Rainbows, Unicorns, V-Shaped recoveries and other fantasies

There are a bunch of reasons to expect this recovery to be longer and more painful than the market’s V-shaped expectations. Of course, within such an environment there will be businesses that do well, and we reckon we own a whole bunch of them in The Montgomery Fund and the Montgomery Small Companies Fund.

Thankfully we also have a lenient mandate when it comes to holding cash, ensuring we also have the ability to preserve capital when prudent.

A slow and halting recovery is something we have been contemplating as we weigh up the arguments put forward by those who believe the recovery will be easy and quick, and those who reside in the slow and halting camp. First let’s look at employment, keeping in mind the retail sector is the second largest employer and the construction industry is the third largest.

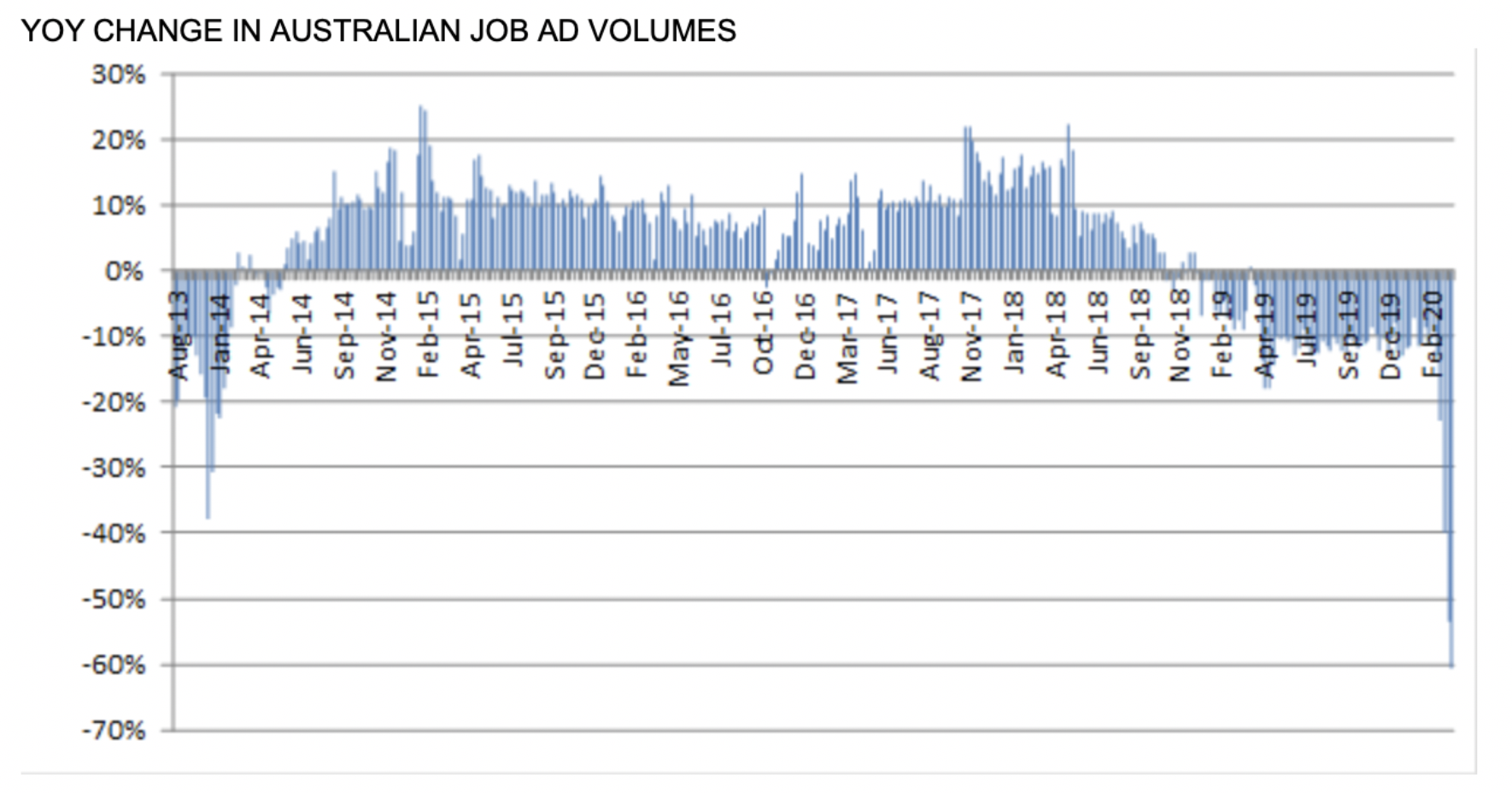

As Figure 1 shows there has been a material disruption to the jobs landscape.

Figure 1. Seek Year on Year Job Ad Volumes

Source: Seek

Fewer ads means there are fewer business looking to hire. While April unemployment numbers revealed a jump in unemployment from 5.2 per cent to 6.2 per cent, the fact is that all employees who received the government’s JobKeeper wage subsidy were counted as employed even if they didn’t work any hours! The participation rate fell to its lowest level in sixteen years, from 66 per cent to 63.5 per cent. If the participation rate had remained unchanged, the unemployment rate would be over 10 per cent.

Peter Costello, our longest serving treasurer, remarked; “… it’s going to take some time to get unemployment back to 5 per cent…If we peak at 10 per cent or 11 per cent, I think we’ll get back to seven pretty quickly, but I think it’s going to be a long hard grind to get back to 5 per cent unemployment.”

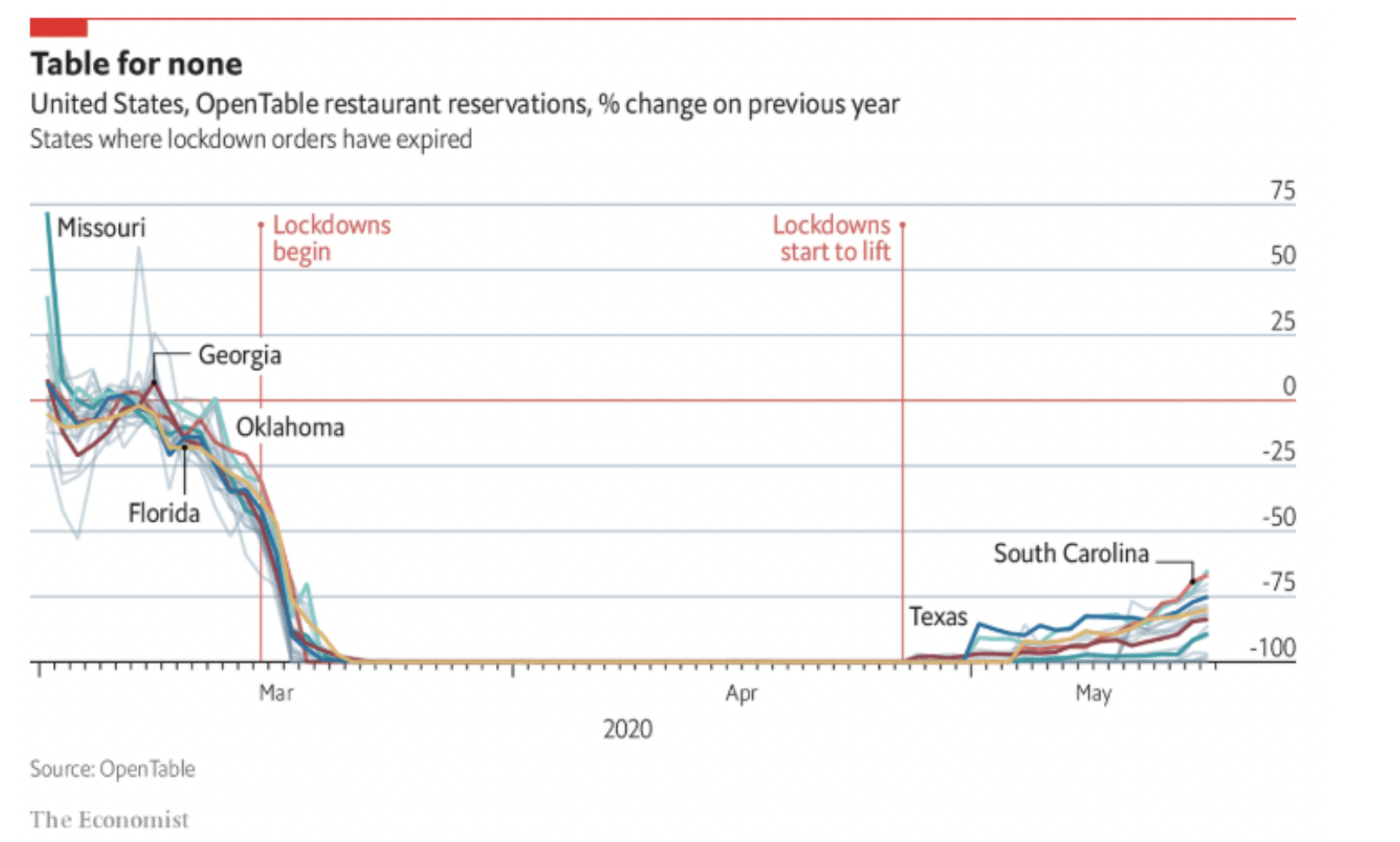

And take a look at what is happening to restaurant businesses in some US states where lockdowns have been unwound completely.

Figure 2. OpenTable restaurant reservations

A close look at the chart in Figure 2. reveals restaurant bookings are taking much longer to rebuild than the speed at which they stopped. Even in states where COVID-19 did relatively little harm (thus far), bookings remain depressed. In Georgia, for example, where restaurants have been open for three weeks, bookings remain 84 per cent lower than their peak. Florida bookings are 80 per cent low, Texas down 75 per cent, and South Carolina, where two weeks have elapsed since stay-at-home orders were lifted, is still 67 per cent weaker.

According to Steve Hafner, the chief executive of OpenTable, as many as a quarter of restaurants in the US will never open their doors again. Profit margins on these businesses are wafer thin thanks to labour and rent so many of those who have lost jobs may find their old job no longer exists.

The read-through for Australian jobs should not be underestimated, and the impact on those job ads (Figure 1.) could mean they remain depressed for some time.

On top of the challenges for hospitality, retail is also doing it tough, and remember retail is the second largest employer in Australia. A conga-line of consumer facing businesses have collapsed this year or are closing a significant number of stores including McWilliam’s Wines, Flight Centre, G-Star, EB Games, Bardot, Curious Planet, Jeanswest, Bose, Kaufland, Colette, Ishka and Kikki K. And this is on top of those that have collapsed in 2019 and 2018 including Harris Scarfe, Napoleon Perdis, Dimmeys, Ed Harry, TopShop, Gap, Esprit, ToysRUs, Roger David and Shoes of Prey.

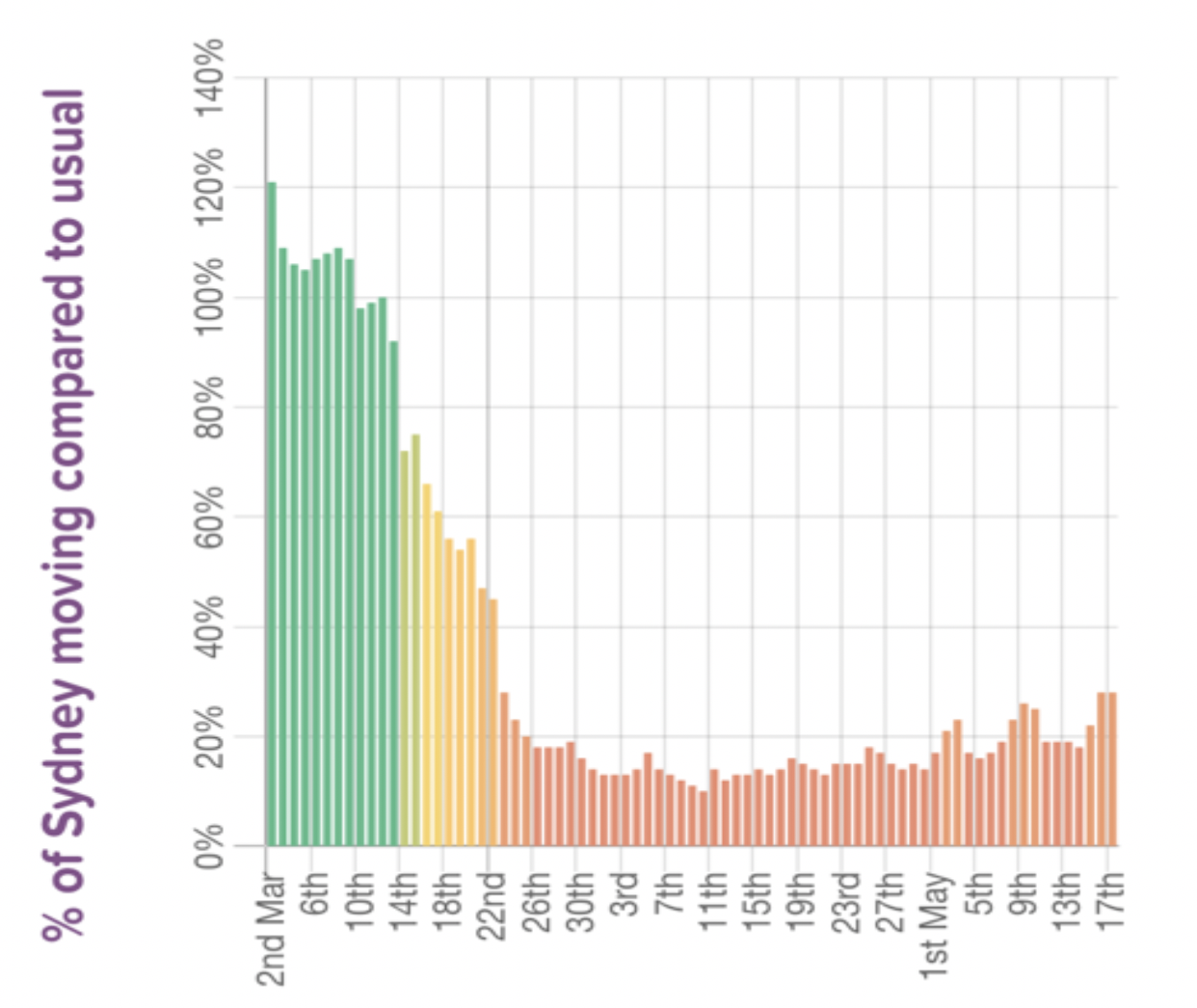

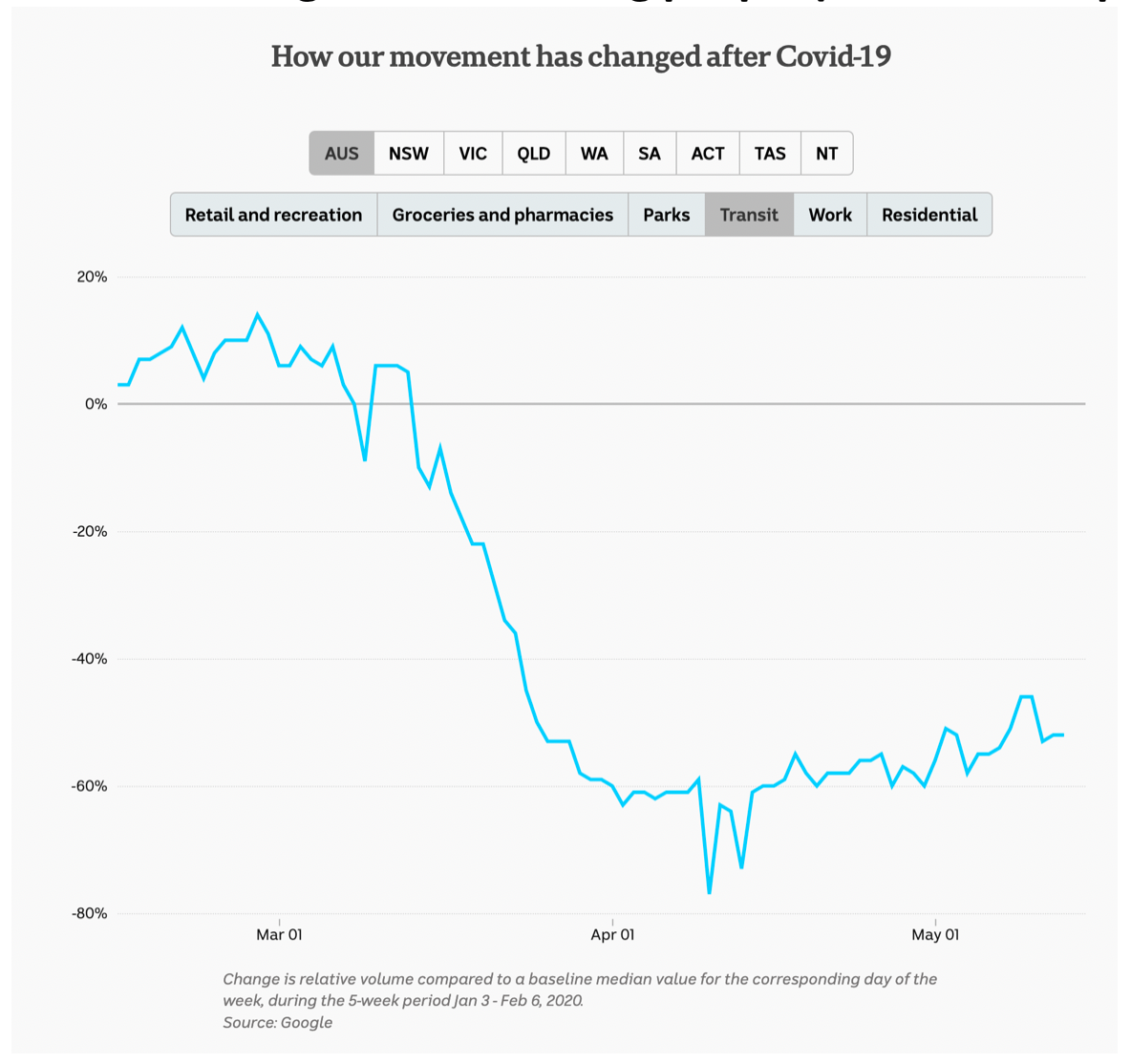

Data from city mapper (Figure 3.) and Google (Figure 4.) shows that the number of people in transit, at work, in shops and at parks has jumped spectacularly from the low point in Australia on April 10 when those movements were down 80 per cent from a normal, pre-COVID-19 day. Today the level of those activities is down between 30 and 50 per cent. Importantly, they have not reverted to normal, and given a higher level of unemployment, may not do so for some time.

Figure 3. Percentage of people moving in Sydney compared to a pre COVID-19 ‘Normal’

Figure 4. Transiting people (with Android phones) Australia wide

The construction industry is the third largest employment sector in Australia, and a third of its employees are in residential construction. Our channel checks suggest residential builders are experiencing cancellations of up to a third of new home building contracts.

Adding up the situation in retail, hospitality and construction, it looks likely there will be fewer jobs for people to come back to when the JobKeeper payments cease. Jobkeeper payments have been helping support household incomes but the stresses on those incomes from this recession are already being felt. According to bank data, ten per cent of the banks’ mortgage books are already in hardship and that’s on top of the two per cent officially in arrears.

This is occurring while half of the nation’s workforce are on income support through an increased JobSeeker payment or the JobKeeper wage subsidy. But both of these programs terminate after six months, unless the government extends them. Additionally, the eviction bans protecting tenants and the big four’s offer to suspend mortgage repayments for landlords expire at the end of the third quarter of calendar 2020.

Any short-term jump in retail sales as pent up demand is sated amid the plethora of expected seasonal sales will probably as households are forced to manage significant declines in household cash income and still record levels of household debt.

Finally, let’s think about recessions, and particularly their length. If a recovery is defined as a return to pre-crisis incomes, famed economists Carmen Reinhart and Kenneth Rogoff note that it took four year on average to ‘recover’ across the post war crises. Following the Great Depression, it took ten years. Meanwhile the average length of all global recessions has been 18 months and my read of the 39 US recessions since the 1836 recession, and the beginning of the free banking era, is that they averaged one year and eight months.

It’s a far cry from the six months that the market’s v-shaped recovery is clearly anticipating.

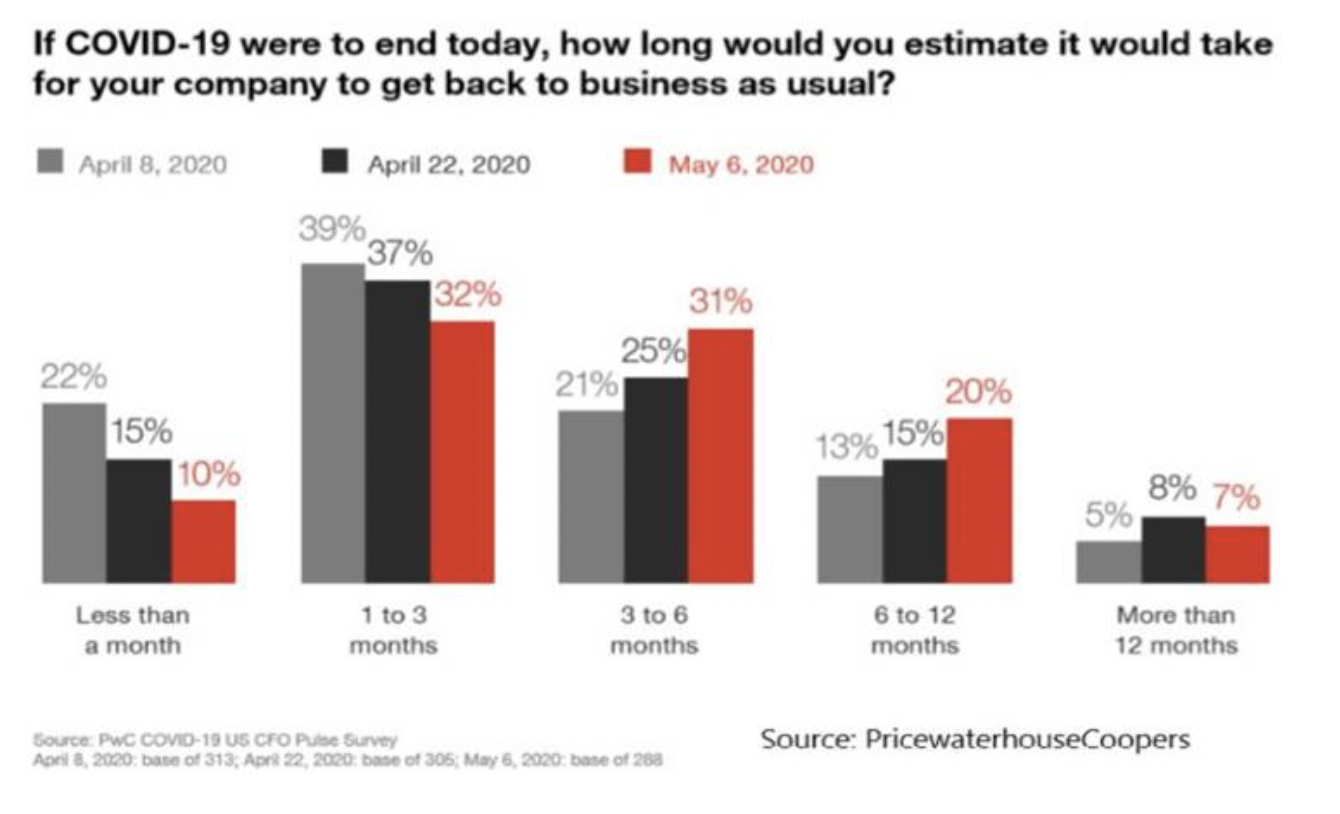

It’s even a far cry from the length of time current business owners are saying they will take to recover (Figure 5.).

Figure 5. Australian business owners’ expectations (PWC Survey)

There are some businesses that will do well through this crisis and recession, taking share and attracting a new legion of loyal customers, but there are many more that will suffer. In aggregate it seems the market might be unduly optimistic about the prospects for many businesses and a V-Shaped recovery might be relegated to the same fantasy as rainbow-coloured unicorns.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

Roger,

The economy makes no sense to me at the moment.

I have been talking to friends who are in a range of industries (Construction, real estate, specialist retail) and all but one have used the phrase “never been busier”.

The bulk of these people are on the large housing estate side of construction but the media says new house sales are down.

My friend in retail is putting on more staff to cope with the workload. But media reports have them waiting outside centre link.

Even the well dressed people in real estate indicate that the lease on the new Audi is not a problem as genuine buyers are still active.

I am not questioning the data but I am wondering if the pandemic will be the real test of the survival of the fittest.

But my question is what are your thoughts on the economic impact if the government puts the brakes on the handouts and reverts to infrastructure expenditure

Hey Andre, please put me in touch with your contacts. Would love to do the due diligence on this. Master Builders Australia, represents $220bn building and construction industry and said today that 73% of its members have reported an average drop in forward work of 40%. Perhaps busy now but forward orders declining?

I wonder if the day will come if the incentive is as much as the asset house you are buying?

My suspicion is this increase in activity – in specific sectors – is a last ditched effort to clear everything off the books.

If I am a builder sitting on a nearly completed housing estate (which there are many of) I am going to put everything I’ve got into getting the stoves and carpets in and sell them at bargain-basement prices. I am trying to beat all the other builders to the sale because I realise I might be left with property that can’t be sold. I will be happy to make small losses before they become big ones. I am not however going to be thinking about buying up new land and building on it. Plenty of work for those in this industry for about 2 more months.

Your view may change John if Josh Frydenberg now decides it is wise to give anyone buying and building a new home $50k towards their plan.