The uneven effect on households

The easing cycle for the Western world has thankfully begun with each of the Canadian Central Bank, the European Central Bank and the Swedish Central Bank cutting their official cash rate by 0.25 per cent to 4.75 per cent, 4.25 per cent and 3.75 per cent, respectively.

In the recent report on the Canadian economy, Desjardins argue many Canadians are under serious cost of living pressure from the household debt to GDP ratio exceeding 103 per cent, whilst unemployment hit 6.4 per cent in June 2024. (Among the advanced economies, only Switzerland and Australia have a higher household debt to GDP ratio, relative to Canada).

Highlights include:

- Across all quintiles, the average percentage of disposable income dedicated to (mortgage) interest payments are much higher than it was before the pandemic. The proportion has gone up more sharply for households in the lowest income quintile.

- From the perspective of accumulated wealth, the lower quintile has negative wealth on average, meaning total assets are less than total liabilities. The lowest quintile spends all their disposable income on core personal consumption including housing, transportation and food, and are more likely to take our loans to “survive”.

- Looking specifically at more liquid assets, only the top two quintiles in terms of wealth have other financial assets greater than their debt, on average. Since 2021, only the wealthiest households have seen their real disposable income increase.

- The income gap between this group (the top quartile) and the rest of the population reached record levels in 2023. One of the reasons behind the growing disparity is that higher interest rates affect income distribution, benefitting the rich.

- In 2023, real consumption declined as households across the board cut back on discretionary spending. The lower three quintiles have been dis-saving as their income has not kept up with the rising cost of living and this population is more vulnerable to various economic or financial shocks.

- Generally, the housing crisis has negatively affected younger adults and advantaged older adults. The most indebted Canadians will get some relief as interest rates gradually come down over the next few quarters.

The Desjardins report also discusses gender inequality, limiting rising housing costs, and productivity gains being a key factor in raising incomes.

Apart from our lower unemployment rate (4.10 per cent), we could replace the word “Canada” with “Australia” and get an excellent update on how the higher interest rates are having an uneven effect on households.

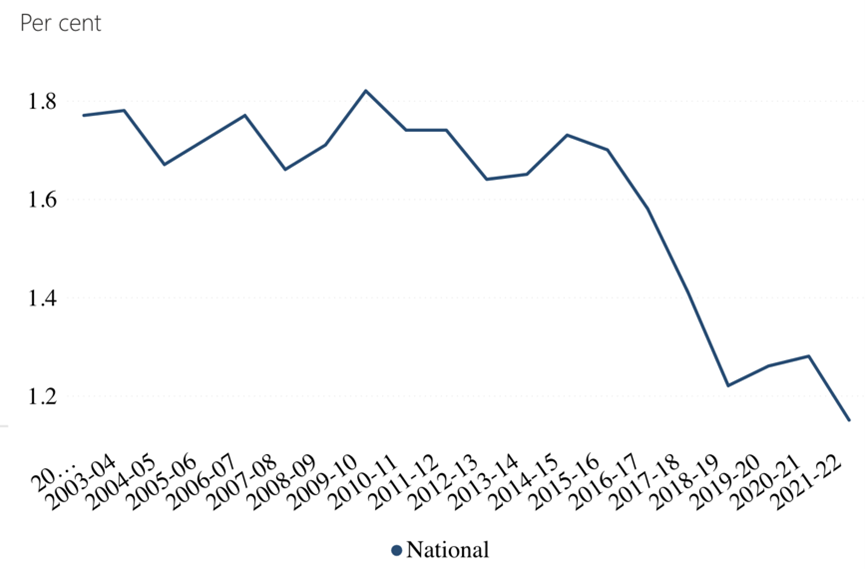

Australia’s 20-year average labour productivity growth

Source: ABS Australian System of National Accounts

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.