China’s non-financial corporate debt – it’s distressing

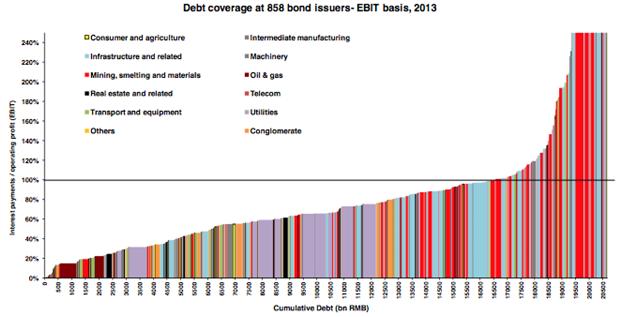

Over the 2009 to 2014 period, China’s non-financial corporate debt to GDP ratio has risen from 90 per cent to 120 per cent. Our friends at Macquarie Research have done some excellent analysis, collecting the financial data from nearly 3,000 companies that have outstanding bonds.

Our take is that at least half the companies in this survey are “financially distressed”. That is their debt-servicing ratio, or the ratio of Interest Payments to EBIT (Earnings before Interest and Tax), exceeds 65 per cent. Worse still, for twenty percent of the companies in this survey, Interest Payments actually exceed their EBIT, meaning they are producing a loss at the pre-tax level. That is their debt-servicing ratio is above 100%, and interestingly many companies within the “Mining, smelting and materials” sector have a debt-servicing ratio of 200 per cent.

Source: Wind, Company Data, Macquarie Research, September 2014

Source: Wind, Company Data, Macquarie Research, September 2014

The analysis also argues the corporate debt in China is disproportionately a State Owned Enterprise (SOE) issue. It seems likely the State will pursue some strong command signals via recapitalization, debt restructuring, asset disposals, SOE reform and in the case of the “Mining, smelting and materials” sector, some forced supply restrictions would not surprise.

Meanwhile, The Shanghai Composite Index remains 60 per cent below its 2007 all-time high, and while the incremental return on capital employed grinds down it is hard to get bullish on the Chinese stock market.

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.