Caltex under the pump

The 20 June announcement by Caltex clearly caught the market by surprise, let’s look at the evolving landscape in Australian petrol retailing, the competitive dynamics and how this has impacted Caltex’s profit and share price.

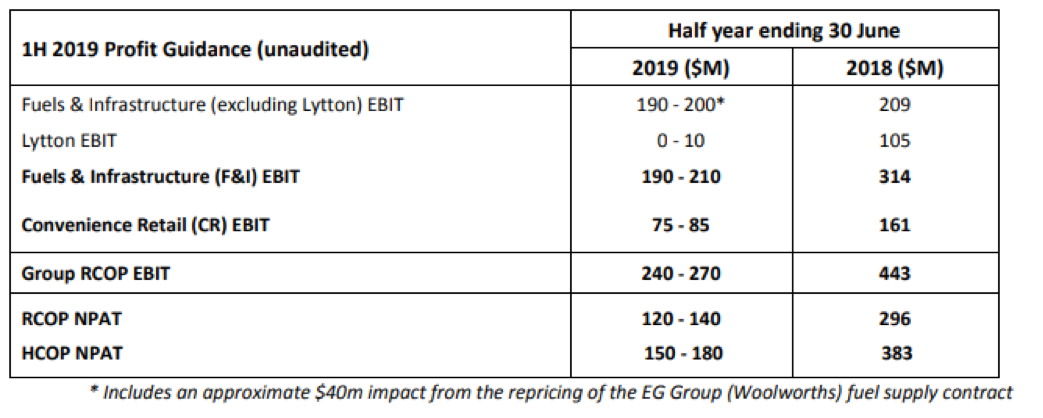

Following on from David’s post on Caltex, the company issued profit guidance for the June 30 half-year. Group EBIT was guided to be between $240-270m for the 6 months, which was between $160-200m below the previous year. It was also $140m below the analyst consensus forecast prior to the announcement.

The announcement clearly caught the market by surprise, as the share price fell by 13 per cent on the day (although it has recovered by about 7 per cent since). The development is interesting due to a couple of reasons:

The fall in Convenience Retail (CR) EBIT signals a structural change in Retail Fuel margins

While the fall in Lytton EBIT is not surprising (Caltex provides an update on refining margins on a quarterly basis – has been monthly historically), the significant drop in CR EBIT suggests retail fuel margins are more volatile than previously believed.

I had previously written about the higher pricing Coles Express had adopted in their arrangement with Viva Energy. However, back in February, the Coles – Viva alliance struck a revised agreement whereby Viva would take on responsibility for retail fuel pricing and marketing (the board price was previously set by Coles). Given the Coles fuel network had been ceding significant market share over the past 2 years due to higher than average pricing (and increasingly savvier and price sensitive motorists), the change in arrangements flagged a renewed push at stemming, and then increasing VEA’s volumes, most likely through lower prices.

There is also signs that the independent sector (e.g. Metro, Westside and Budget) has become a strong competitor.

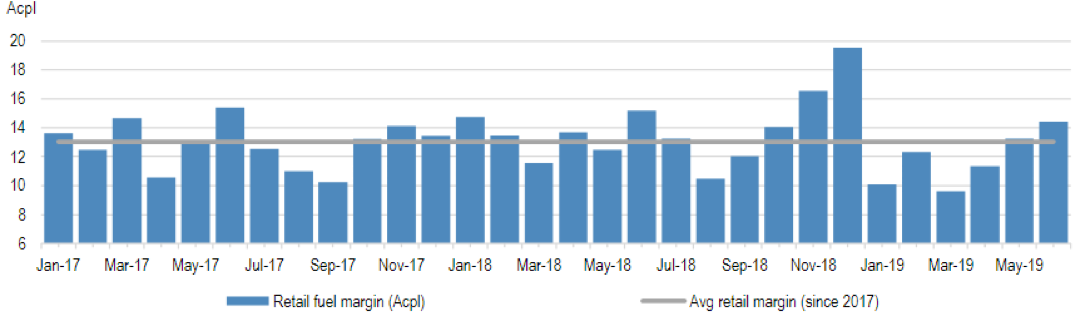

Difference between average Retail less average Wholesale price for fuel

Source: JP Morgan, Australian Institute of Petroleum

This chart demonstrates the change in retail fuel margin over the past 2.5 years. As the chart shows, three of the first six months of 2019 has seen a retail margin significantly less than the average (~2-4c / L), with Jan and March especially impacted.

Caltex issued profit guidance for the June 30 half-year which was between $160-200m below the previous year. Is the downgrade reflecting cyclical or structural factors? Share on XSlowing Australian economy is impacting

Caltex has cited a challenging market, with a slowing Australian economy, lower FX and higher crude prices combining to impact the profit outcome – with industry sales volumes down 2 per cent on the previous half. Despite being a defensive company, the consumer is clearly not immune to slower Australian consumption, especially with motorist’s tendency to have a relatively fixed budget at the “servo.”

Viva announces stabilised volumes

On the June 24, Viva Energy provided its own profit guidance, which was largely in-line with their updated guidance provided in April 2019. The company also cited challenging macro conditions in retail – although this was disclosed earlier in April. In the announcement, Viva announced the company had successfully stabilised volumes in the Alliance (vs previous double-digit declines), although there had yet to be a material increase in sales volumes.

The developments in the Australian retail fuel market highlights the need to monitor the competitor response as keenly as the company’s own initiatives. Observers of the revised arrangement between Viva and Coles – as well as the change in pricing strategy at Coles Express – would be alert to a potential change in competitive dynamics, which has clearly impacted the Caltex profit and share price.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY