Farewell Fiscal 2015, Hello Fiscal 2016

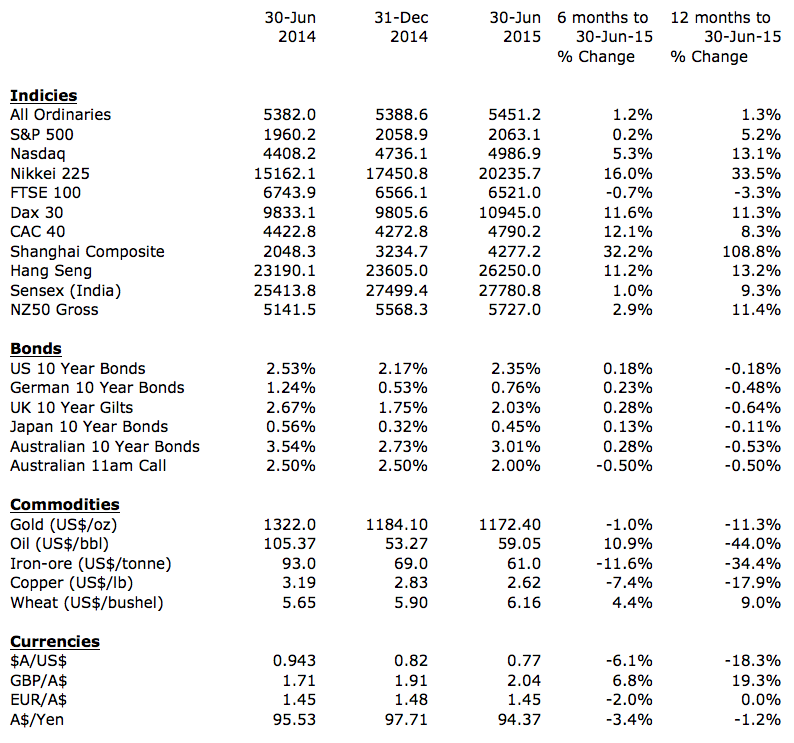

As Fiscal 2015 draws to a close and Greece defaults on its debt repayments, let’s take a look at the year that was. The Australian market, excluding reinvestment of dividends, has continued to trade sideways, up 1.3 per cent from 5,382 to 5,451.

Record low cash rates, which were cut to 2.25 per cent in February and again to 2.0 per cent in May, are supportive of the market, however a number of companies have downgraded their earnings expectations.

With the exception of the FTSE (The Financial Times Stock Exchange) 100, which declined 3.3 per cent, most international markets delivered close to double-digit returns for the year, with the Shanghai Composite Index leading the way, up 108.8 per cent, while the Nikkei 225 increased 33.5 per cent.

After troughing at below 1.65 per cent in early 2015, the US 10-year Government Bond Yield has increased to 2.35 per cent. This 0.7 per cent reversal of the longer-term downtrend has seen the yield on many Governments’ ten year bonds follow suit in recent months.

Hard commodities had a rough year with oil, iron-ore, copper and gold all performing poorly. Oil at least reversed its downtrend in the June 2015 half-year to finish at US$59.05/bbl. Soft commodities are looking more promising and wheat improved 9 per cent to US$6.16/bushel.

The Australian Dollar declined around 18 per cent against both the US Dollar and the Sterling, but was steady against the Euro and the Yen.

My guess is many economies with large external debt to GDP ratios will likely hit the headlines over Fiscal 2016. I have previously pointed out the fact that there are several countries, mostly based in Eastern Europe – while not in as bad shape as Greece – seem to have external indebtedness issues nevertheless.

While the US Federal Reserve has indicated a tightening bias later in the December 2015 half-year (from effectively nil), European Quantitative Easing will be around until the latter part of 2016, and just maybe it will be extended.

FAREWELL FISCAL 2015, HELLO FISCAL 2016

To learn more about our funds, please click here, or contact me, David Buckland, on 02 8046 5000 or at dbuckland@montinvest.com.

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.