Generative AI’s growing impact on businesses

Over recent years, artificial intelligence (AI) has gained considerable traction. And on the back of the resultant excitement, price-earnings (P/E) ratios for stocks even remotely related have soared. Is the excitement premature?

McKinsey recently published an article titled The State of AI in 2023: Generative AI’s Breakout year, draws on the results of six years of consistent surveying and reveals some compelling findings. My takeaway is that service providers are buying the chips and working furiously to offer AI-enhanced solutions, but corporate customers are still some way off embedding those solutions in their own workflows. There exists a lack of understanding, necessitating more education.

The highest-performing organisations however, as showcased in the research, are already adopting a comprehensive approach to AI, emphasising not just its potential but also the requisite strategies to harness its full value.

Irrespective of the industry, and of whether they are service organisations or manufacturers, the most successful industry leaders strategically chart significant AI opportunities across their operational domains. McKinsey’s findings suggest that despite the buzz surrounding the innovations in generative AI (gen AI), a substantial portion of potential business value originates from AI solutions that don’t even involve gen AI. This reflects a disciplined and value-focused (cost) perspective adopted by even top-tier companies.

One of the critical takeaways from McKinsey’s research is the integration of AI in strategic planning and capability building. For instance, in areas like technology and data management, leading firms emphasise the functionalities essential for capturing the value AI promises. They are capitalising on large language models’ (LLM) prowess to analyse company and industry-specific data. Moreover, these companies are diligently assessing the merits of using prevailing AI services, termed by McKinsey as the “taker” approach. In parallel, many are working on refining their AI models, a strategy McKinsey labels the “shaper” approach, where firms train these models using proprietary data to build a competitive edge.

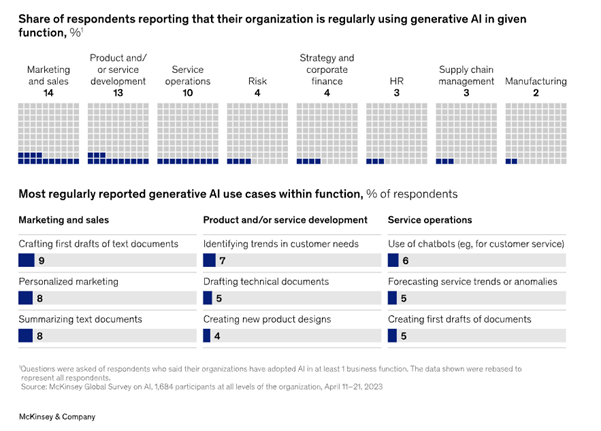

But the number of organisations doing so are relatively few (Figure 1.)

Figure 1. Gen AI is mostly used in marketing, sales, product and service development

Nevertheless, the latest McKinsey global survey reveals the burgeoning influence of gen AI tools is unmistakably evident. A mere year after their debut, a striking one-third of respondents disclosed that their companies consistently integrate gen AI in specific business functions. The implications of AI stretch far beyond its technological aspects, capturing the strategic focus of top-tier leadership. McKinsey quotes, “Nearly one-quarter of surveyed C-suite executives say they are personally using gen AI tools for work,” signalling the mainstreaming of AI in executive deliberations.

In other words, however, a common finding is individuals are using gen AI personally, but their organisation have yet to formally incorporate it into daily processes and workflows. This, despite the “three-quarters of all respondents expect[ing] gen AI to cause significant or disruptive change in the nature of their industry’s competition in the next three years.”

As an aside, AI’s disruptive impact is expected to vary by industry.

McKinsey notes, “Industries relying most heavily on knowledge work are likely to see more disruption—and potentially reap more value. While our estimates suggest that tech companies, unsurprisingly, are poised to see the highest impact from gen AI—adding value equivalent to as much as 9 per cent of global industry revenue—knowledge-based industries such as banking (up to 5 per cent), pharmaceuticals and medical products (also up to 5 per cent), and education (up to 4 per cent) could experience significant effects as well. By contrast, manufacturing-based industries, such as aerospace, automotive, and advanced electronics, could experience less disruptive effects. This stands in contrast to the impact of previous technology waves that affected manufacturing the most and is due to gen AI’s strengths in language-based activities, as opposed to those requiring physical labour.”

Moreover, the journey with AI isn’t devoid of challenges. McKinsey’s findings highlight a significant area of concern: risk management related to gen AI. Many organisations appear unprepared to address gen AI-associated risks, with under half of the respondents indicating measures to mitigate what they perceive as the most pressing risk – inaccuracy.

Drawing from McKinsey’s comprehensive survey, it’s evident that while the realm of AI, particularly gen AI, presents immense potential, it’s a domain still in its very early stages. Many organisations are on the brink of leveraging its power, but there’s still a considerable journey ahead in terms of risk management, strategic adoption, and capability building. As the landscape continues to evolve, McKinsey’s research offers a crucial ‘Give Way’ sign in the roadmap for businesses to navigate the AI frontier.

And that means there is every possibility the boom in AI-related stocks is a bubble. Stock market investors are notoriously impatient and if the benefits (measured in dollars) aren’t coming through investors will recalibrate their expectations. There is every possibility AI is as transformative for the world as promised, but the stock market’s journey is likely to be rocky, inevitably rewinding premature expectations ahead of more sober assessments. Think, ‘fits and starts’.

As a result, investors should have ample opportunity to invest in the transformative impact of AI at reasonable prices again and shouldn’t feel compelled to pay bubble-like prices amid a fear of missing out.

The full McKinsey article can be read here

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.