Empty promises may pop the AI bubble

I know everyone is focused on Iran and oil at the moment, but when the conflict eventually ends, investors will cheer…and return to the themes that previously dominated markets.

And that theme is artificial intelligence (AI).

At Montgomery, we have always preached that, in the long run, share prices follow a simple trajectory: the present value of future cash flows or the ‘intrinsic value’ of a stock. We have long advocated investors look for “great” businesses with high returns on incremental invested capital and durable competitive advantages.

From time to time, however, the market enters a period of “narrative-driven” exuberance where the arithmetic is ignored in favour of a grand story. A theme.

Recently, and prior to the conflict between the U.S. and Iran, that story was being authored by Sam Altman from OpenAI. And while his prose is beautiful – promising the end of poverty and the curing of all diseases – I am beginning to worry the reality looks far less promising.

Altman has captured headlines with his claims that AI will be able to solve almost all human maladies once a certain level of machine-learning intelligence is reached.

He’s been variously quoted stating AI will solve the 1) housing crisis, 2) cancer, 3) poverty, 4) climate change, 5) mental health, 6) democracy, 7) universal basic income, 8) a bunch of diseases, 9) heart disease, as well as 9) help you accomplish your goals and be your best, 10) provide very high quality healthcare, 11) make important new scientific discoveries, 12) bring the marginal cost of energy rapidly towards zero, and 13) create a more equal world, with its inhabitants enjoying, 14) universal extreme wealth.

Phew. I thought the world was toast. Thank you, AI.

Poor quality revenue

OpenAI’s annual recurring revenue (ARR) has reportedly reached US$20 billion as of late 2025/early 2026, according to statements by CEO Sam Altman and CFO Sarah Friar.

But on the other side of the ledger, Altman has signalled an astonishing US$1.4 trillion in infrastructure spend over the next eight years. If you’re playing along at home, current annual revenue represents less than 1.5 per cent of the promised expenditure.

Even more concerning for any intelligent investor is the nature of this spending. As we’ve reported previously, we’re seeing a circular valuation loop. Microsoft and Nvidia invest billions into OpenAI. OpenAI turns around and spends those same billions on Microsoft’s cloud and Nvidia’s chips.

This creates a phantasmal picture of revenue growth. If Nvidia is essentially funding its own future sales through venture stakes, the quality of those earnings is significantly diminished, if not poor. As a value investor, you have to ask: if the investment stops, does the revenue growth vanish?

Just trust me. Heads I win, tails you lose.

In any research of great companies, management integrity is paramount, and track records are hugely insightful. Mr Altman’s history, however, suggests a pattern of what we might call ubiquity over utility.

Take Loopt, Altman’s first venture. Loopt was a big deal for Altman, as it was his first company, which sold an app for locating friends. Altman reportedly insisted the user base was massive. According to reports, Loopt always refused to say how many users it had, with Altman reportedly insisting there were “way more users than any other similar service.” Reuters reported in 2012, “Loopt founder Sam Altman says the 500 DAU number is off by 100 times, and says he’ll be posting data shortly to prove it,” adding, “When reached for comment, Loopt CEO Sam Altman said the 500 DAU figure is ‘off by orders of magnitude.” Yet, when the business was sold to Green Dot (and promptly shuttered), it was revealed Loopt had only 500 users.

Elsewhere, it is reported that in 2015, Altman agreed with Reddit (see below) to allow OpenAI to scrape everything posted on the forum to feed into OpenAI’s tech. In the year prior, Sam Altman made a public pledge [1] to the Reddit community, promising he and his fellow investors would return 10 per cent of the platform’s value to users – a commitment that remains unfulfilled and, some argue, is ‘conveniently’ obscured by complex regulatory hurdles.

Nevertheless, this perhaps forgotten gesture serves as a sobering reminder of the widening chasm between grand visions, rhetoric, and the reality of OpenAI’s ecosystem.

Conflicts?

Of course, while investors in the listed tech space should be wary when a CEO’s primary product is a “future promise”, they should also be on the lookout for any perceived or potential conflicts of Interest.

As the late Charles Munger once wryly observed,

“Show me the incentive, and I’ll show you the behaviour.”

It’s been noted Altman isn’t just the CEO of the world’s leading AI firm; he is also a major investor in energy companies, including nuclear energy hopefuls Helion and Oklo [2] (be sure to read the Oklo footnote below, which describes recent significant selling of shares by the CEO and COO), as well as the “proof-of-personhood” platform (Worldcoin) that it’s reported OpenAI will use as a necessary layer of verification to combat AI-driven fraud, in an era of human-like AI content.

OpenAI also needs enormous quantities of data because large language models (LLMs) cannot be built without sampling language and content. One source of that data is Reddit, which Altman owns a material share of and was on its board until 2022.

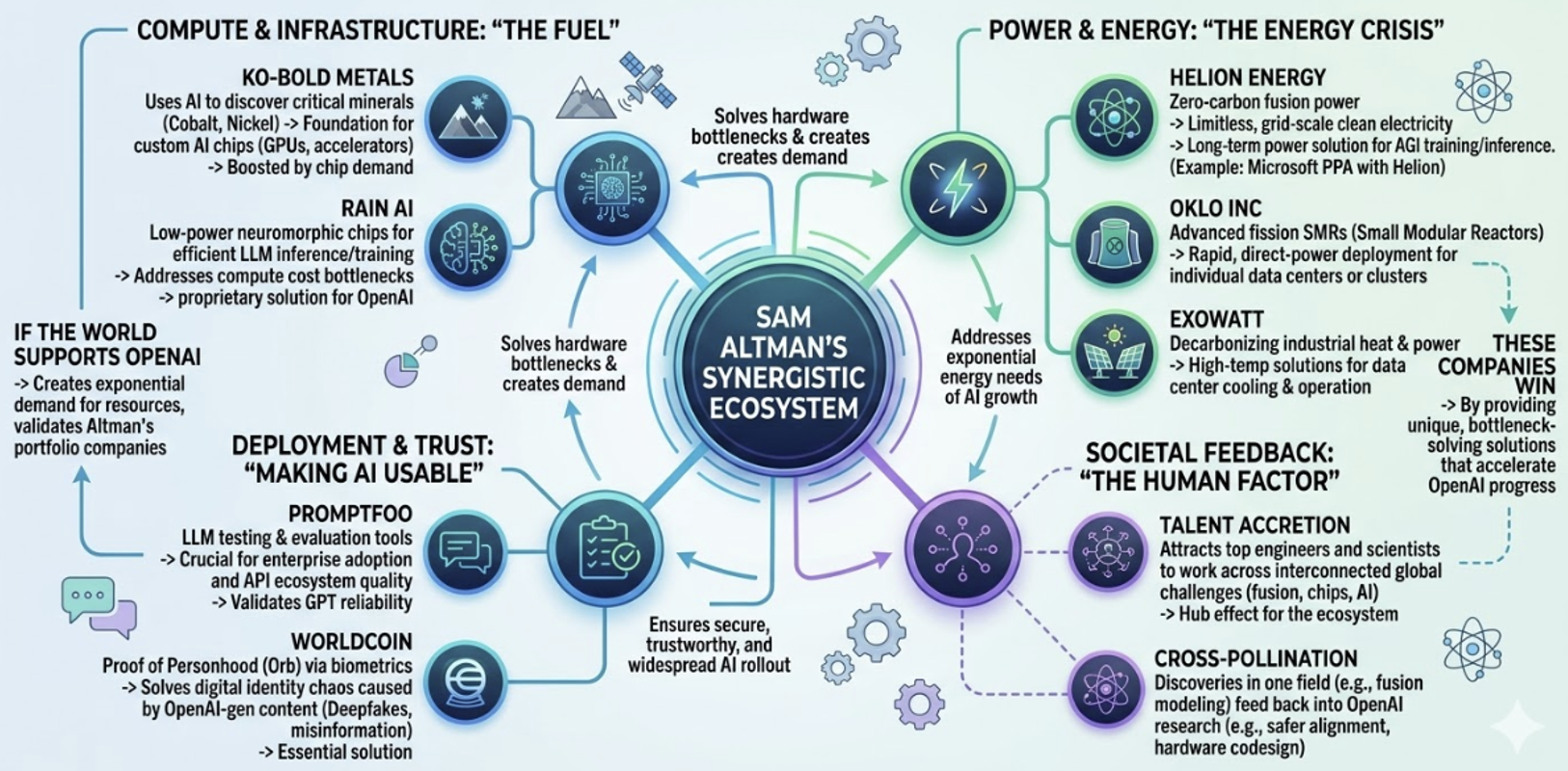

Figure 1. The Altman/Open AI feedback loop

Source: NanoBanana , Prompt: Montgomery

Look beyond the world-curing public declarations to the personal investment portfolio, and you might argue a disquieting pattern emerges. One has to ask whether the world is backing a speculative technology whose ‘messiah’ has strategically positioned his capital across the very pillars necessary for OpenAI’s continued existence.

Reportedly invested in AI networking equipment, thermal battery technology (Exowatt), and the intensive mining of the rare earth metals (KoBold Metals [3]) required to sustain the massive server farms that power AI, Altman’s might be a closed loop of influence where the line between corporate strategy, social good and personal wealth is more than merely blurred.

Altman is also reportedly invested in multiple companies offering protection against AI bad actors (Promptfoo, MirrorTab), the previously mentioned identity verification to prevent deepfakes (Worldcoin), and insurance for losses from AI scams and hacking.

Altman may be seen as one building the tools of the future, but is he simultaneously securing ownership of the entire value chain, ensuring that when the inevitable problems – the energy crises, the logistical bottlenecks, and the social frictions – arise from this AI transition, he will be in a position to profit from the solutions to the very complications he helped create?

That would be a governance red flag that should make any disciplined investor pause.

Too big to fail – here we go again.

The most audacious part of the OpenAI strategy appears to be its attempt to become Too Big to Fail. By warning of AI dangers, including superintelligence and autonomous machines, AI CEOs secure government support. Then, by tying the AI infrastructure rollout to the power grid and seeking government “backstops” – as alluded to by OpenAI’s CFO – AI companies shift risk, privatise profits and socialise the losses.

If the AGI (Artificial General Intelligence) breakthrough doesn’t arrive as promised, or if the marginal cost of energy doesn’t “trend to zero” as Altman is reported to have claimed, the trillions of dollars currently being poured into data centres and specialised chips will produce the most expensive white elephants in history.

The bottom line

Altman and his peers say they want to build AI with humanity’s best interest at heart.

But in return, OpenAI is asking for electricity, water, infrastructure, capital, and your data.

And in exchange for the promise of some future technology that fixes everything,

AI companies are also asking humanity to adjust to a world riddled with deepfakes, data breaches and massive job losses.

We’ve all seen this movie before. Whether it was the dot-com boom or the Nifty Fifty, the ending is always the same: At the end of the hype cycle, lies a period of creative destruction. Price is what you pay, value is what you get.

You should prefer companies that pay you to own them, not companies that require a hope and a prayer.

Follow the money.

Footnotes:

[1] Sam Altman’s pledge:

“First, it’s always bothered me that users create so much of the value of sites like reddit but don’t own any of it. So, the Series B Investors are giving 10% of our shares in this round to the people in the reddit community, and I hope we increase community ownership over time. We have some creative thoughts about the mechanics of this, but it’ll take us awhile to sort through all the issues. If it works as we hope, it’s going to be really cool and hopefully a new way to think about community ownership.” Blog.samaltman.com, October 1, 2014 at 3:46 AM, 119786 views

[2] OKLO footnote:

From Robert Bryce/Substack: “In 2020, Oklo became the first US company in a decade to submit an application to the Nuclear Regulatory Commission to build and operate a nuclear reactor. Oklo went public in May 2024 via a SPAC backed by Sam Altman, the CEO and founder of OpenAI, and Altman was named chairman of Oklo’s board of directors. Five months later, Denver-based Liberty Energy, which was co-founded by Chris Wright, invested $10 million in Oklo. Wright served on Oklo’s board from May 2024 until February of 2025, when he was confirmed by the Senate to be Secretary of Energy. In September 2025, the company broke ground at Idaho National Laboratory on its first reactor project. About a month later, the company’s stock hit an all-time high of about $174 per share. In January, Meta (Facebook) announced a deal with Vistra, Oklo, and TerraPower to supply the tech giant with up to 6.6 GW of nuclear power by 2035. Oklo said that its part of the deal includes “plans to develop a 1.2 GW power campus” in Ohio to power Meta’s data centres in the region, and that it aims to “deliver up to the full target of 1.2 GW by 2034.” Although its stock price has plummeted over the past few months, Oklo remains the belle of the publicly traded SMR startups. Its market capitalisation of $9.7 billion makes it worth more than all of the public pure-play SMR companies combined. Over the past week … a deep dive into Oklo’s SEC filings [reveals] …significant selling by [CEO Jacob] DeWitte and [COO and co-founder and Dewitte’s wife, Caroline] Cochran.” Source, Robert Bryce/Substack.

[3] KoBold metals:

The investment in KoBold Metals is also reportedly part of a broader, high-stakes effort by tech investors to locate and extract rare earth metals in areas like Greenland, aimed at reducing reliance on Chinese supply chains.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.