Why the right investment framework is important

We recently published a blog post I wrote entitled, ‘Why I think tech and small caps could rally this year’. In that post I explained the unreasonableness of the interest rate market’s expectations of more than three rate cuts by the end of January 2024.

Citing the U.S. Federal Reserve Chairman Jerome Powell’s own comments that he is not forecasting recession, as well as the improbability the U.S. inflation rate will plunge far enough, or unemployment will rise fast enough to prompt the Fed to cut rates, I concluded the equity market, and in particular technology and small-cap stocks, could rally on the back of a combination of economic growth and disinflation.

In this blog we pour more coals on the head of rate cut expectations noting the Fed has been extremely ineffective at slowing employment growth with the blunt hammer of monetary policy and rate hikes.

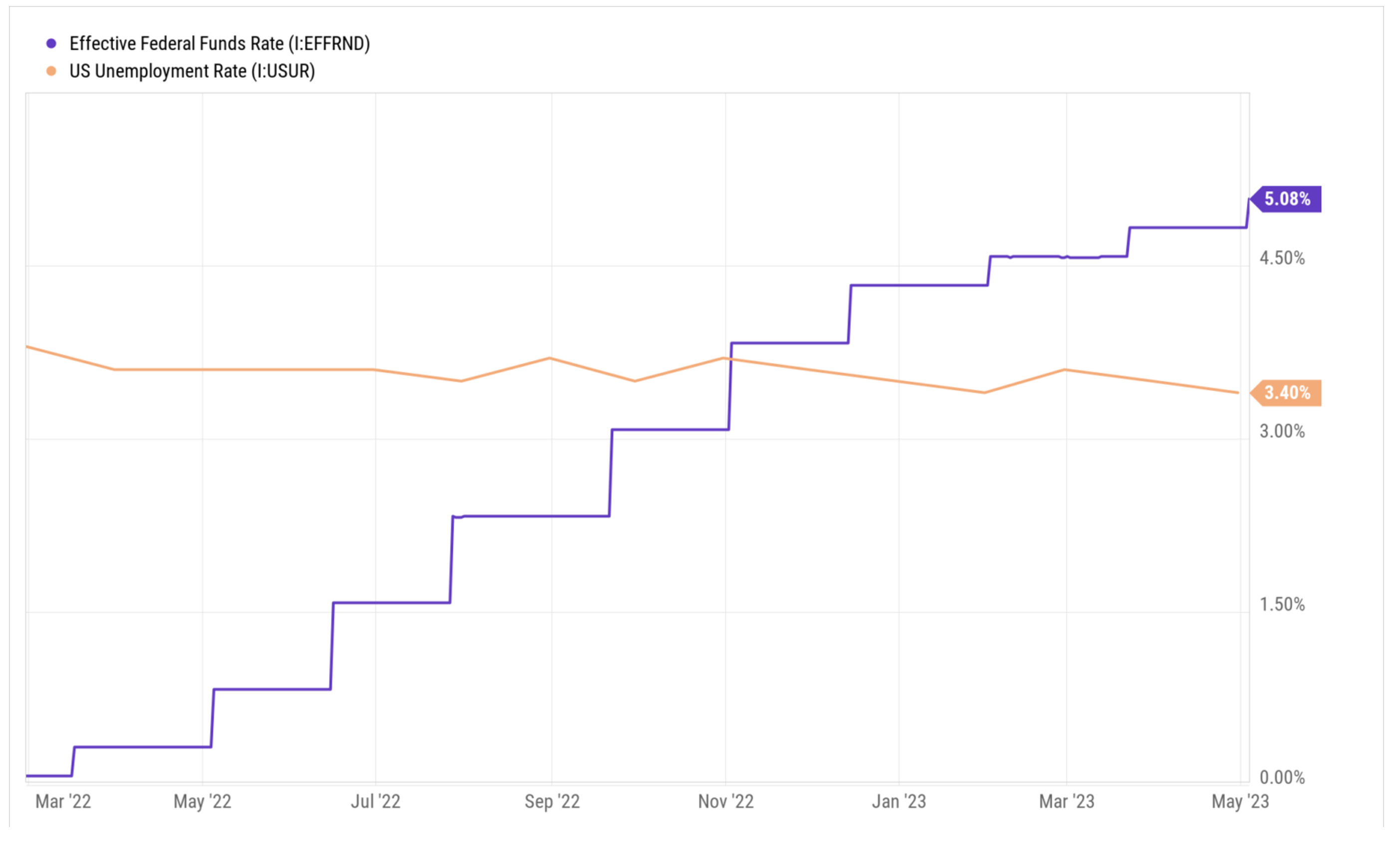

Figure 1. U.S. Federal Reserve rate hikes alongside unemployment

Figure 1. reveals the U.S. Federal Reserve’s rate hikes have been ineffective at quelling demand for labour. For the economy to ease enough for inflation to slow, a higher unemployment rate is at least one of the necessary requirements. It certainly seems to be one of the aims of the Fed.

But it’s not working. In the period the U.S. central bank raised rates from its target range of 0-0.25 per cent as recently as February 2022, to its current target of 4.75-5.25 per cent, the unemployment rate has fallen from four per cent to 3.4 per cent.

Think about that. Despite the Fed raising rates at its fastest rate in history, unemployment has fallen. A cynic might suggest that when inflation was declining, rate cuts did nothing to stop the decline, and now rate hikes are contributing relatively little to the quest to bring inflation down.

It seems to me however, the COVID pandemic justified a cut in the Fed Funds target from 1.50-1.75 per cent to 0-0.25 per cent because unemployment jumped from just 3.5 per cent in February prior to the outbreak of the virus, to a peak of 14.7 per cent just two months later. But that lower bound interest rate target remained in place for just a month shy of two full years.

As one commentator pointed out the U.S. economy added almost five million jobs last year and has added more than a million jobs thus far in calendar 2023 and that’s alongside the prime-age labour force growing to an all-time high of 106.5 million people.

Perhaps the point of all this is that as investors, there are only a few things we can control. We can control our temperament, the framework we adopt for our investing and the discipline with which we invest. We have written extensively about all of those requirements on our blog. We cannot however control whether interest rates rise or fall, whether a recession is around the corner, what the government will do in its annual budget, or the direction of markets.

The uncontrollable however probably matter far less. Your long term returns will be sound if you have the right framework and temperament, irrespective of whether the Fed is successful in fighting inflation and employment.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

Why would the Fed (and likewise, our own RBA) raise rates even more when the US Government already owes $7.3 trillion, isn’t that a bit of ‘shooting yourself in the foot’ ? But then again, nothing would ever surprise me. If it was China, they would say to the Reserve Bank “you will not raise rates” but saying that, that brings it’s own problems when you are trying to contain inflation, but that doesn’t matter in the quasi world of China where GDP, inflation and whatever else is “what we say it is”.

Hey Chris, the central banks are separated from the government and act independently.