Rethinking the core

For decades, Australian and global investors seeking income have depended on a traditional “Core” fixed income allocation for their portfolios, mainly consisting of government-related debt and investment-grade corporate bonds. The result is the conventional 60/40 portfolio – a widely accepted blend of equities and fixed income (bonds).

Structural changes in liquidity, regulation, and market dominance, however, are occurring rapidly and may reduce the effectiveness of these old benchmarks.

The “Fixed Income Replacement” framework, championed by Apollo Global Management, demonstrates how, here in Australia, Aura Credit Holdings’ private credit strategies – specifically the Aura Core Income Fund and the Aura Private Credit Income Fund – can help investors enhance the returns from the fixed income component of their portfolios, while maintaining quality and risk parameters in a fast-changing landscape.

The convergence

Globally, at least, the traditional fixed income landscape is being reshaped by three primary forces:

- Spread Compression: Yields in public credit markets have become increasingly compressed, leaving little room for active “alpha”.

- Benchmark Concentration: Public indices are becoming highly concentrated in specific sectors and issuers, increasing systemic risk for passive investors. By way of example, nearly half (47 per cent) of the Investment Grade (IG) Corporate Bond Index is exposed to just three sectors: Banking, non-cyclical consumer, and technology*. *Data as of December 2024. Note: Data is based on estimates from sample of 8,689 funds. Source: Bloomberg, Apollo Chief Economist

- The Liquidity Paradox: The forces that have made some segments of public credit more liquid have also contributed to narrower spreads, reducing opportunities to generate differentiated yields and making it difficult for investors to achieve durable, high-quality income.

As a result, private credit – once a niche market for distressed debt – has evolved into an estimated US$40 trillion global market, with the majority, according to Apollo Global Management, now being investment-grade quality.

This “convergence” of public and private markets allows and requires investors to seek “excess yield” by providing capital where traditional banks have retreated.

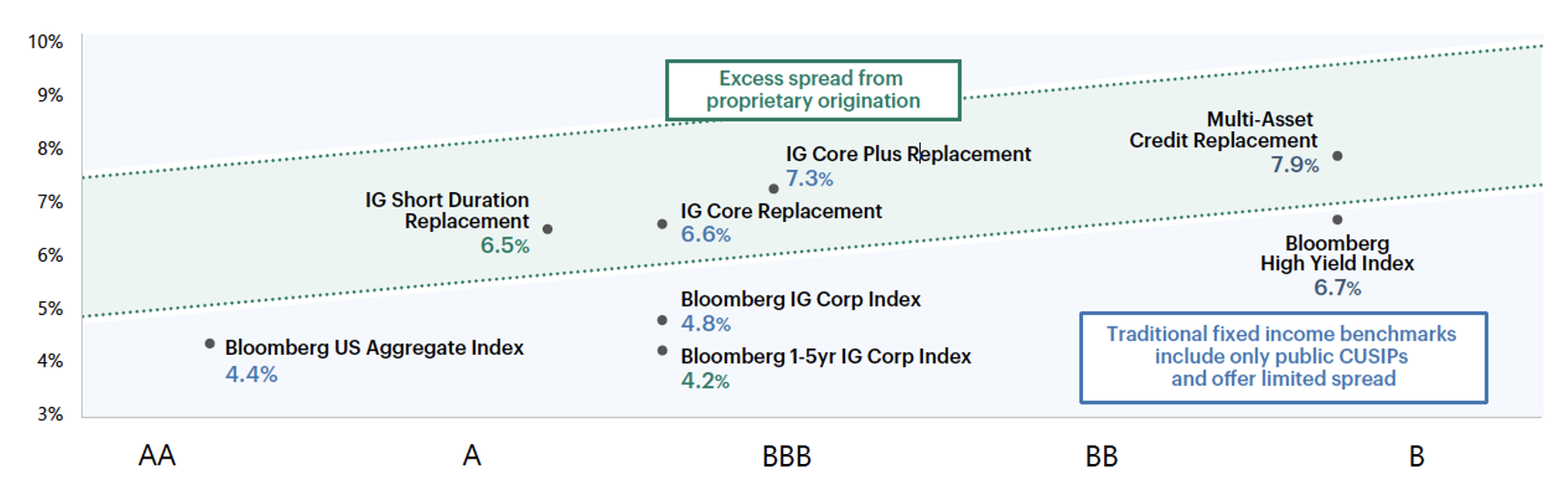

As Figure 1., reveals, the Fixed Income Replacement idea can generate excess spread (higher yields) relative to public markets. The size of the opportunity means investment grade private credit is a scaleable source of yield and diversification.

Perhaps more importantly, as Apollo points out for investors, Figure 1., shows, in a direct quote: “Replacing some public fixed income exposure with private credit has the potential to provide investors with excess spread without excess credit risk. As just one example, private investment-grade credit can provide 150-200+ basis points of excess spread compared to traditional Core Fixed Income and public IG corporate debt without going lower in credit rating.”

Figure 1. Private and Public Yield Differentials (higher yield for a given risk)

Source: Apollo Analysts, Barclays, ICE BofA, Pension & Investments. Data as of July 31, 2025. For illustrative purposes only. Note: Fund ratings are based on the underlying investment ratings using S&P, Kroll, Moody’s, and Apollo Analysts. Spreads presented for private market portfolios are based on hypothetical model portfolios and are not indicative of actual spreads experienced. Actual results may vary substantially.

The Australian context: the banking retreat

The global trend of retreating banks is particularly visible in Australia. As major banks face stricter regulatory capital requirements, they have significantly reduced their lending to Small and Medium Enterprises (SMEs). This “funding gap” presents a compelling opportunity for private investors to provide tailored, professionally-directed asset-backed and secured financing to high-quality businesses.

Aura Credit Holdings has positioned its funds to capture this premium, providing Australian investors with access to a diversified pool of private debt assets that were previously the sole domain of institutional banks.

Implementing the Fixed Income Replacement (FIR) framework

Apollo’s “Fixed Income Replacement” (FIR) framework suggests that investors should categorise private credit based on the traditional assets they are meant to replace. Aura offers two distinct paths for Australian portfolios:

- Core replacement: Aura Core Income Fund

For investors seeking to complement their “Core” corporate fixed income – traditionally the safest, most stable part of a corporate portfolio – the Aura Core Income Fund is designed with capital preservation as the “first order of concern.”

- Strategy: Focuses on senior-secured positions within the capital stack, providing an additional layer of security.

- Performance: Targets a return of 3.5 per cent – 5.5 per cent above the Reserve Bank of Australia (RBA) Cash Rate (currently aiming for ~7.35 per cent – 9.35 per cent p.a. net of fees) and paid as monthly distributions.

- Role in Portfolio: Acts as a “Core/Core-Plus Replacement,” offering higher yields while maintaining low volatility and high-quality asset backing.

- Short duration, higher-yield replacement: Aura Private Credit Income Fund

For those seeking to enhance yield further, the Aura Private Credit Income Fund (formerly the Aura High Yield SME Fund) provides a powerful solution. Like, Aura Core Income Fund, it is also designed with capital preservation as the “first order of concern.”

- Strategy: Invests in a highly diversified portfolio of over 13,900 individual loans to Australian SMEs, typically with a short duration of 3–6 months.

- Performance: Targets a robust return of 9 per cent – 12 per cent p.a., paid as monthly distributions.

- Role in Portfolio: Seeks to deliver higher yields with the downside protection of asset-backed, short-term lending.

Key advantages of Aura’s Private Credit approach

Following the principles of the Fixed Income Replacement framework, Aura’s funds offer several structural advantages:

- Inflation protection: Both funds utilize floating-rate loans. As the Reserve Bank of Australia (RBA) adjusts interest rates, the yield on the underlying loans adjusts accordingly, protecting investors from the price erosion typically seen in fixed-rate bonds during inflationary periods.

- Diversification and scale: By lending to thousands of SMEs across multiple industries, Aura avoids the “concentration risk” that plagues other private and public offerings.

- Structural protections: Aura employs sophisticated risk-management measures, including independent warehouse note trustee structures and “first-loss” capital from lending partners, ensuring investor capital is shielded from initial defaults.

A new blueprint for income

The convergence of public and private credit is not a temporary trend; it is a structural evolution of the financial markets globally. For Australian investors, the path forward involves moving beyond the limitations of traditional bond indices or portfolios and embracing private credit as a fundamental component of the “Fixed Income” allocation.

Whether through the AA rated Aura Core Income Fund or the enhanced yield of the Aura Private Credit Income Fund, Aura could provide the tools to help build a more resilient, higher-yielding, and truly diversified portfolio for the years ahead.

Disclaimer:

You should read the relevant Product Disclosure Statement (PDS) or Information Memorandum (IM) before deciding to acquire any investment products.

Past performance is not a reliable indicator of future performance. Returns are not guaranteed and so the value of an investment may rise or fall.

This information is provided by Montgomery Investment Management Pty Ltd (ACN 139 161 701 | AFSL 354564) (Montgomery) as authorised distributor of the Aura Core Income Fund (ARSN 658 462 652) (Fund). As authorised distributor, Montgomery is entitled to earn distribution fees paid by the investment manager and may be issued equity in the investment manager or entities associated with the investment manager.

The Aura Core Income Fund (ARSN 658 462 652)(Fund) is issued by One Managed Investment Funds Limited (ACN 117 400 987 | AFSL 297042) (OMIFL) as responsible entity for the Fund. Aura Credit Holdings Pty Ltd (ACN 656 261 200) (ACH) is the investment manager of the Fund and operates as a Corporate Authorised Representative (CAR 1297296) of Aura Capital Pty Ltd (ACN 143 700 887 | AFSL 366230).

You should obtain and carefully consider the Product Disclosure Statement (PDS) and Target Market Determination (TMD) for the Aura Core Income Fund before making any decision about whether to acquire or continue to hold an interest in the Fund. Applications for units in the Fund can only be made through the online application form that accompanies the PDS. The PDS, TMD, continuous disclosure notices and relevant application form may be obtained from www.oneinvestment.com.au/auracoreincomefund or from Montgomery.

The Aura Private Credit Income Fund is an unregistered managed investment scheme for wholesale clients only and is issued under an Information Memorandum by Aura Funds Management Pty Ltd (ABN 96 607 158 814, Authorised Representative No. 1233893 of Aura Capital Pty Ltd AFSL No. 366 230, ABN 48 143 700 887).

Any financial product advice given is of a general nature only. The information has been provided without taking into account the investment objectives, financial situation or needs of any particular investor. Therefore, before acting on the information contained in this report you should seek professional advice and consider whether the information is appropriate in light of your objectives, financial situation and needs.

Montgomery, ACH and OMIFL do not guarantee the performance of the Fund, the repayment of any capital or any rate of return. Investing in any financial product is subject to investment risk including possible loss. Past performance is not a reliable indicator of future performance. Information in this report may be based on information provided by third parties that may not have been verified.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.