Bulls now and then

While it may not inform your investing decisions, it’s undeniably enjoyable to look at what bulls were saying during a previous bubble and comparing those comments to what is being said today.

In this post, I compare the statements from the latest post of stock market bull Ed Yardeni, and the statements made in the April 1999 Merrill Lynch report entitled ‘e-Commerce: Virtually Here’.

Published on 8 April, 1999, the section beginning on Page 13 and titled The Epicenter, was authored by Henry Blodget. According to The Guardian, “As the dotcom bubble was rapidly expanding in the late 1990s and early 2000s, Blodget was arguably the world’s most famous financial analyst, named Institutional Investor’s “all-star” analyst three years running and taking home a salary of US$12m from Merrill Lynch.”

Figure 1. The April 1999 Merrill’s Report.

Source: Montgomery

Ed Yardeni 2026: The bears say the exuberance is irrational, driven by lots of excitement about artificial intelligence (AI). We say it is rational, based on our Buzz Lightyear Theory (BLT) of “To Infinity and Beyond!” According to our BLT, there’s a fourth factor or [sic] production, not just the historically recognised three. In addition to land, labor, and capital, which are relatively scarce, there’s now data, the supply of which is unlimited.

Merrill Lynch 1999: It is important to keep in mind that a major driver of internet stocks is an imbalance of supply and demand. The price of any good or service is determined not by its inherent “worth” but by the law of supply and demand – and good internet investments are in short supply and great demand.

Ed Yardeni 2026: Instead of focusing on rational versus irrational exuberance, let’s compare FOMO to FEMO. The former stands for “Fear Of Missing Out.” Investors pile into stocks, bidding up their price-to-earnings multiples. FEMO is “Fabulous Earnings Momentum.” Analysts raise their earnings estimates because hard data and company guidance give them reason to do so.

Merrill Lynch 1999: Stocks go up or down not because they are trading at particular multiples of published projections but because, for a variety of reasons, investors decide to buy or sell them.

Ed Yardeni 2026: This year has been all about FEMO (Fabulous Earnings Momentum). Through Friday, the S&P 500 is up 9.2 per cent year-to-date (ytd), forward earnings is up 14.4 per cent, and the forward price-to-earnings (P/E) is down 4.6 per cent. The entire rally has been driven by forward earnings. The multiple has contracted. FOMO inflates the P/E. This market did the opposite. That is why we are not in the bubble camp. FOMO is based on hope and hype. FEMO is based on fundamentals. At 21.1 times forward earnings, the S&P 500 is not irrationally valued unless a recession is coming in the foreseeable future. We don’t see one.

Merrill Lynch 1999: For several reasons, moreover, we believe that even when viewed through the lens of a more rigorous valuation framework, the stocks are worth more than the casual observer might think. These reasons include: 1) that no one knows with any degree of certainty what the future cash flows will be or what the real risk associated with them is (the leading companies have been blowing away expectations from the get-go); 2) the potential for unprecedented returns on invested capital, which will ultimately equate to higher P/E multiples, and 3) benefits from the “network effect,” through which franchises are made more valuable and sustainable with every new customer or supplier they add.

It’s said history doesn’t repeat, but it certainly appears to rhyme. Whether analysts and strategists are unwitting pawns in a greater game of chess or victims of the fads and fashions of the day, it certainly seems they respond similarly to price stimuli across time and space.

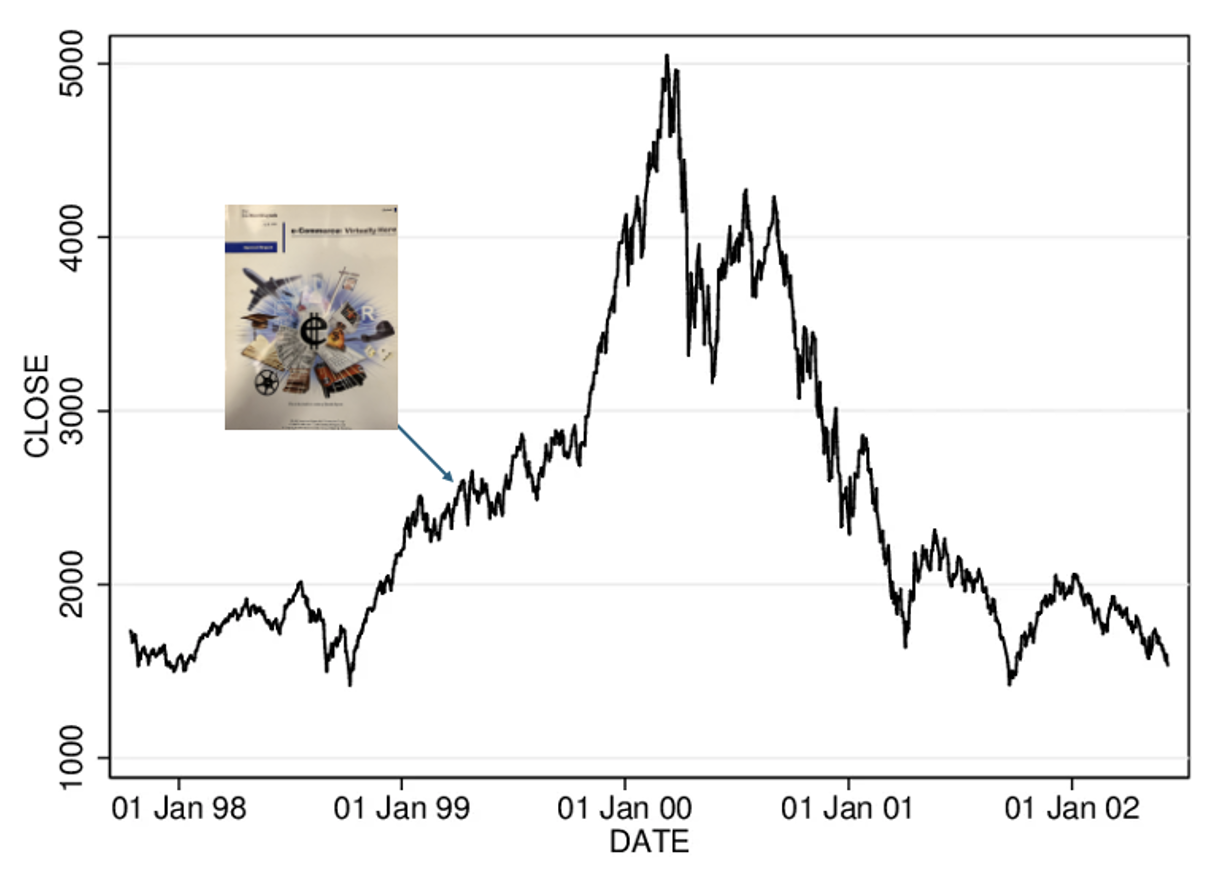

Figure 2. NASDAQ composite index 1998-2001

Source: Montgomery

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.