The limitations of monetary policy and negative interest rates

Following my blog entitled “The Next Economic Disaster” I thought it worthwhile exploring why Central Banks aren’t succeeding in their sworn fight against deflation.

The main reasons are:

1. China’s private sector debt to GDP ratio has rocketed from 150 per cent to around 210 per cent in the past six years. In absolute terms, China’s private sector debt has grown from $8 trillion to $23 trillion and this has created enormous overcapacity in housing, steel and cement etc.

2. With severe overcapacity come problem loans from the Chinese financial sector. Recent examples include housing in the US in 2008 and commercial real estate in Japan in 1991. Some commentators believe Chinese banks’ aggregate problem loans are a staggering US$2-$3 trillion, and this compares with their US$1.5 trillion of capital. (These are similar numbers produced by the US banking sector in 2008/09, however the US economy is 70 per cent larger than the Chinese economy). So we wait for the Chinese banks and shadow banks to come clean on their loan loss provisions or for recapitalization announcements from the Government.

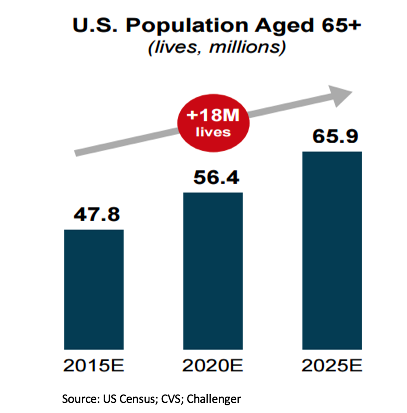

3. Western World demographics means the growth in consumption will be limited as my parents generation are only earning one or two per cent per annum risk-free on their hard earned savings. Grandparents are handing down excess goods to their children and grandchildren and are enjoying more local services (restaurants and cinemas) rather than buying more imported goods.

4. Stress among selected commodity producers will likely increase as many hundred billions of dollars of debt matures over the next four years. With $400 billion of debt set to mature in 2020, investors are particularly nervous about the fact this represents the highest amount of rated debt to mature in a single year in the history of credit markets. Refinancing will be a challenge for may issuers. In an example close to home, today’s Sydney Morning Herald stated “Arrium’s Whyalla steelworks and thousands of South Australian jobs are hanging in the balance after the company’s irate bankers knocked back a US$927 million (A$1.21 billion) lifeline from United States vulture fund GSO Capital. Australia’s big four are part of the 20 plus banking syndicate”.

4. Stress among selected commodity producers will likely increase as many hundred billions of dollars of debt matures over the next four years. With $400 billion of debt set to mature in 2020, investors are particularly nervous about the fact this represents the highest amount of rated debt to mature in a single year in the history of credit markets. Refinancing will be a challenge for may issuers. In an example close to home, today’s Sydney Morning Herald stated “Arrium’s Whyalla steelworks and thousands of South Australian jobs are hanging in the balance after the company’s irate bankers knocked back a US$927 million (A$1.21 billion) lifeline from United States vulture fund GSO Capital. Australia’s big four are part of the 20 plus banking syndicate”.

5. Negative interest rates may cause solvency issues for certain sectors of the economy. Witness the poor share price performance from selected Western European insurers and banks, for example, so far this calendar year including the likes of UniCredit (-41%), Credit Suisse (-38%), Deutsche Bank (-35%), Generali (-25%) and Societe Generale (-24%).

To learn more about our funds, please click here, or contact me, David Buckland, on 02 8046 5000 or at dbuckland@montinvest.com.

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.