Yardeni pivots again and again

Pivots galore

Few global macroeconomists have carried as much recent optimism as Ed Yardeni, who, as president of Yardeni Research, has spent the better part of this decade championing a ‘Roaring 2020s’ thesis – a nod to the roaring 1920s, on the back of productivity gains, technological innovation, and a resilient American consumer, Yardeni’s thesis has included a very bullish end to 2026.

In an interview with Thoughtful Money, however, Yardeni pivoted. While not abandoning his longer-term bullish base case entirely, the war in the Middle East, seems to have influenced a bit of a capitulation. He has also increased his probability of a recession from 20 per cent to 35 per cent, on the back of geopolitical volatility and the return of ‘bond market vigilantes’ – the latter being a term Yardeni famously coined in the 1980s to describe investors who protest inflationary fiscal policy by selling bonds.

Yardeni’s current concern stems from the unpredictability of the Middle East conflict. While initial military successes might suggest a ‘decapitated’ Iranian regime, the reality of a state built on what he terms “professional terrorism” means that command-and-control disruptions do not necessarily end the threat.

Indeed. I would go further and suggest Trump’s actions have inspired, anew, generations of people who hate the West and the U.S. in particular.

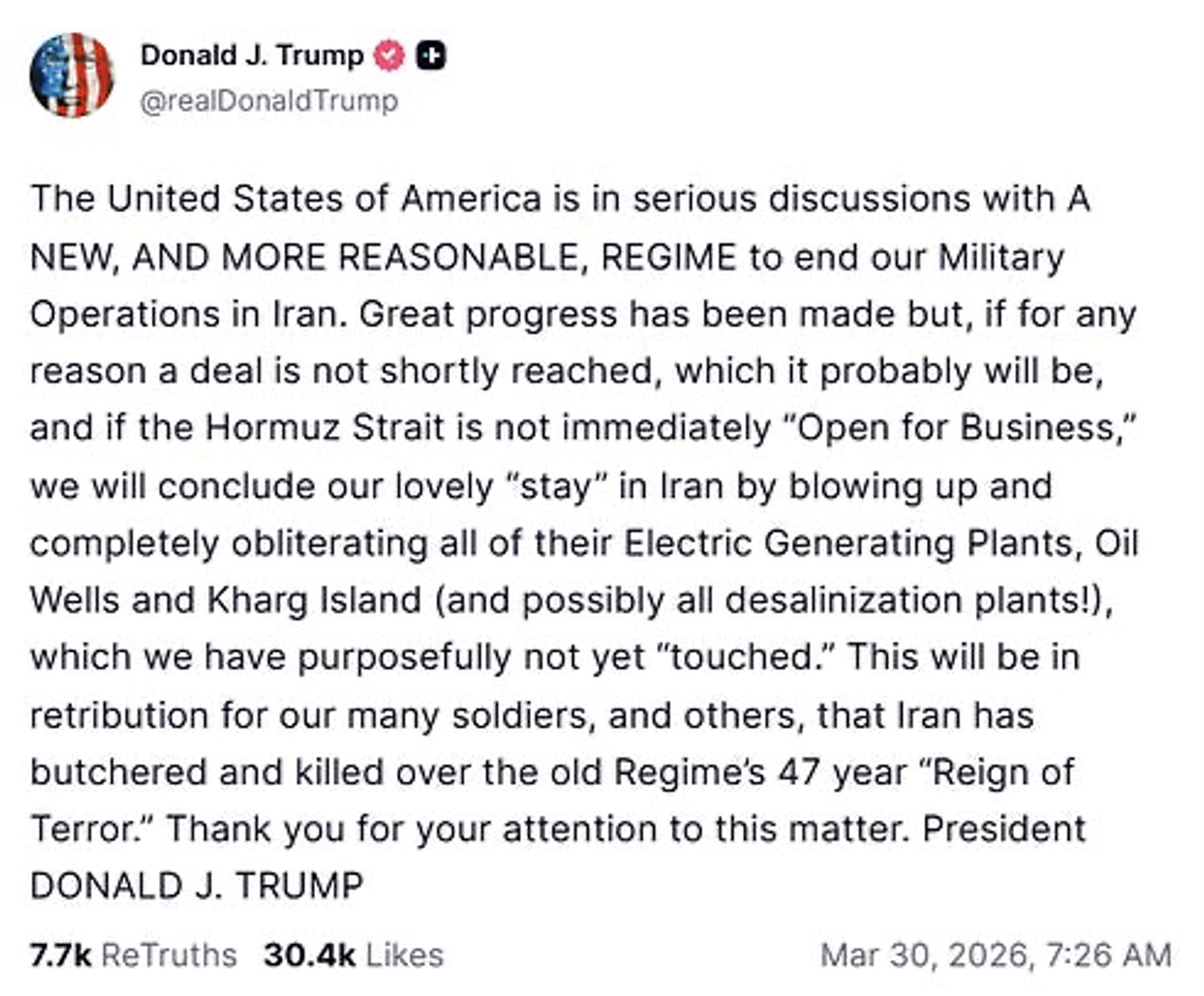

At the time of the interview, Yardeni did not have the benefit of Trump’s latest Truth Social Post.

Figure 1. Trump on Truth Social

Source: Truth Social

In response to, or perhaps in spite of, Trump’s post, it might be worth adding that several news outlets have said a 3rd U.S. aircraft carrier is on its way to the Middle East, something rarely done for show.

Yardeni noted that with hundreds of thousands of Revolutionary Guard members and a proliferation of drone and missile technology, a swift resolution is far from guaranteed.

Military history is littered with air campaigns that failed to achieve their ultimate objectives without boots on the ground, a scenario that currently remains less probable but looming.

The biggest losers – beyond the human tragedy – are global growth forecasts. The longer the conflict persists, the more corrosive its effects become on the global economy.

Yardeni has also joined the band of economists concerned about stagflation, which I wrote about in a recent article on the blog: The Australian – The ghost of the 1970s oil crisis looms large. Now, according to Yardeni, if the war drags on and with the Strait of Hormuz being a vital maritime choke point for 20 per cent of the world’s oil supply, the global economy could face a stagflationary “lost decade” for stocks, reminiscent of the oil-shocked period fifty years ago.

We know that even as the market bounces on the prospect of an end to the conflict, investors are conflating an end to hostilities with a smooth reopening of the Strait. But if this artery remains constricted, even after the war ends, the resulting oil price shock acts as a regressive tax on consumers worldwide, potentially forcing a retrenchment in spending that tips a fragile global recovery into a full-scale recession.

Yardeni notes the 2022 Russia-Ukraine invasion showed initial fears of soaring food and energy prices eventually gave way to a rapid cooling of inflation, which might suggest today’s global economy may be more adaptable than it was in the 1970s.

One of the most compelling arguments Yardeni makes for American resilience is the fundamental shift in the United States’ energy profile. Unlike the 1970s, when the U.S. was precariously dependent on foreign crude, the nation is now largely self-sufficient.

This energy independence serves as a strategic buffer for the U.S., reducing the economy’s energy intensity and potentially turning a global crisis into a domestic opportunity. As Middle Eastern supply becomes compromised, global demand for more reliable American energy exports– particularly Liquefied Natural Gas (LNG) – could surge. Maybe that was Trump’s game plan all along?

Yardeni notes the damage to LNG production facilities in places like Qatar could take half a decade to repair, further cementing the U.S. as the world’s primary energy fortress.

And it is also worth remembering LNG production is inextricably linked to the supply of helium, a critical component in semiconductor manufacturing.

Yardeni adds that while stock prices have corrected and price-to-earnings (P/E) multiples have compressed, equity analysts remain stubbornly optimistic about corporate earnings.

Yardeni watches forward earnings as an indicator of economic health, noting forward earnings correlate strongly with real Gross Domestic Product (GDP) growth. As long as technology giants like Nvidia continue to report robust artificial intelligence (AI)-powered earnings, and as long as industrials show resilience, the “Roaring 2020s” scenario remains his base case with a 60 percent probability.

He suggests that we are currently in a 10 to 15 per cent market correction, which will prove to be “stress test” that may once again surprise bears who have long predicted a recession.

On the subject of handling Iranian oil exports, Yardeni and Taggart discussed the idea of the U.S. moving from sanctions to active confiscation – essentially seizing Iranian tankers outside the Strait of Hormuz and selling the oil to China, with the proceeds held as reparations. If it occurred, it would create an economic chokehold on Iran without the political and human nightmare of boots on the ground. It would also serve as a warning to China, which remains heavily dependent on Persian Gulf oil. By demonstrating the U.S. can control the flow of energy to the Indo-Pacific, Washington gains significant leverage in broader geopolitical tensions, including those surrounding Taiwan.

Conclusions

I think it’s Yardeni’s “bond vigilantes” that will prove the ultimate arbiter of this new era. Yields on U.S. 10-year Treasuries have climbed toward 4.5 per cent as investors demand a higher premium to reflect the inflationary risks of war and the mounting defence spending that follows. And if fiscal stimulus is used to offset the recessionary impact of high energy prices, the vigilantes may tighten credit conditions further, creating a self-fulfilling economic cooling.

Yardeni maintained his year-end S&P 500 target of 7,700 (an 18 per cent rally from current levels), though he admits investors will need a “neck brace” to survive the whiplash.

My view? Returns from here will depend on whether supporters of an inflationary or stagflationary view of the economy from the Middle Eastern war win out against those who believe in the deflationary, productivity-enhancing power of AI.

For now, Yardeni is betting that American resilience and technological progress will win out. But as another analyst noted, “the potential for disruption to energy supply chains and global shipping routes make this conflict one with wider implications for global markets”. And as Luke Gromen recently observed, “Iran is not attempting to defeat the United States military, which it clearly cannot do. Instead, Iran is trying to challenge the United States Treasury market.”

So, keep an eye on the bond yields and tanker movements in the Gulf. And for the latter, the leading indicator will be insurance premiums on large tankers falling from the current 4-10 per cent of value to circa 2 per cent.

*The latest update:

In less than 12 hours from the Thoughtful Money Interview, Yardeni might have already pivoted again. In a post to clients received at 2:26pm AEDT, Yardeni wrote: “Today’s powerful relief rally in the stock market was fueled by news that President Donald Trump intends to declare victory in the war with Iran, according to an article in this morning’s Wall Street Journal. Around noon, the market moved higher still on a report that the President of Iran said his country is ready to end the war if the U.S. agrees to its 5-point peace plan. Then, after the market closed, around 6:30 pm EST, Trump told reporters that the U.S. would be leaving the war zone in 2-3 weeks. His press secretary announced that the President will deliver a formal Address to the Nation Wednesday night at 9:00 pm. He certainly won’t be accepting the Iranian plan, and he seems ready to withdraw without Iran accepting his 15-point plan, which includes opening the Strait of Hormuz,” adding, “If Trump is declaring mission accomplished, then so are we regarding our stock market correction call. We will probably lower our recession odds from 35 per cent back to 20 per cent once we have a better handle on whether the conflict in the Persian Gulf is actually over.”

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.