Which companies will gain from a stronger Aussie dollar?

If you’re about to travel to the US, you’ll be gladdened by the trajectory of the Australian dollar (AUD). After falling to around US75c in December, it’s now buying around US80c. For Australian companies, however, the picture is far more complex. So I thought I’d have a look at some of the likely winners and losers from changes in the AUD.

How currency movements affect share prices

The movement in value of currencies impacts share prices in a few different ways:

- For companies that have a mismatch between their currency base of revenues and costs, changes in the value of currencies can have quite significant negative or positive impacts on margins. If you are an export oriented company with manufacturing in Australia (not so many of those left unfortunately) and the value of the (AUD) goes up vs the currencies you sell your goods in, you will most likely see a squeeze on margins; conversely, if the AUD goes down, your margins will benefit. If you are a company that is focused on imports, you will experience the reverse effect. This can of course be impacted by any hedging you undertake but the fundamental direction should still be the same. Since most companies are valued with some reference to their earnings power, changes in currencies will impact the share price. Long term changes in currencies will also have a long term impact on the relative competitiveness of different companies and industries.

- For companies with borrowings in different currencies, changes in the value of those currencies will impact the value of the debt that will eventually have to be repaid and hence have an impact on the share price as the value split between equity and debt will change.

- There are some companies that are dual listed and where the primary listing is not in Australia. The share price for these companies is generally set in the foreign currency and any changes in currencies should translate directly to the value of the Australian listed shares.

- Commodity prices are generally set in USD and companies that are either producers of commodities or heavy users of commodities are hence directly impacted by changes in currencies.

What is happening to the value of the AUD?

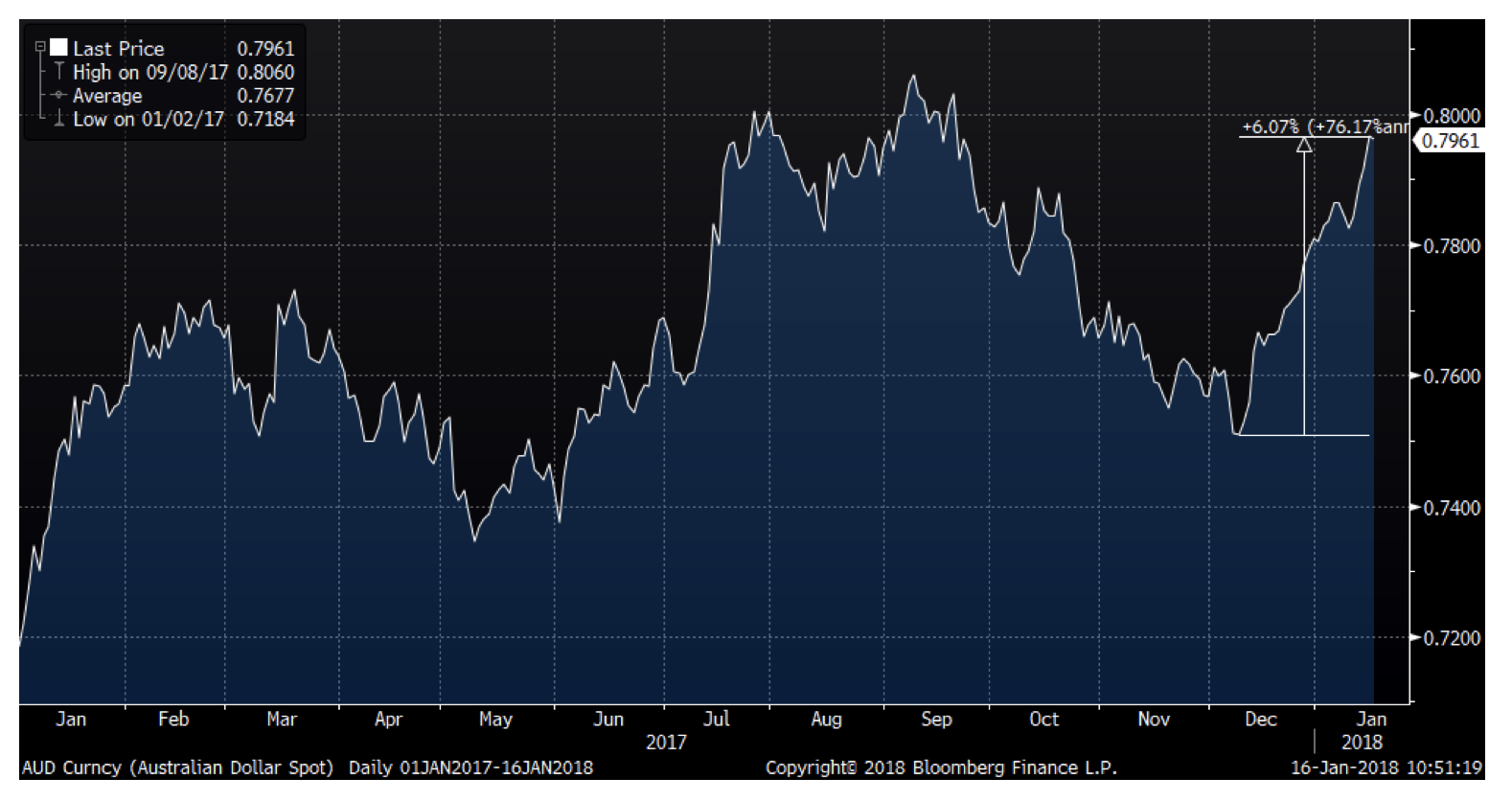

If we compare to the USD, we can see that the AUD has recently strengthened significantly by about 6 per cent from the low in early December. The current level is about 3.8 per cent above the average exchange rate in 2017, meaning that import oriented companies with the majority of their cost base in USD are seeing a free boost to their profits.

It is worth remembering that although USD is the world’s dominant currency, it is not the only currency that matters. If we instead compare to the Euro (EUR), the situation is reversed, with the AUD currently trading at a 4.5 per cent discount to the average level during 2017.

From this, we can draw the conclusion that it is really the USD that has been weak and not the AUD that has been strong, which is confirmed if we look at the DXY index which plots the USD vs all the other major currencies and which shows that the USD is trading at a 5.8 per cent discount to the average value during 2017.

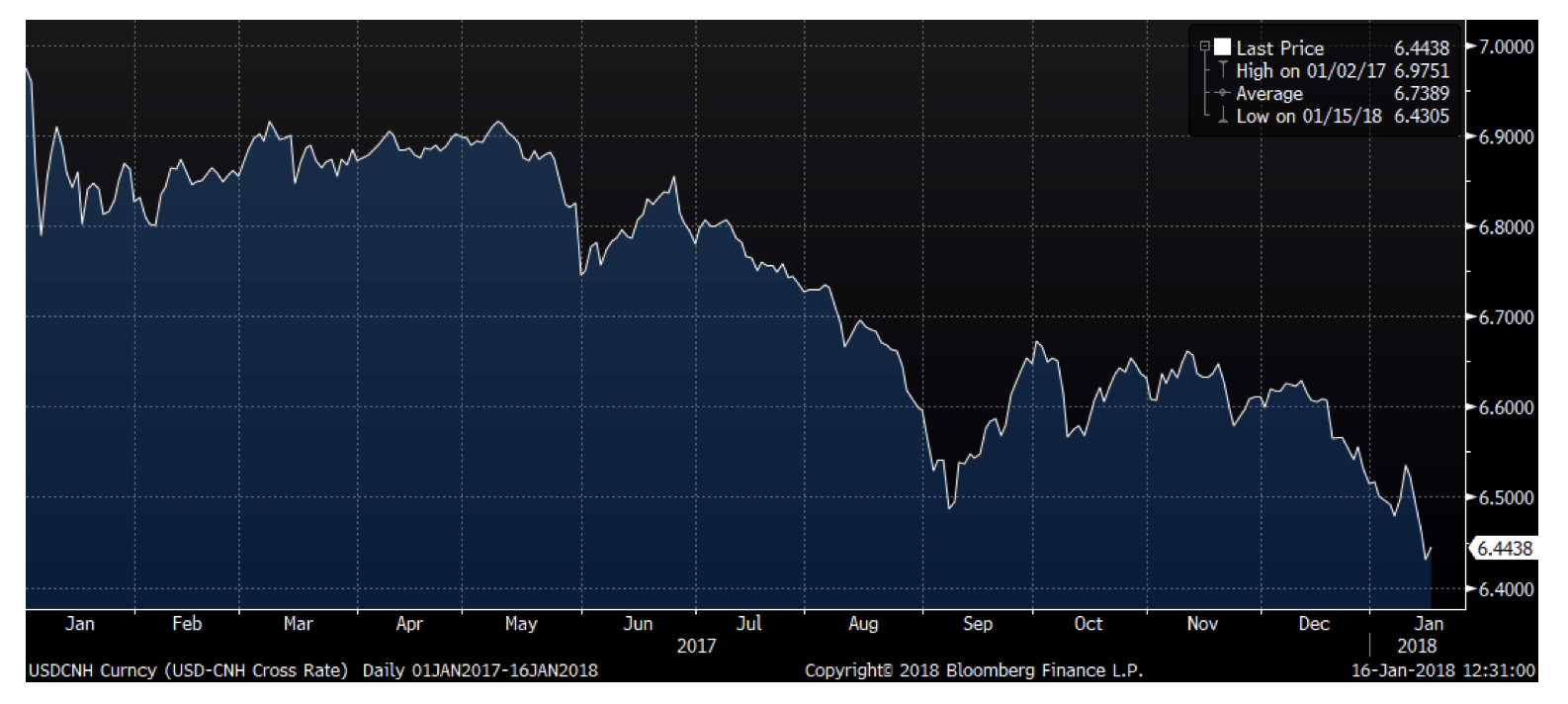

And if we look at the USD vs the Chinese Yuan, which is of particular interest to Australia (as China is by far the biggest purchaser of commodities from Australia and said commodities are priced in USD), we can see that the USD is trading at 4.5 per cent below the average level of 2017.

So what conclusions can we draw from this? Currencies can of course change quite rapidly so drawing very strong conclusions is hard, but some key ones I would highlight are:

- Australian companies with significant business in Europe are likely to see some benefit from the strong EUR. One such company is Ramsay Healthcare which has quite a bit of exposure to Europe. Another example is Sonic Healthcare where roughly one-third of revenues comes from its European operations. BT investment management is a third company benefitting from this due to the exposure to Euro denominated funds.

- Companies primarily listed in US with a secondary listing in Australia will see a negative translation effect on their share price. One such example is Resmed but in this case there are other offsetting factors as they have quite a bit of their cost base in USD and it is also a beneficiary of the proposed US tax corporate tax cuts.

- Weak USD is likely to improve the position for US companies and drive investor interest in US export oriented companies. This could have a negative impact on foreign interest in Australian stocks overall, especially combined with corporate tax cuts in US.

- It is probably on the margin positive for commodity companies as Chinese buyers of commodities are in effect getting a price cut on their purchases due to the strength of the Yuan vs the USD.

What do we think about the future of the different currencies? I would not proclaim to be an expert in currency forecast, but my inclination would be:

- The USD is probably too low at this point and I would expect a reversal due to the strong economic fundamentals we are seeing in the US.

- This means that the AUD should come down vs the USD and probably stay flattish vs the EUR.

- The big unknown is what will happen with China. If we were to see a slowdown in China due to credit contraction, we should expect the AUD to be quite significantly lower due to lower demand for commodities.

The Montgomery Funds own shares in Ramsay Healthcare, BT Investment Management and Resmed

If you’re about to travel to the US, you’ll be gladdened by the trajectory of the AUD. For Australian companies, however, the picture is far more complex, here are some of the likely winners and losers from changes in the AUD. Share on XThis post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY