Are we seeing a dissonance between credit markets & broader equity indices?

UK Macroeconomic Strategist Michael Wilson has penned an interesting piece entitled “Involution” which came across my desk. It was interesting enough that I thought it worth sharing in its entirety.

Involution

Involution is what happens to your muscles when you spend too much time in space. Without the discipline of pushing against gravity, they wither away and become incapable of doing productive work. What happens to human beings at zero G also happens to the global capital stock at zero rates. It withers away. When there is no discipline to make a return above zero, returns fall to zero.

The problem is that deteriorating returns tighten liquidity conditions, even with low rates. That’s because deteriorating returns change corporate behaviour.

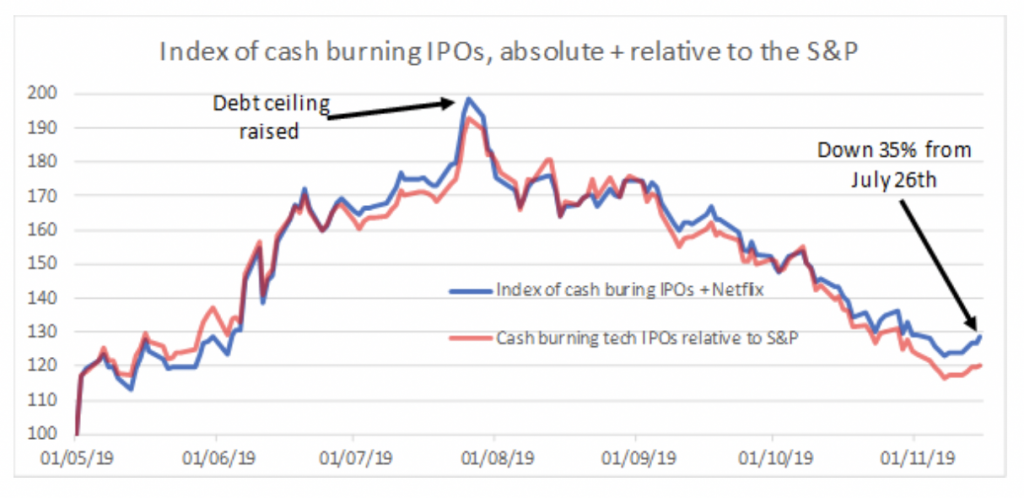

It was the dissonance both between credit markets & broader equity indices and within equity markets that gave away the 2001 & 2008 market downturns ahead of time. That dissonance is returning today. We are seeing it in leveraged loans, in high yield energy spreads & spreads for highly levered companies. We are seeing it in the performance of the recent IPOs of cash burning tech stocks. And we are seeing it in VC funding and the fortunes of WeWork & Softbank.

The ensuing funding squeeze will force these companies to run for cash. With financialised demand now at 9-11 per cent of US GDP on my estimates, it is easy to see how this might trigger an investment recession and an end to the cycle. Fears of a Warren presidency may accelerate the process.

If US corporates switch from growing borrowing by 5 per cent to shrinking it by 5 per cent, it will take US$2 trillion of liquidity out of the system, 10x more than the Fed can inject by cutting to zero by the end of 2020. Whether corporates collectively run for cash or carry on as usual will determine whether the cycle ends in six months, two or four years. My view is that that the cycle ends sooner rather than later.

For more from Macrostrategy Partnership visit: http://www.macrostrategy.co.uk

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

Maybe someone with a background in finance can correctly interpret the above piece.

To my untrained economic brain it sounds awfully like the world economic system is terminal?

And as he puts it getting there ‘sooner rather than later.’