Should you ignore the hype?

TPG Telecom Limited (ASX: TPM) has been sold off sharply over the past few days presumably post the Government’s response to the Vertigan Panel’s review of the National Broadband Network & telecommunications industry which you can find here.

The report contains a lot of material, an analysis of which could extend for several pages, so below we attempt a more concise review of some of the changes and their potential implications for TPG as we currently see them.

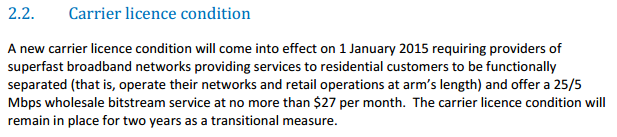

The first is section 2.2: Carrier licence condition; to summarise, this puts price limits on what TPG can charge on a wholesale basis for its FTTB (Fibre to the Basement) network rollout plan. If we consider the expected cost per premise of $500-$600 dollars, it’s an easy calculation to see the potential returns at $27 per month are not too bad when fibre can last in the ground for up to 30 years. But there’s a catch.

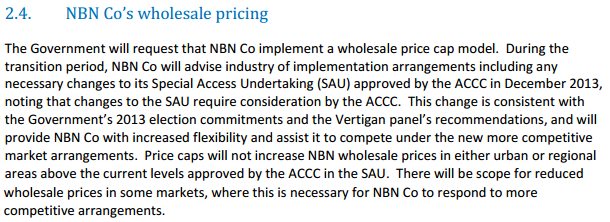

Under section 2.4 NBN Co’s wholesale pricing; essentially this passage identifies that NBN Co will compete against TPG at some stage given both would have networks running into a building and hence will compete against each other for customers. This is complicated because telecommunications lines running beside one another are known to interfere with each other’s connection quality.

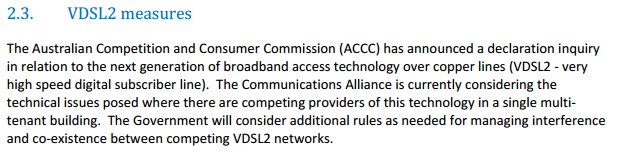

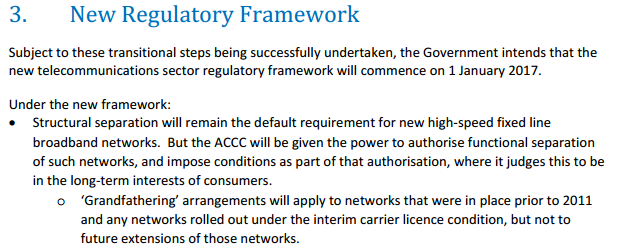

The government seems to be looking at this partly in section 2.3 VDSL2 measures. It’s also interesting to note that Section 3 (New Regulatory Framework) essentially gives TPG until 1 January 2017 in order to complete its rollout (i.e. it closes the loophole that TPG has been using until now). In our opinion, this is a problem for TPG’s FTTB prospects as it’s highly unlikely that this would be an adequate time frame.

TPG currently has to obtain permission from the property owner to access the building (for installation purposes) and Telstra Corporation Limited (ASX: TLS) to access the ducts containing the telecommunications wiring. This often results in long delays in the rollout of their FTTB network and one has trouble seeing how they could possibly reach their target of 500,000 connections by 1 January 2017.

It’s important to note, however, that for every customer TPG cannot connect to its FTTB infrastructure, it can instead resell them a service on the NBN. To this point, TPG already is pricing itself competitively and is adding circa 500-600 NBN customers per week. On this basis, we see only marginal differences between customers signing up with TPG on a FTTB service and those signing up for a resold NBN plan.

To sum up, whilst the changes do appear to impact their ambitious FTTB project, the remainder of their business appears set to push forward like it has done in the past. Competitive advantages in both NBN resale & their corporate opportunities remain intact and despite the hype about FTTB, these opportunities are likely where the real longer-term growth is.

To a degree, it seems that the market may be over-reacting with their share price down heavily since the Governments response was released.

However understanding the businesses prospects and its drivers, given we are not currently shareholders, we are at the same time very welcoming of a quality businesses shares becoming cheaper.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY