Has Italy’s economy hit crisis point?

These days, most investors looking beyond our shores are focused on the US. But the situation in Europe is also worth watching closely, particularly in Italy – the world’s eighth biggest economy – which appears to be in dire straits.

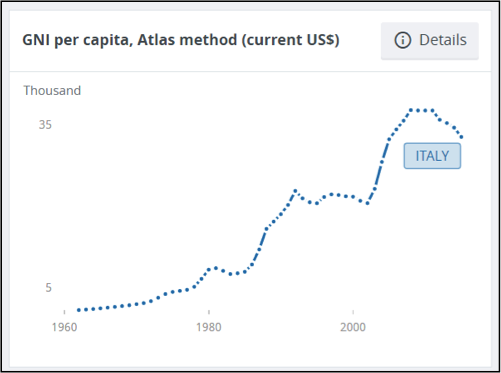

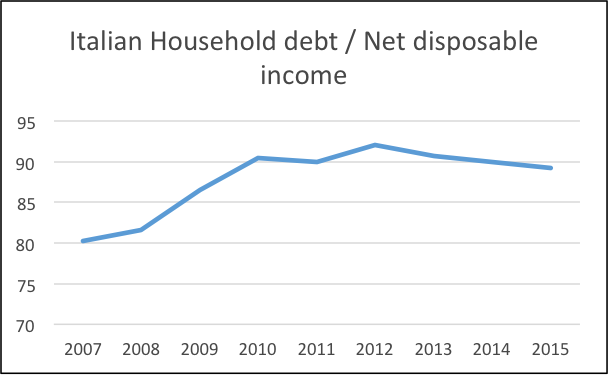

The main issue (as we see it) is high levels of debt in the economy or, more specifically, debt to income ratios in Italy are unsustainably high relative to the household’s ability to pay. With the country in recession, a downward cycle is being created whereby lower incomes push up debt/income ratios, which forces citizens to cut back on spending (to bring the ratio back down), which in turn reduces incomes, etc etc etc.

This is very easy to see in the economic data.

The optimal policy response from the government/central bank would be to:

- increase spending /pursue a pro-business agenda such as to raise nominal gross national product growth above that of the nominal interest rate;

- enact quantitative easing programs; &

- lower the currency.

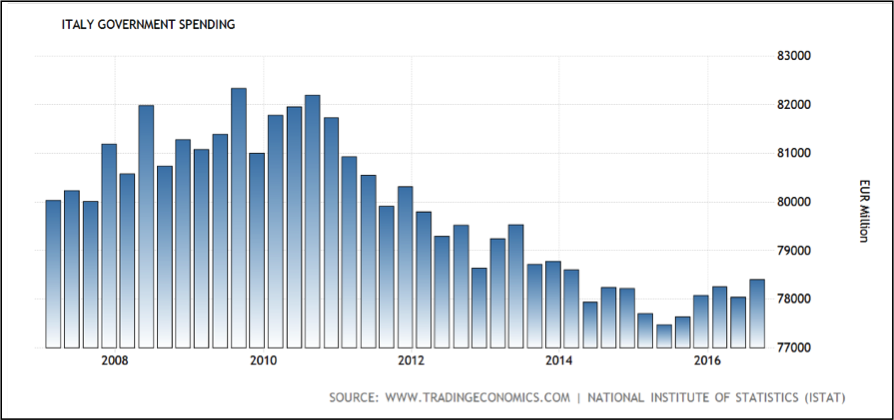

On all 3 fronts, however, the Italian government has either not enacted the correct policy or has had its hands tied (sometimes a little of both). On the first, it’s constrained by its own faltering economy (which results in lower tax revenues) and budget spending constraints. On the second and third, it has not the means to achieve these goals since this rests with the ECB. The effectiveness of these latter two points is a topic for another time.

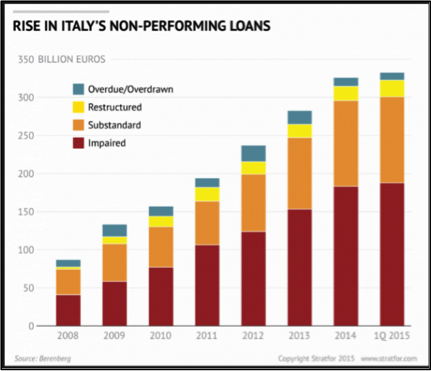

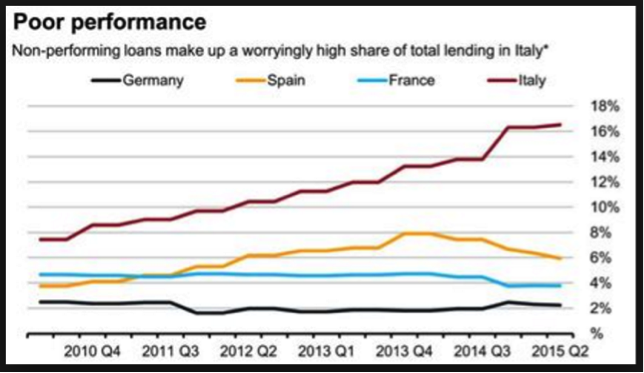

The debt to income ratio is falling for Italy, but in a slow and economically painful manner. Bad debts are skyrocketing (notably the other way for the debt to income ratio to fall is for citizens/companies to default).

It goes without saying that skyrocketing bad debts are toxic to the nation’s banking system. And this is where the risk really lies. Non-performing loans have grown to north of 360b euros in 2016. This is notably a very high proportion of the banking system’s overall loans and is clearly an unsustainable way for the banks to do business.

The crisis has already resulted in several banks receiving bailouts and it appears likely that more will follow. It can be difficult for the government, however, to bail out banks. EU bank bailout and state aid rules require that the bank first look for private injections of capital, ‘bail-in’ some bond holders and even scrape the deposits of some customers of the bank (ones with balances >90k euros). The impact is that many investors in the bank (Italians) lose out, further reducing wealth/income for citizens (e.g. about 40k retail investors own Monte dei Paschi bonds).

If the banking system were to collapse, however, via a loss of faith by depositors or out of control NPL’s, the key question would be the level of interconnectedness between the Italian financial system and that of other major EU countries (Germany, France, etc). If any large institutions had substantial assets invested in the Italian financial system, these may be impaired and allow for a spreading of the crisis.

Unfortunately, the prospects for Italy do not appear bright. The EU has recently asked Italy to further reduce its budget deficit (see here). As we know, since reduced government spending would simply lower the incomes of workers in the economy, this would just make a bad situation another tad worse.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY

As the great Sir John Templeton put it: “People are always asking me where is the outlook good, but that’s the wrong question. The right question is: Where is the outlook most miserable?”

From that perspective, Italy looks pretty interesting to me.