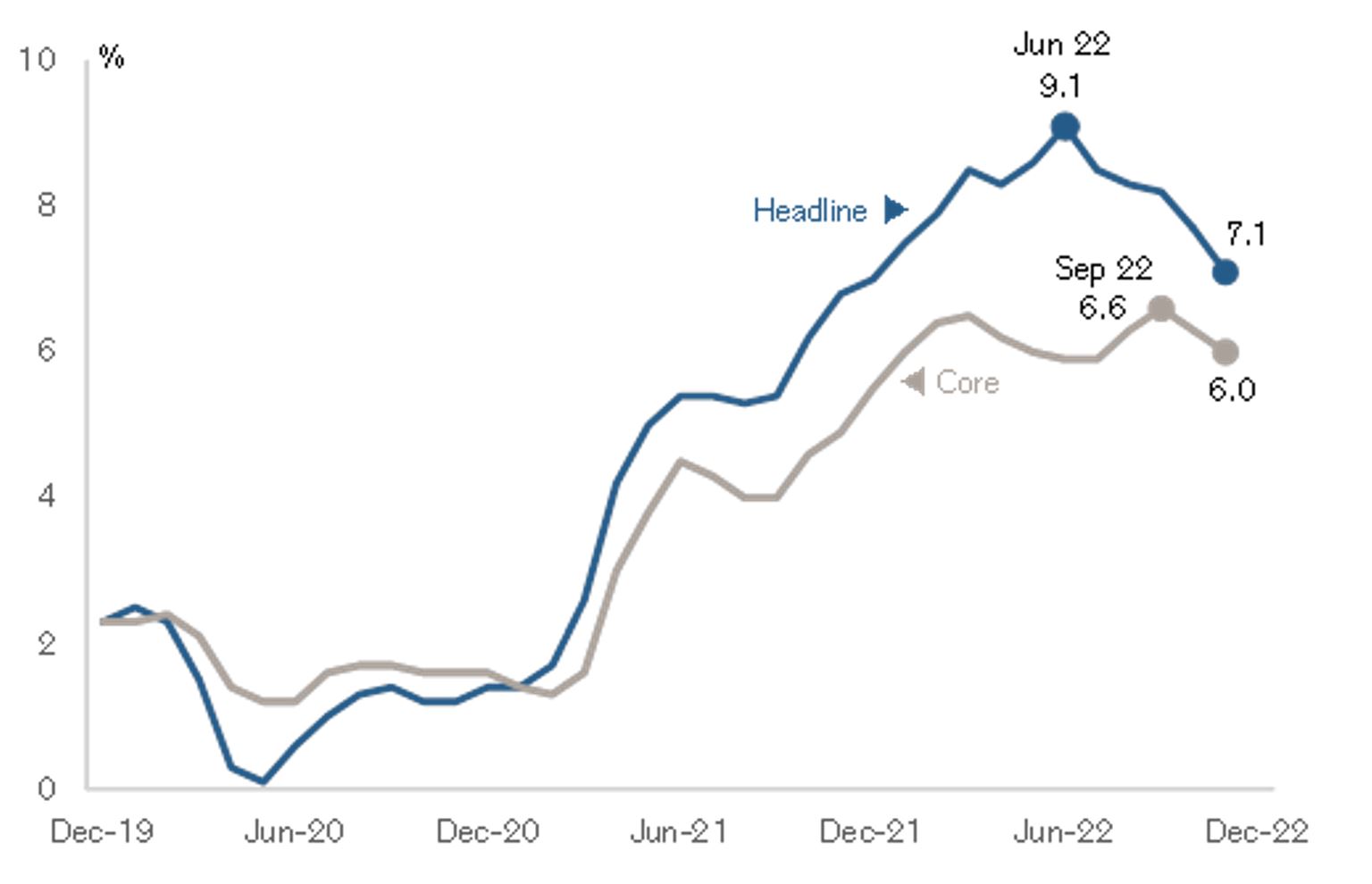

Market narrative to pivot from peak inflation to recession

Twelve months ago, official cash rates sat at record lows and only one English-speaking Central Bank – the Reserve Bank of New Zealand (RBNZ) – had commenced the tightening process in response to increasing inflationary expectations. The rapidly rising commodity prices coinciding with the war in the Ukraine (commenced 24 February 2022) finally got the attention of the English-speaking Central Banks and they followed the RBNZ typically with 8 or 9 “interest rate increases” over the balance of 2022.

Today, we have a situation where the official cash rate for the five English-speaking Central Banks, New Zealand, USA, UK, Canada and Australia, averages 3.87 per cent, with a range from 3.10 per cent (Australia being the lowest) to 4.25 per cent (New Zealand, the US and Canada). With the exception of the RBA, these are the highest official cash rates since 2008, when the Global Financial Crisis (GFC) really got going.

|

New Zealand Date |

% |

USA

Date |

% |

UK

Date |

% |

Canada

Date |

% |

Australia

Date |

% |

|

2021 |

|

|

|

|

|

|

|

|

|

|

6/10 |

0.50 |

|

|

|

|

|

|

|

|

|

24/10 |

0.75 |

|

|

16/12 |

0.25 |

|

|

|

|

|

2022 |

|

|

|

|

|

|

|

|

|

|

23/2 |

1.00 |

17/3 |

0.25 |

3/2 |

0.50 |

26/1 |

0.25 |

6/4 |

0.35 |

|

13/4 |

1.50 |

5/5 |

0.75 |

17/3 |

0.75 |

2/3 |

0.50 |

8/6 |

0.85 |

|

25/5 |

2.00 |

15/6 |

1.50 |

5/5 |

1.00 |

13/4 |

1.00 |

5/7 |

1.35 |

|

13/7 |

2.50 |

27/7 |

2.25 |

16/6 |

1.25 |

1/6 |

1.50 |

2/8 |

1.85 |

|

17/8 |

3.00 |

21/9 |

3.00 |

4/8 |

1.75 |

14/7 |

2.50 |

6/9 |

2.35 |

|

5/10 |

3.50 |

3/11 |

3.75 |

22/9 |

2.25 |

8/9 |

3.25 |

4/10 |

2.60 |

|

23/11 |

4.25 |

14/12 |

4.25 |

3/11 |

3.00 |

27/10 |

3.75 |

1/11 |

2.85 |

|

|

|

|

|

15/12 |

3.50 |

7/12 |

4.25 |

6/12 |

3.10 |

|

Number of increases |

9 |

|

7 |

|

9 |

|

8 |

|

8 |

Now we have early indications of declining inflationary expectations in the US which probably means further increases of Central Banks’ official cash rates in the March 2023 Quarter will be quite muted.

Nevertheless, with a move from an average official cash rate of virtually nil to an average expected to exceed 4.0 per cent in the near-term – post around nine separate increases in approximately twelve months – we are likely to see the market’s concern shift from “peak inflation” to “recession”.

Economic conditions in 2023

As investors, we need to ask ourselves what are the ramifications of recessionary economic conditions in 2023; and to what degree this has already been priced into the market? What I mean by this, for example, is to what degree has the twelve-month share price decline (to 15 December 2022) of 65 per cent for Meta Platforms (formerly Facebook), 51 per cent decline for Netflix, 48 per cent decline Amazon, 37 per cent decline for Google and 23 per cent decline for Microsoft, assumed a severe slowdown in demand by the consumer?

Importantly, which businesses will exit the forecast recessionary conditions in better shape, relative to their competitors? These are the ones – which have a sustainable competitive advantage – the businesses which should be part of any investor’s long-term portfolio.

Given share prices tend to go up by the staircase and go down by the lift shaft, an even more important question from an investors’ perspective is which businesses will exit the forecast recessionary conditions in worse shape, relative to their competitors? This implies a loss of differentiation or competitive advantage and the loss of an ability to sustainably “over-earn”. This “loss” often corresponds with a long-term decline in market rating and market capitalisation. And its these companies we need to avoid.

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.