Why Centuria Capital is a beneficiary from the flood of liquidity into markets

One theme we continue to follow is the impact of the ongoing flood of liquidity being provided to financial markets and the impact it is having on the value and demand for income generating assets.

The share prices of property managers have generally been strong over the last 12 months on the back of this thematic. The benefit of owning the property manager rather than just owning the underlying asset is that the shareholder not only benefits from the impact of falling interest rates and capitalisation rates on the existing pool of assets owned and managed by the company, but the increased demand for income generating assets also drives fund inflow, adding further growth to the revenue and earnings line.

However, to leverage both sides of this opportunity, the company must have both a strong property acquisition capability as well as the platform to tap increasing investor demand.

One of the companies benefiting is Centuria Capital (ASX:CNI). Over the last few years, the company has been building out its distribution platform and broadening its geographic and property class capability with the acquisitions of Healthley, Augusta, and PrimeWest.

The benefits of those acquisitions in combination with its existing capability in unlisted and listed office and industrial property funds was evidenced in the recent results presentation for the year to 30 June 2021.

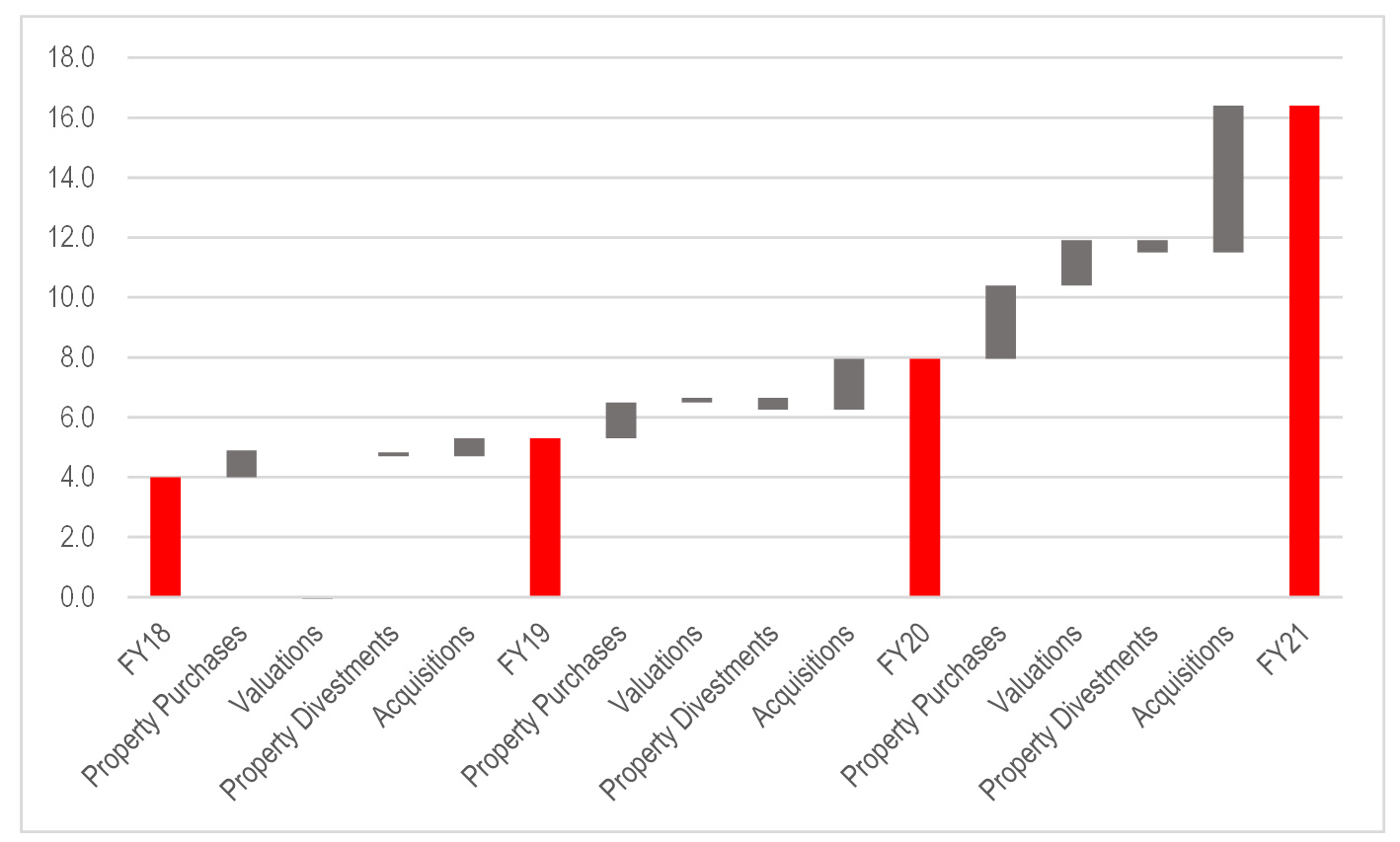

The company has delivered material growth in assets under management over the last few years both on an organic and acquired basis.

Figure 1: CNI – Property Assets Under Management – Drivers of Growth

Source: Company, MIM

Given property management revenue is driven by assets under management (AUM), the material increase in AUM in FY21 sets the company up for a step up in management fees and earnings as the impact is annualised from FY22.

Additionally, management guided to an additional A$2.75 billion of property acquisitions in FY22, with activity to date running ahead of expectations.

Centuria has recently added another string to its bow with the addition of a property development capability. The company stated that its current committed pipeline of A$1.15 billion of projects, most of which will be owned and funded by third party mandates and managed trusts, is expected to deliver fee revenue over the next 2-3 years. It will accelerate Centuria’s growth in assets under management and reduce its reliance on making acquisitions to meet the growing demand for its products. The company also has a future uncommitted development pipeline of A$758 million which would flow through over 5 to 6 years.

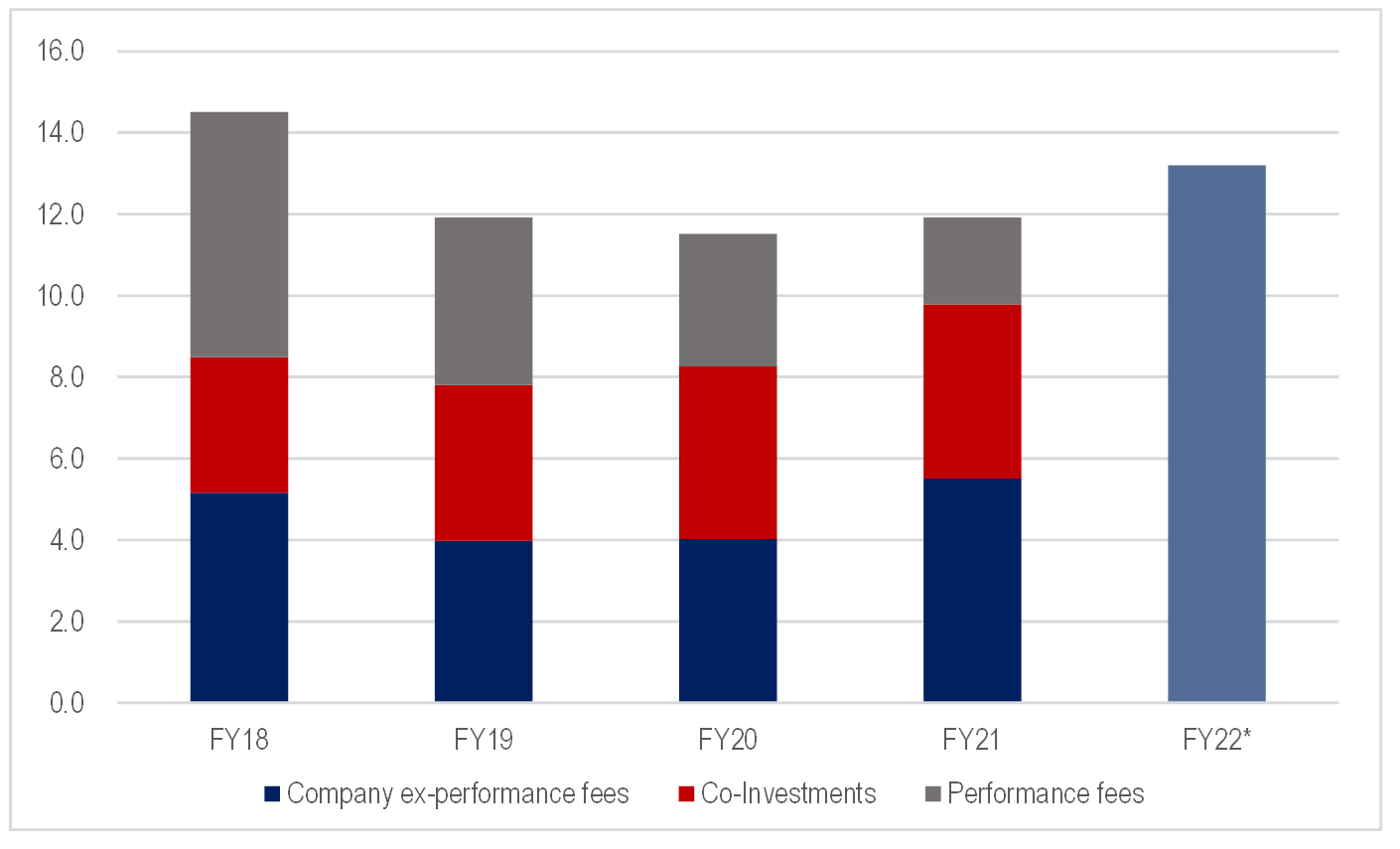

The company’s operating earnings per share has been flat to down over the last few years as equity issuance to fund platform acquisitions has more than offset profit growth. However, the aggregate EPS numbers hide the improving quality of the earnings base with earnings increasingly generated by more secure management fees and income from co-investments rather than volatile performance fees.

Figure 2: CNI – Operating EPS Drivers

* Management Guidance Source: Company, MIM

The above also includes management’s guidance for FY22 operating EPS. With the platform now in place and delivering accelerated growth in assets under management, operating EPS growth is expected to accelerate materially in the coming years.

The Montgomery Funds owns shares in Centuria Capital. This article was prepared 15 September 2021 with the information we have today, and our view may change. It does not constitute formal advice or professional investment advice. If you wish to trade Centuria Capital you should seek financial advice.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY