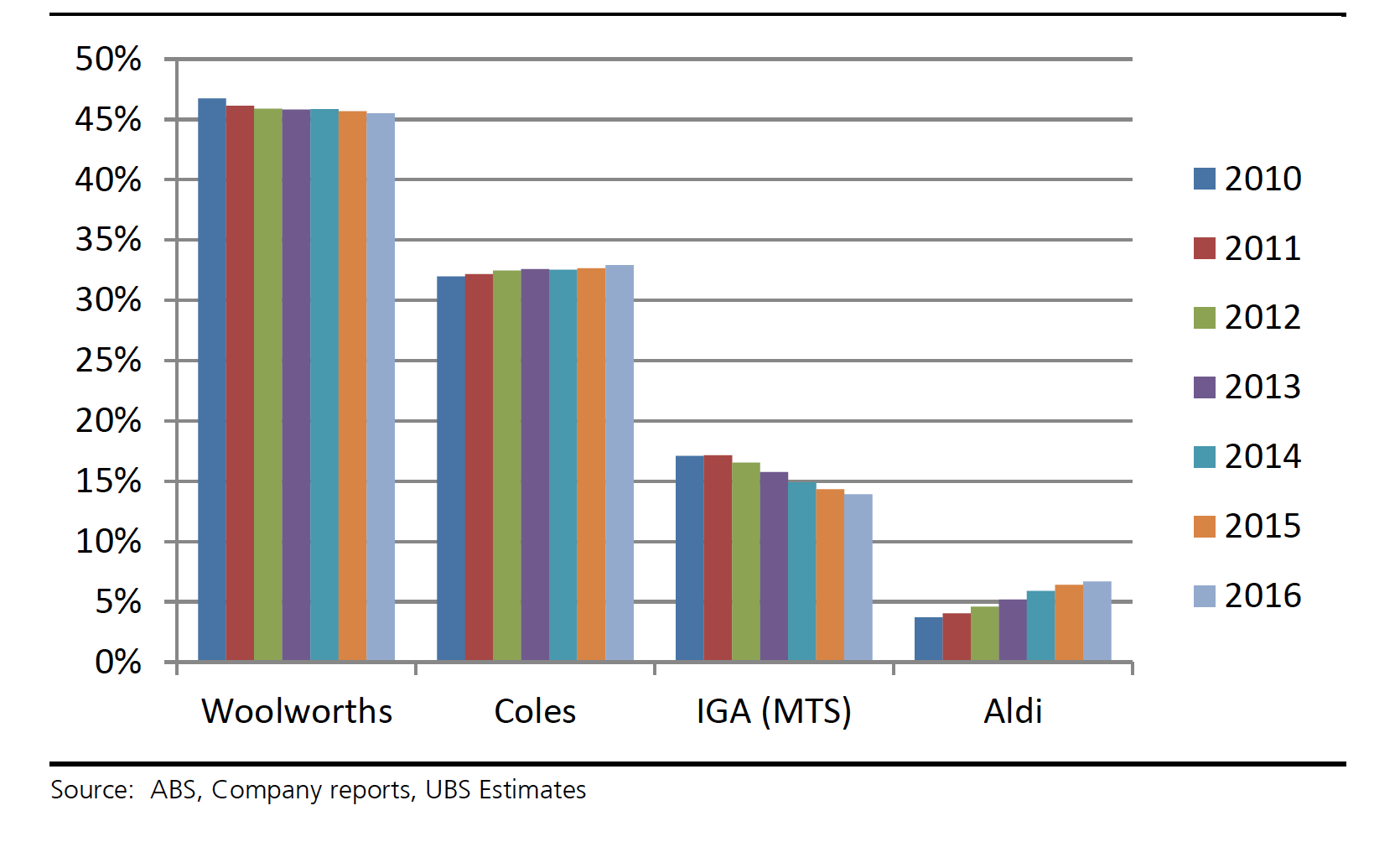

The upshot of all this, is it appears to us that Metcash continues to lose market share and as we show below, it is a trend that is now well established.

With sales growth failing to match cost growth – costs for Metcash are rising at a faster rate than revenues – underlying earnings per share declined 10.2 per cent, which obviously needs to be arrested if the share price is ever to recover.

But it’s here that we note that the future outlook is becoming less certain. The first-half dividend has been cut to just 6.5 cents per share, the lowest level since the same period in 2007.

A few analysts have pointed to the decline in this half as being accelerated by a ramp up in investment, interestingly, one of the biggest points of restructure is a new marketing theme to be implemented by Metcash termed “price match” – which basically means the business will simply match any of its competitor’s prices.

From our prior research into the ‘Aldi’ effect, this will ultimately just continue to drive down prices (which good for consumers) and play right into the hand of the German operators whose retailing format is up to ~60 per cent more efficient already. This is also perhaps the very reason why the independents which include IGA, for example, are considered the soft underbelly of the Australian supermarket industry and those likely to suffer from increasing competition (price discount war) first before the majors.

We also note that Aldi has plans to enter Western Australia and South Australia from late 2015, so it’s a trend that continues to gather momentum and like anything that’s building up speed, it becomes harder and harder to stop.

And because of that, despite the large fall in their share price, longer-term Metcash shares look anything but cheap.

Russell Muldoon is the Portfolio Manager of The Montgomery [Private] Fund. To invest with Montgomery, found out more.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY