Beware the pitfalls of speculating on this market

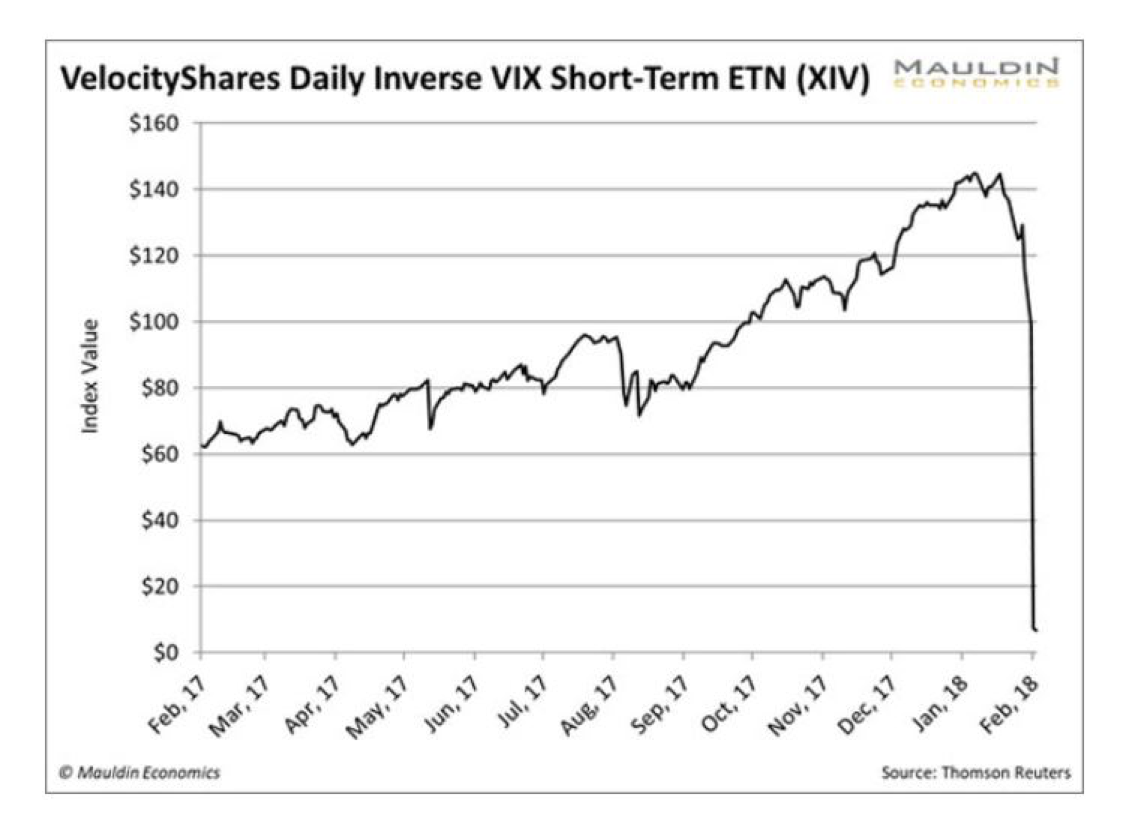

Most of us know of the volatility index, otherwise known as the VIX. But the inverse index – the XIV – was little known until a recent story surfaced about a trader who lost $4 million when the XIV lost 96 per cent of its value in one day. It was a sobering reminder that this bull market can’t roll on forever.

As many of you know, we write regularly for my friends Chris Cuffe and Graham Hand, in their Cuffelinks newsletter. We can therefore highly recommend it here https://cuffelinks.com.au.

The latest issue delivers a useful warning about speculating on, or investing in, a continuation of the higher stock market and ultra-low volatility theme. I repeat the warning below because I couldn’t have said it better than the trader who bet the farm and lost the lot.

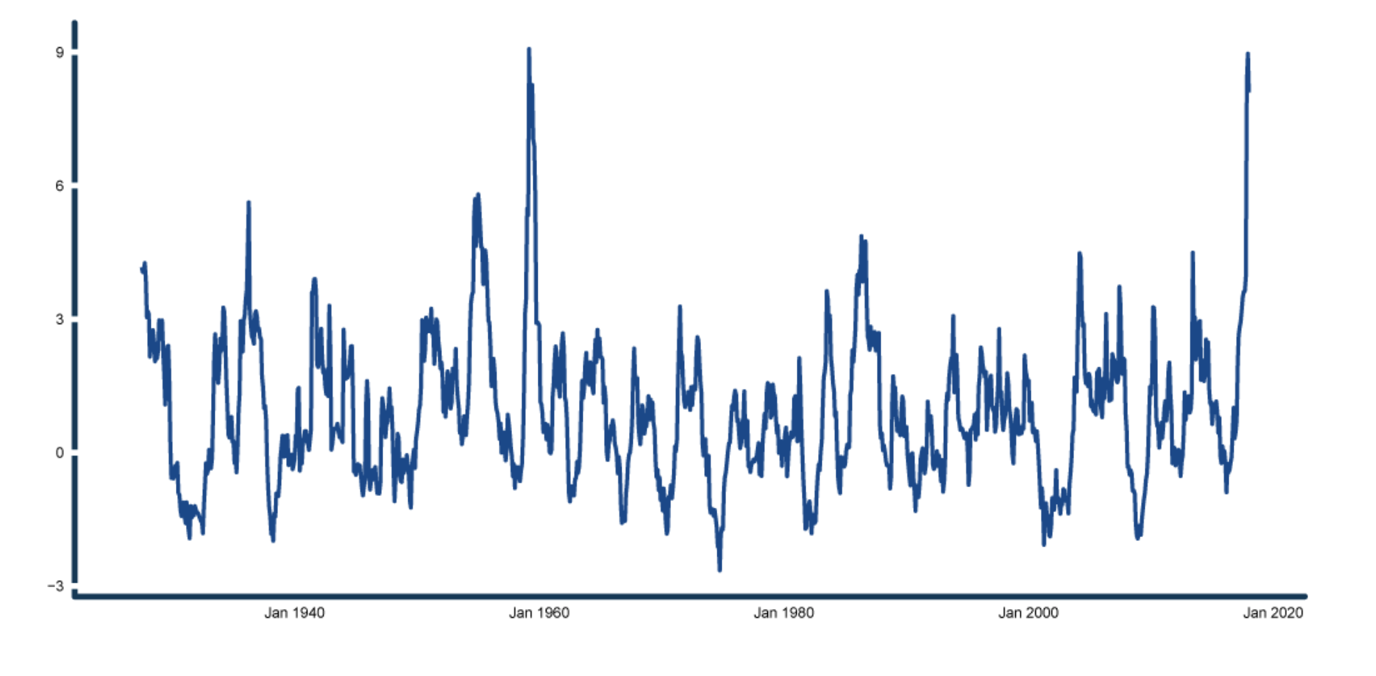

As the following chart of the rolling 1-year annualised Sharpe Ratio for the S&P500 reveals, smooth and high returns simply don’t last, and certainly not at levels that produce the Sharpe ratio recently recorded to December 31, 2017.

Here’s an excerpt from the latest edition of Cuffelinks’s Editors Letter.

There’s a scramble now to explain XIV. Bring on Lewis’s next book. One day after the CBOE Volatility Index (VIX) had its largest-ever one day rise of 116 per cent, Credit Suisse announced it would close its inverse VIX note. This VelocityShares Daily Inverse VIX Short Term ETN (NASDAQ code XIV) lost 96 per cent of its value on one day. It’s arcane to most Australian investors, but this was a $2.5 billion listed note that many local traders enjoyed as it returned 150 per cent per annum for the previous two years.

What happened? In brief, until the start of 2018, equity markets had enjoyed years of falling volatility. Traders used products based on the value of the VIX (the VIX is an index and cannot be directly bought or sold) to sell at say 20, and buy back at say 12 as volatility fell. The inverse note, XIV, traded on the market just like a share, and as the VIX fell, XIV increased in price. Where there’s demand, Wall Street creates a product.

But many traders had forgotten about risk. As volatility returned to the market, VIX rose dramatically, and the inverse note, the leveraged XIV, collapsed.

This ‘shorting volatility’ strategy paid for many a Porsche out of trader bonuses. Discussion website Reddit has a ‘Trade XIV’ group with 1,800 members, which carried posts like: “How I made $356,000 on XIV in two years”. Now it includes this post:

“I’ve lost $4 million, 3 years of work, and other people’s money. I started with 50k from my time in the army and a small inheritance, grew it to 4 mill in 3 years of which 1.5 mill was capital I raised from investors who believed in me. The amount of money I was making was ludicrous, could take out my folks and even extended family to nice dinners and stuff. Was planning to get a nice apartment and car or take my parents on a holiday, but now it’s all gone.”

Many of the investors were friends and family. I have not attached the relevant link to Reddit because much of the language is crude.

I’ll leave it to Michael Lewis to write the XIV book and explain backwardation, gamma and contango, given he will have about 300 pages. Then go watch the movie.

It’s not investing. Volatility trading and the need to cover leveraged risk on XIV and other products probably accelerated the overall market decline. This activity infiltrates mainstream stocks and induces investors to panic in response to headlines and fear. Forces such as these and high frequency trading (where computers automatically issue orders and now comprise about 60 per cent of US equity trading) can have a pervasive impact on everyone’s portfolio. The consequences appear to have been contained this time, and despite the screaming headlines, the US share market is ahead in 2018 to date.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.