Should you be buying Fairfax Media?

Fairfax Media Limited (ASX: FXJ) announced yesterday that it has acquired 100% (up from 50%) of the shares on issue of Metro Media Publishing Holdings (MMPH). You can read the announcement on the ASX here.

In a nutshell, Fairfax will issue 68.5 million new shares which implies a transaction value of $72 million (including $18.5 million in cash). The firm’s current shareholders will receive 65% of their consideration in shares and the remaining balance in cash.

Naturally, a transaction such as this brings up queries about the prospects for Fairfax given their growing presence in the real estate listings market and whether this will derail any growth in REA Group’s realestate.com.au. On the latter point, derailment seems unlikely given REA’s dominance of the sector, which was discussed briefly here.

Getting back to Fairfax, we would first examine their current lines of revenue to see if a business that is making over $14 million in EBITDA per annum (according to MMPH CEO Anthony Catalano) will move the valuation needle. In short, not really, given that the firm has reported earning $306.4 million in EBITDA in FY14.

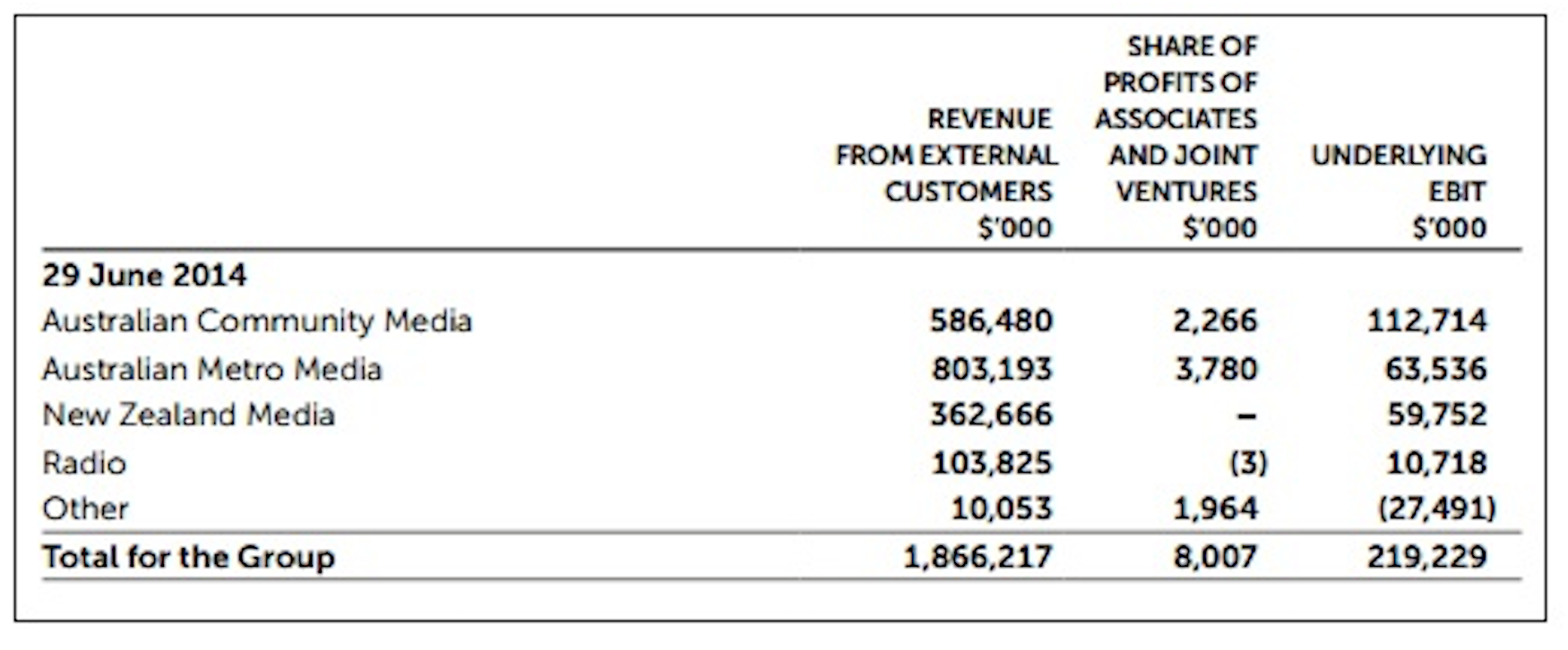

How about the prospects for some of Fairfax’s other businesses? The below table is sourced from the firm’s FY14 financial statement, page 136 for those interested.

I’ll focus on the top 3 lines, Australian Community Media (ACM), Australian Metro Media (AMM) and New Zealand Media (NZM). ACM is largely the firm’s print & online newspaper arm which unfortunately is well known to be in structural decline as news has become available online and for free. The same set of prospects can be said of NZM which operates a similar business model of print & online publications in New Zealand.

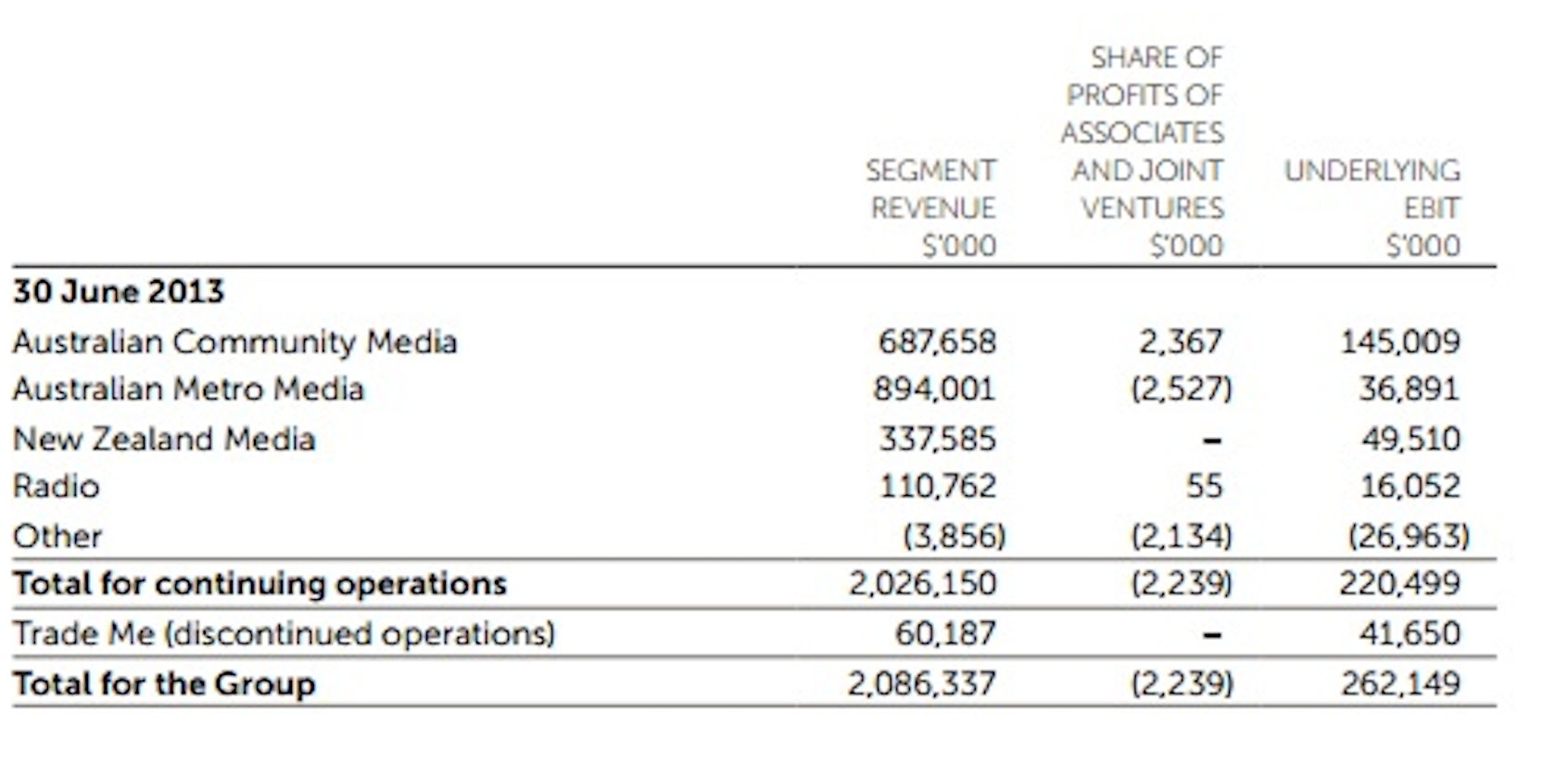

AMM includes print mediums but also includes classifieds. This segment despite its niche appeal also appears to be in decline. FY13’s spread of results versus business segment is below as a comparison.

The business as a whole does have some segments in growth, of which most notable is the Domain website, which will now incorporate the reviewproperty.com.au website originally owned by MMPH. But on the whole it doesn’t seem to stack up currently as a business with bright prospects.

Scott Shuttleworth is an Analyst with Montgomery Investment Management. To invest with Montgomery, find out more.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY

Some issues and questions I am pondering:

* A paperless office may not happen and print may not completely disappear

* The network affect on a market that has 70% market share may be able to be broken (depending on the market and its dynamics). If the market size doubles, maybe this will create an opportunity for a second company to increase market share

* I know Carsales ad numbers haven’t been so great lately.

* James Packer sold out of many of his online businesses some years ago making a lot of money.

* Is website network affect similar to newspapers network affect? There may be differences

I know of a couple differences between print and website that have implications

Scott, on Fairfax media….not a buy.

Kind regards,

Pam.

Scott,

media shares since the 1997/98 have been a fizzer for me. News limited boomed in the late 1990’s before the dot com drop. A friend of my son held News shares in the late 1990’s and was profitable. My son held News in his portfolio in 2003/04 and went no where. Capital appreciation is what to look for in these stocks, a la News back prior to the dot com crash. Divi’s are minimal and may not carry Australian imputation credits. Fairfax took a hammering several years ago. The future is online digital and online content. Who wants to pay for online content ??? Kind regards, Pam.