Furniture turning down? Ask Nick Scali

With new house sales in December slumping to the lowest levels in almost two decades, retail sales of household goods declining 2.8 per cent in the December quarter, and December foot traffic down eight per cent year on year, the outlook for furniture retailers doesn’t look promising.

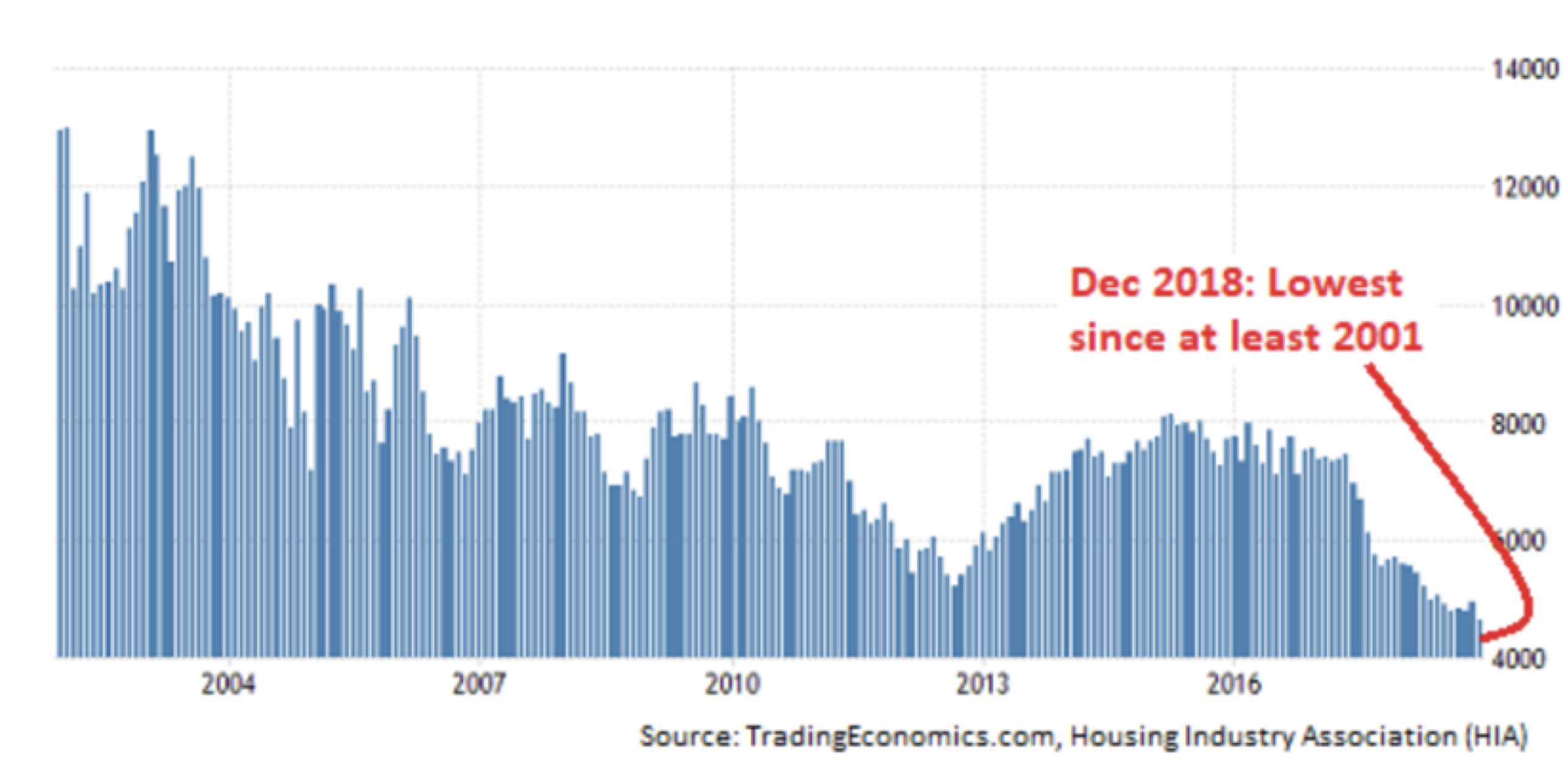

Figure 1. shows a material decline in the sale of new houses suggesting a slump in furniture and appliance sales is on the way.

Figure 1. Monthly sales New Houses Australia

Nick Scali (ASX:NCK) however delivered a first half result that on first inspection appears to suggest the company is bucking the trend.

Nick Scali’s first half 2019 profit after tax was reported up eight per cent to $25.1 million on revenue that was 10 per cent higher. Like-for-like sales revenue was unchanged and very strong cash conversion of circa 80 per cent means there’s plenty to hand out as dividends. But digging a little deeper we find the speed of growth is slowing, which suggests Nick Scali won’t be able to escape the gravitational forces of ‘consumer deleveraging’.

Customer deposits provides a useful insight into future sales and while the $20 million reported is up 1.4 per cent on the previous corresponding period, the company has expanded the number of stores it operates. On same store basis the customer deposits have fallen by about 15 per cent.

Importantly, while the like-for-like sales number was flat for the first six months of the financial year, that number was said to be up two per cent in the first quarter, which means the second quarter saw like-for-like sales decline by about the same amount or a little more.

The company’s numbers have also benefited from a one-fifth reduction in lead times – an improvement quantum that may be difficult to repeat.

The company has said at its briefings that it will maintain prices, rather than volumes, as the market cools, to ensure its brand is protected “out the other side”, implying the company is expecting to enter a rougher patch. Back in 2005 and 2008 the company reported like-for-like sales declines of as much as seven or eight per cent and the share price fell almost 40 per cent in 2005 and 83 per cent in 2008 (GFC influenced).

Nick Scali’s share price peaked in April 2017 at $7.48 and has since declined 25 per cent to around $5.59, putting it on a PE of between 10 and 11 times forward earnings and about five times equity per share. This seems slightly expensive given the downside risk, given the sustainable ROE is probably somewhere south of 40 per cent and given other retailers who are further into their cyclical downturn are trading on PEs of less than ten times.

Assuming a sustainable ROE of 40 per cent (which of course may be optimistic) and a payout ratio of 80 per cent, Nick Scali shares estimated intrinsic value may sit between $5 and $6. A big discount to intrinsic value – a safety margin, however is warranted given the deteriorating outlook, the depths of which is impossible to estimate.

We’ll be watching this sector closely because a couch requires at least two people to move it, making the logistics side for online competitors difficult and thus perhaps protecting Nick Scali from the ecommerce threat.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.