Chipping in – Is exciting ‘safe’?

Inside every smartphone, laptop, PC, smart speaker, smart TV, digital camera, USB flash drive and gaming console is a memory chip. And then there are industrial, medical and military applications. As an aside, Dramatic Random Access Memory (DRAM) and Not And (NAND) are the high-volume, commodity memory semiconductor components, working together in every device. DRAM requires power and manages your data, while NAND, which does not require power, stores your data.

For years, even decades, nobody thought about these chips. They were unseen and also abundant, cheap, and commoditised (maybe they still are), resulting in cycles. Indeed, the recent history of memory chip demand has experienced three major cycles. The first was from 1993 to 1996 as computer demand boomed. The next cycle was driven by the transition to 4GB, 6GB, and 8GB RAM in smartphones between 2016 and 2019, and the most recent cycle was fuelled by the work-from-home boom during the pandemic between 2020 and 2022, which saw demand for smartphones plunge, but this was more than made up for by an eruption in TV, gaming, PC and datacentre demand for memory.

Today’s boom, which began in 2024, was largely unexpected and is all artificial intelligence (AI) driven. The dawn of AI has created a need for large volumes of compute, which requires logic chips such as graphics processing units (GPUs) and central processing units (CPUs) to power key AI tasks. But GPUs and CPUs aren’t the only ingredient AI requires. Memory and storage are the other main ingredients, and AI data centres have become enormous customers of memory chips, pressuring supply and driving prices higher.

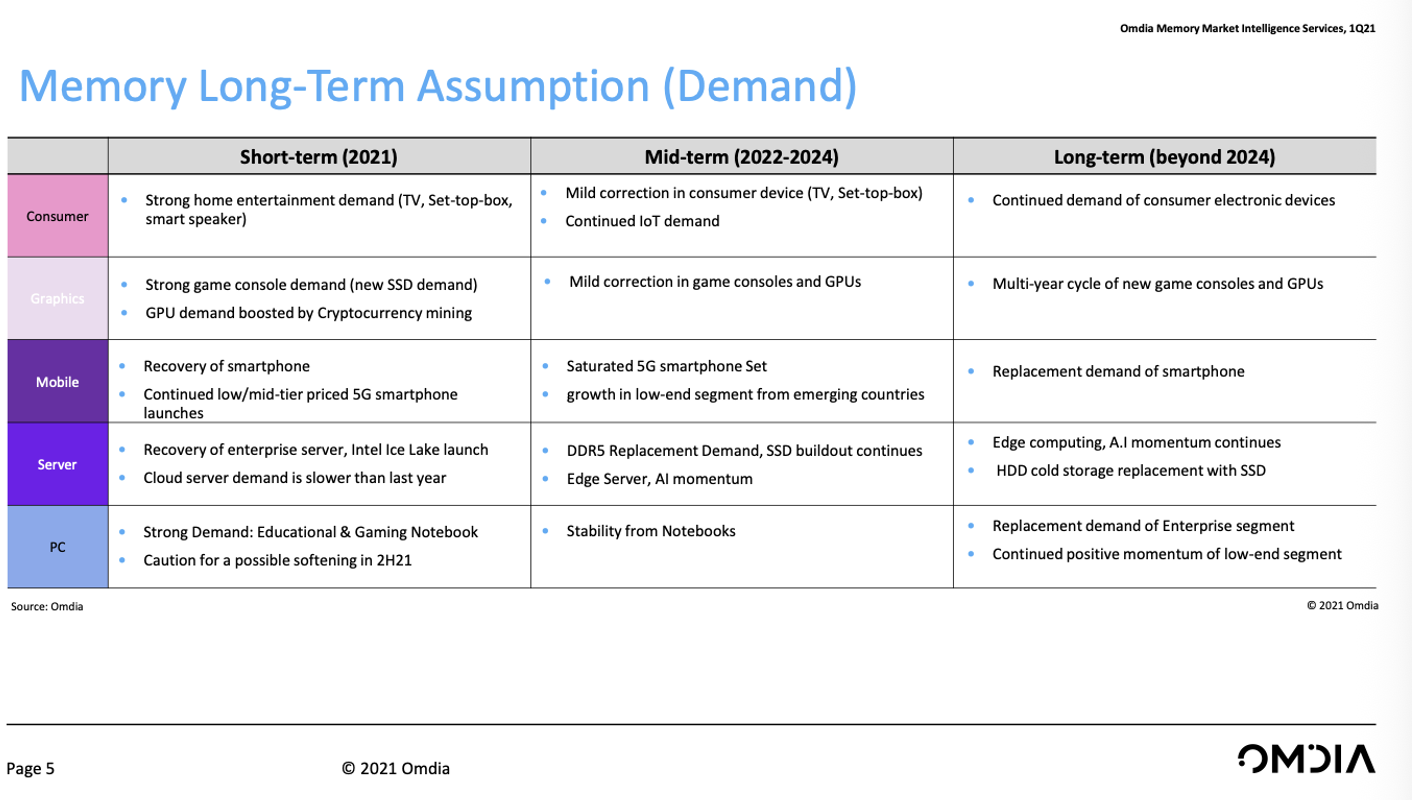

As Figure 1, a slide from a 2021 presentation on memory demand by global technology researcher Omdia (1), reveals, analysts in 2021 knew AI was coming, but its impact on memory demand was not considered a standout.

(1)Omdia promotes itself as combining “the expertise of more than 400 analysts across the entire technology spectrum covering 150 markets and publish over 3,000 research reports annually, reaching over 14,000 subscribers, and covering thousands of technology, media, and telecommunications companies. Our exhaustive intelligence and deep technology expertise allow us to uncover actionable insights that help our customers connect the dots in today’s constantly evolving technology environment and empower them to improve their businesses – today and tomorrow.”

Figure 1. Omdia 2021 memory demand assumptions.

Source: https://www.semiconductors.org/wp-content/uploads/2021/02/Highest-Volume-Mainstream-Memory_Omdia.pdf

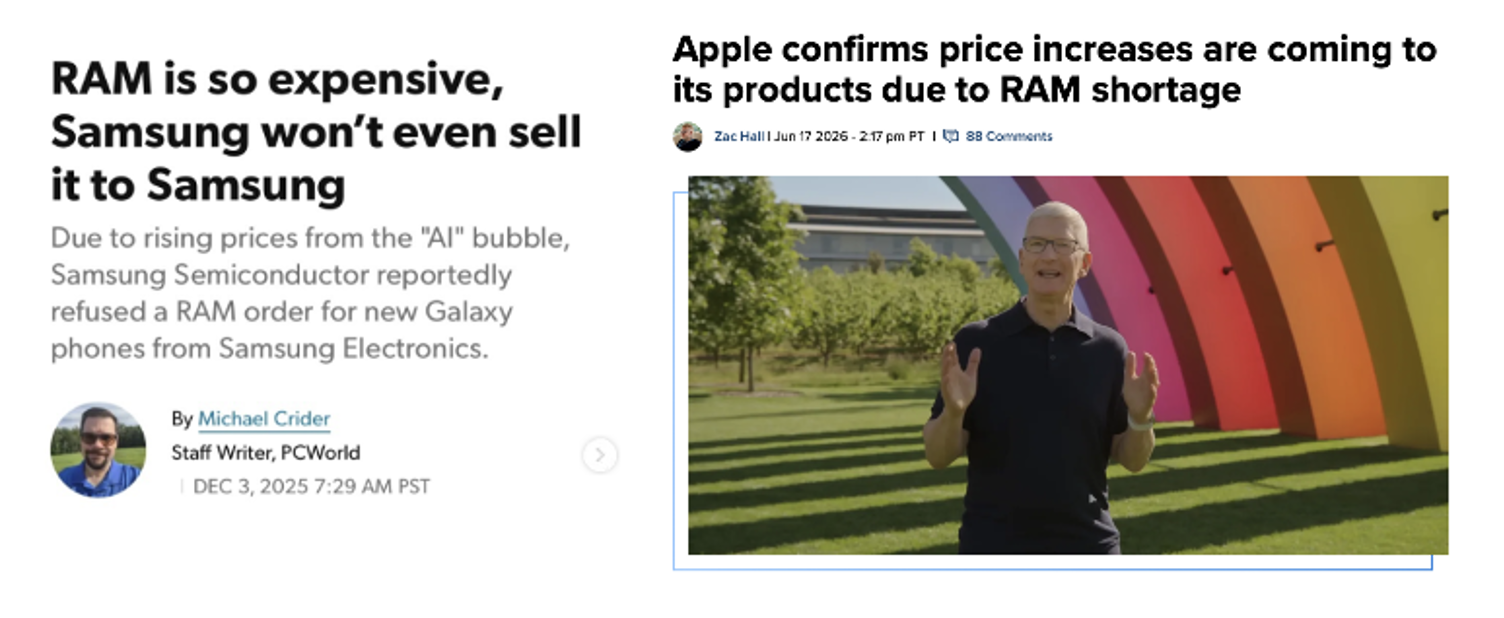

Since 2025, a global shortage of computer memory has emerged due to supply constraints and rising prices in the semiconductor memory market, especially affecting DRAM and NAND flash circuits.

Media outlets have dubbed the crisis “RAMmageddon” or the “RAMpocalypse”, with the current shortage fueled by the deliberate shift of manufacturing capacity toward more profitable AI data centre products.

Consequently, RAM prices are skyrocketing. Given a single AI server can use up to 2TB of RAM, which is the equivalent of hundreds of PCs/ phones worth of RAM, memory manufacturers are prioritising these AI companies over consumer product demand, so supply constraints are forcing consumer RAM prices amid constrained supply.

Figure 2. Recent headlines

Source: PCWorld, 9to5Mac

Why investors are excited

Understandably, this has significantly benefited memory chip manufacturers, for whom demand has surged, leading to notable growth in earnings and stock prices.

For example, in the most recent quarter, chip manufacturer Micron’s revenue surged by 346 per cent, hitting US$41.5 billion. This exceeded expectations by US$5.6 billion, and their data centre gross margin was 87 percent – more than twice that of the same period last year!

Operating cash flow reached US$25.4 billion, a 451 per cent increase year-over-year (YoY). Adjusted free cash flow grew to US$18.3 billion from only US$1.9 billion the previous year, without an increase in chip sales. In fact, volumes increased only slightly, in the low single digits. Meanwhile, DRAM prices surged over 60 per cent in the quarter, and NAND prices climbed roughly 84 per cent.

Micron and its peers, Samsung Electronics, SK Hynix, Kioxia and SanDisk are making hay while the sun shines, selling all the chips they can manufacture even after raising prices massively.

And that’s what’s making investors excited.

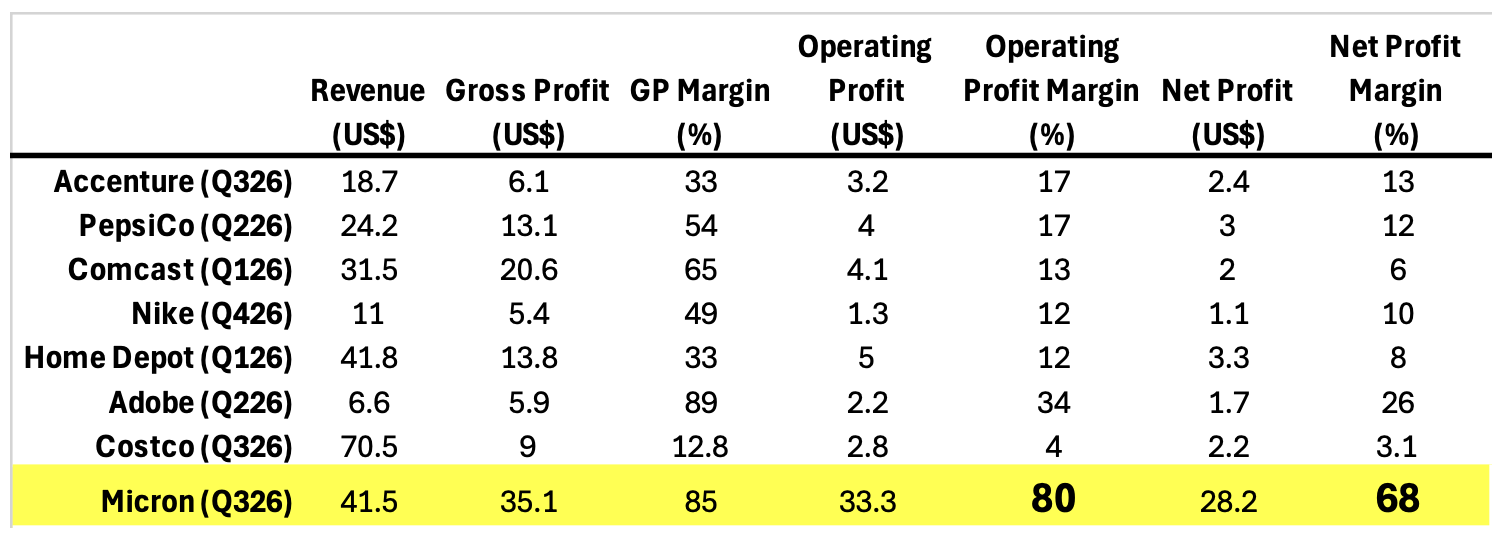

Table 1. Margin comparisons

As Table 1., reveals, few companies can generate the same proportion of ‘take-to-the-grocery-store’ profits from revenue. While Comcast owners can keep just six cents of every dollar of revenue generated and Home Depot owners just eight cents, Micron investors in the last quarter kept almost 70 cents of every dollar of revenue. And it’s not just the proportion of revenue that Micron owners can keep that’s exciting; it’s the quantum. Micron generated more Net Profit nominally than all the other companies in Table 1., combined.

Investors expect limited chip supply to continue well past 2027, driven by strong AI demand from data centres and also from new AI features in smartphones that require significant memory (often 12GB to 24GB) to run smoothly.

The questions for investors to answer, amid Micron’s 690 per cent share price increase over the last year, include, 1) Whether demand for DRAM and NAND chips has, in the infamous 1929 words of Yale economist Irving Fisher, reached “a permanently high plateau”, or whether chip demand will revert to the cyclicality of the past, and therefore 2) Whether there is a bubble in revenues, if not also in share prices?

Micron’s share price has already declined 23 per cent from its share price high on 25 June 2026, wiping US$313 billion from its market capitalisation in less than three weeks. And this is despite the shares trading on a trailing price-to-earnings (P/E) of ‘just’ 27 times at the highs, for a company that grew revenues in the last quarter by 346 per cent YoY and net profits by 48 per cent.

The bottom line is simple. Now, on a trailing P/E of ‘just’ 21.21 times, an investor must decide if the band will keep playing (growth can continue) long enough to draw revellers back to the party. For that to happen, those revellers also need to feel ‘safe’ about growth continuing. Perhaps investors are reduced to guessing what other investors will guess! And that doesn’t sound safe.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.