Build it and they will come – growth stories and high multiples

One of the fundamental aspects of price discovery in the market is the speed at which participants are willing to price in future expectations for a business, adjusted for potential risks in execution.

To that end, the market has always been enamoured with businesses where the addressable market ie “the size of the pie” is significantly large, with a visible runway for growth many years into the future. Many of the top performers in the Australian market in recent years have been exposed to positive “structural tailwinds” including Chinese consumer-related companies (e.g. infant formula), Electric Vehicles and batteries (lithium, cobalt, nickel), wealth management platforms and certain specialised tech industries; where the primary focus is building capacity, or capturing market share as quickly as possible to take advantage of growing markets.

One such company that fits this description is NextDC, a data centre operator providing cloud connectivity and storage services with a national footprint. The company is exposed to trends of growing demand for data storage (which boasts exponential volume growth) and increasing maturity and adoption of cloud-based IT services; in fact, any estimate of growth in data creation is conservatively estimated >15 per cent CAGR for the foreseeable future – and with it – associated growth in services. Since 2015, the share price has more than tripled, reflecting investors’ optimism around the company’s future prospects.

While the share price may tell one story, it is interesting to observe the fundamentals for the business over this period. The chart from Bloomberg below tracks consensus forecasts for EBITDA in FY2018 (red) and FY2019 (green) over the past ~2.5 years versus the move in share price. EBITDA expectations have largely moved in one direction – the opposite of the share price – over this period. At its FY2018 earnings release, the company guided to continued growth in revenue of 20 to 24 per cent and EBITDA of 20 to 28 per cent in 2019, which is in-line with revised expectations.

NextDC consensus EBITDA forecasts for FY2018 and FY2019

Source: Bloomberg

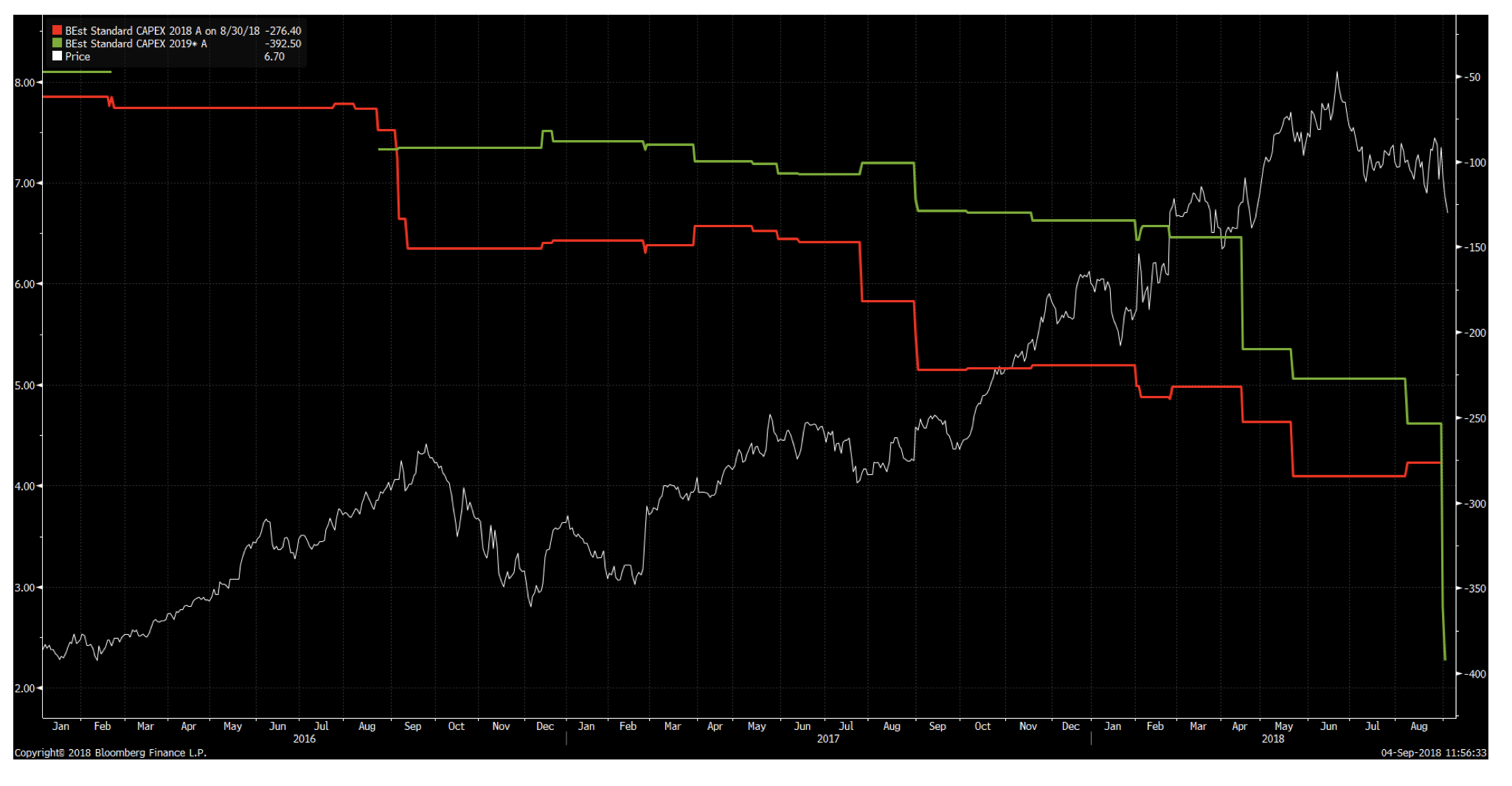

The company also provided capital expenditure guidance of between $430 million and $470 million – ~$200 million higher than prior expectations – in response to strong demand. The next chart tracks consensus forecasts for capital expenditure in FY2018 and FY2019. They too, have clearly moved in one direction – higher (or more negative).

NextDC consensus capex forecasts for FY2018 and FY2019

Source: Bloomberg

Clearly, the story of NextDC is “build it and they will come.” The company is investing in more data centres in Sydney, Melbourne, Perth and more capacity in Brisbane, which should increase the future earnings growth prospects. Its initial data centres in Brisbane, Sydney and Melbourne are effectively close to capacity, generating >65 per cent EBITDA margin with very attractive returns on capital of >20 per cent given premium locations and quality service. The company has built 46 MW of capacity to date with medium term plans to 306 MW, a more than 6-fold increase.

I have little doubt there will be increased demand for data centre services over time given increased migration towards cloud-based IT solutions, and big enterprise focus on data. However, with NextDC’s near-term earnings trajectory having largely been revised down over the past 24 months, the increase in share price implies a greater willingness from the market to pay more for future earnings growth now. For a long-term investor, a higher share price not only reduces the upside for good execution, it also reduces the margin for error by pushing back the time it takes for the company to grow in to its current valuation metrics.

As investors, it is important not to lose sight of the second part of future expectations equation – adjusting for potential risks in execution. While the market may be willing to overlook a slower ramp-up in sales or stretched valuation metrics for prolonged periods, it is important to acknowledge there are always risks to an investment thesis even for high quality companies in growth industries. Risks may be as simple and observable as the actions of a competitor, new substitute products, technological disruption, regulatory intervention, change in consumer preferences or may even constitute risks unknown at this point in time.

One area of risk you can control is the initial price of investment – and assessing the range of possible outcomes relative to what is being implied in the share price. This exercise will help determine whether the headline earnings metrics reflects an overvalued stock, or one where the market is undervaluing the potential for longer-term growth.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY