Bank reporting season highlights costs and slowing revenue growth

Over the last week, ANZ, NAB and Westpac reported their full year 2016 results, while CBA provided a trading update for the September quarter. So I thought it would be a good time to review the key themes to emerge.

But first, let’s go back to 21 September, when I posted a note setting out the six main variables to focus on when assessing the outlook for the banks:

- Loan book growth

- Net interest margins

- Non-interest income growth

- Cost growth

- Asset quality

- Capital requirements

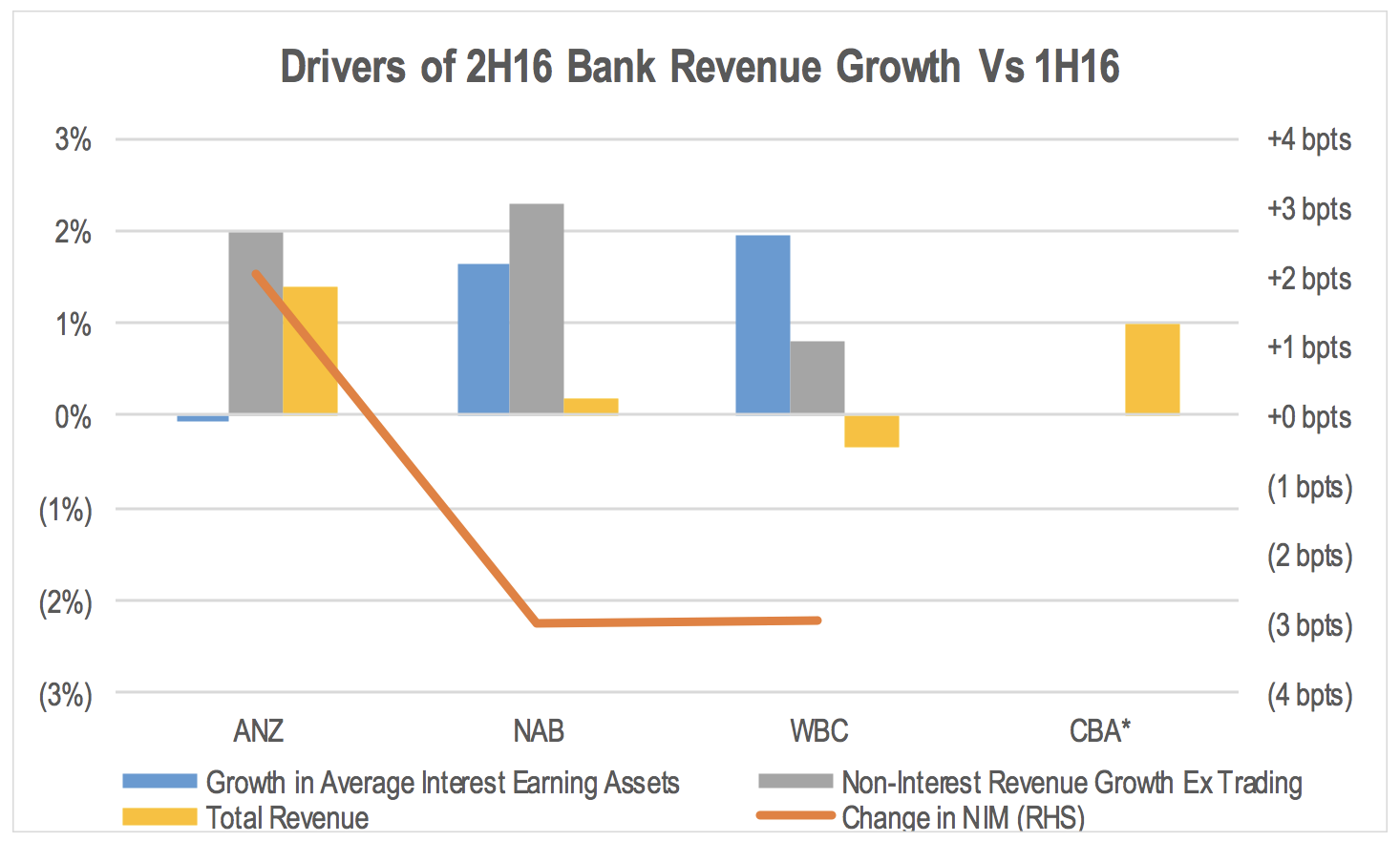

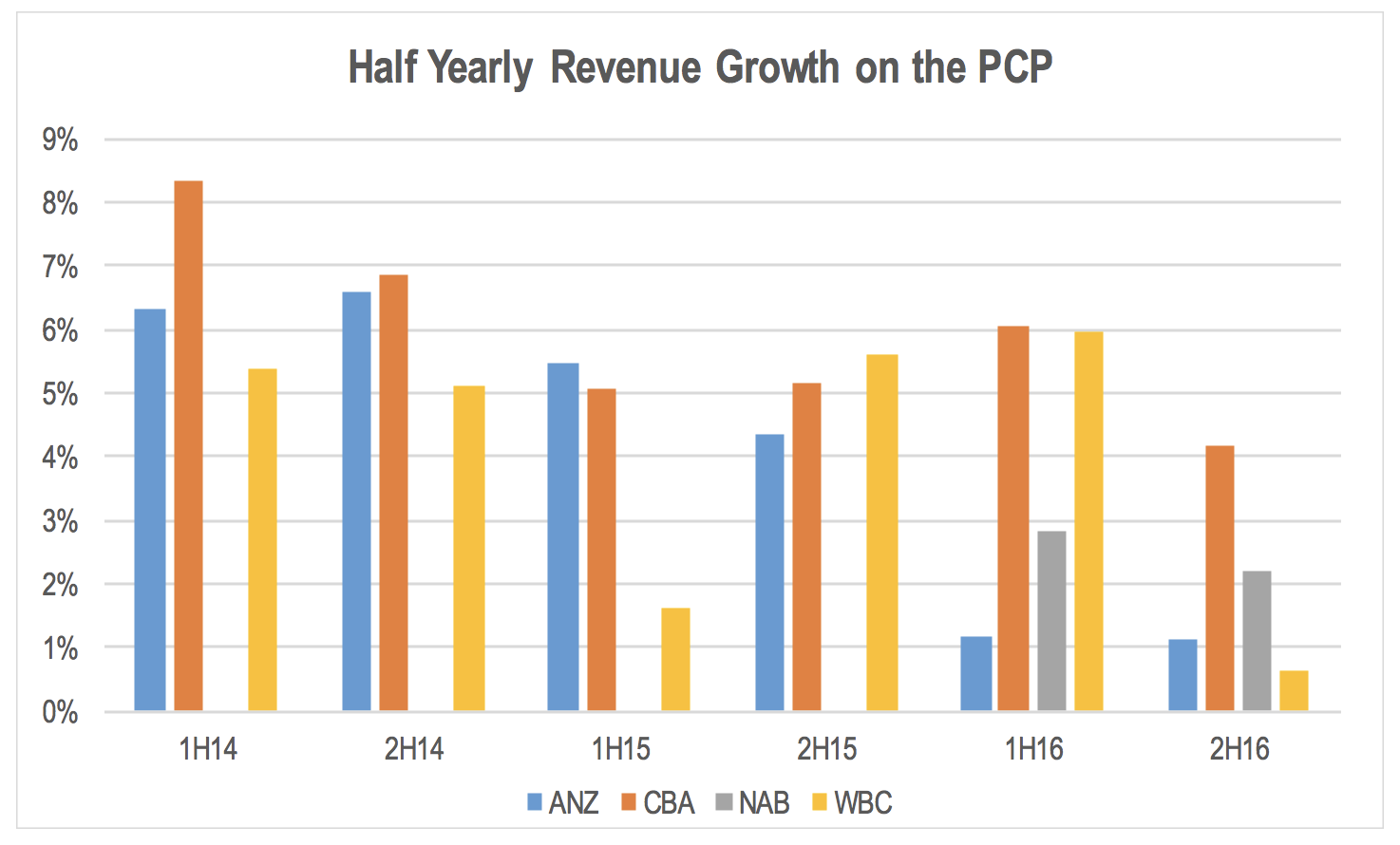

Of note in the recent results was the slowing rate of revenue growth. This was due to slowing loan book growth, combined with flat or falling net interest margins and continued difficulties in growing non-interest revenues. Non-interest revenues generally benefited from a recovery in trading revenues, but this is lower quality given the inherent volatility of this line item results from risk positions.

*CBA figure represents 1Q17

Revenue growth has slowed over the last few periods.

The pressure on net interest margins shifted from business segment to the mortgage book in the period, driven by the impact of passing on the full RBA rate cut in May to the variable mortgage rate, despite a limited ability to pass on the cut fully to deposit rates. This was offset later in the period by the partial pass through of the August rate cut. Net interest margins on mortgages were also negatively impacted by aggressive front book discounting earlier in the period. While this has eased more recently, this discounting will be flowing through the average pricing in the back book in coming periods. Rising wholesale funding spreads also negatively impacted margins.

Slowing revenue growth is shifting the focus to cost reductions in order to drive earnings growth. Despite this focus, operating earnings growth was generally fairly lacklustre. Expenses were generally well managed and fell slightly in the period. Only WBC failed to reduce reported costs in absolute terms. However, the picture wasn’t quite as positive if software spend capitalisation net of amortisation is added back to expenses.

Bad debt provision expenses were generally lower than expected, with underlying conditions stabilising after the deterioration in the six months to March. Provision charges also benefited from a reduction in larger single item specific charges. Mining regions and New Zealand dairy remained the main areas of noticeable stress.

The most positive aspect of the reported results was the common equity tier 1 (CET1) capital ratios reported. While the amount of CET1 capital generated during the period was generally in line with expectations, the period end risk weighted assets were lower than expected as a result of improvements in the mix of risk weights in the loan books, as well as improvements to data in modelling. This resulted in CET1 ratios that were 20-30 basis points higher than expected, offsetting the expected dilution of this key capital ratio from the increase in mortgage risk weights imposed by APRA from July.

The CET1 ratio is a key focus for the market as it is one of APRA’s main measures of the equity capital held by each bank against their businesses. The heightened focus on systemic risk following the GFC has resulted in regulators increasing the amount of equity capital banks need to hold. This has seen the major Australian banks retain more of their earnings as well as raising new equity to meet APRA’s increasing requirements. This dilutes sustainable returns, and therefore reduces the value to shareholders of loan book growth.

The expectation is that APRA will further increase the capital requirements applied to the major banks once it defines what it constitutes its previously stated “unquestionably strong” requirement. This is expected to occur sometime in 2017.

Higher than expected CET1 ratios as at 30 September 2016 potentially mean the major banks will not need to raise as much incremental capital going forward to meet the new APRA hurdles, reducing the risk to bank stocks of significant return and earnings dilution from large scale equity raisings and/or the need to cut dividends.

However, we note that the reduction in risk weighted assets in the period from data improvements might be unwound by Basel IV as it reduces the ability of banks to reduce their risk weighted assets through their accredited risk assessment models relative to using standardised risk weights.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.

INVEST WITH MONTGOMERY