What’s war good For? Markets tell a different story

What’s war good for? With apologies to Motown songwriters Norman Whitfield and Barrett Strong, absolutely nothing from humanity’s point of view. While the human cost of conflict – measured in lives lost, families displaced, and immense suffering – is profound and undeniable, the historical relationship between geopolitical chaos and long-term market valuations is remarkably detached, perhaps because markets grind on, focused on profits and with what appears to be indifference to the tragedies that dominate the headlines.

Historically, at least, equity markets decline ahead of conflict as investors brace for the unknown, but rally during it, often led by rotations into sectors that profit from the chaos.

Today, many investors are asking whether the current Middle East conflict will reveal markets to be equally resilient (and indifferent).

Before we dive in, it’s worth making a few observations about the current conflict in the Middle East.

The first is the resulting supply shock will trigger price rises of many goods. It is already increasing the price of money as interest rates rise, and in so doing, causing the cost of capital to rise with consequences for merger financing, which in turn will hurt deals, hurt the prospects for bailouts, and, through the impact on the very wealthy, discredit political leaders worldwide, especially those aligned with Trump.

In fact, it’s reasonable to conclude that many of the follow-on effects of this supply shock are adverse, including on living standards across the world.

The World Wars’ impact on markets

During the two World Wars, the U.S. stock markets generally performed positively despite initial panic. In WWI (1914–1918), following a 30 per cent drop when markets reopened after war broke out, the Dow Jones rebounded significantly, rising 88 per cent in 1915 alone and finishing with a 43 per cent gain (8.7 per cent annualised). In WWII, despite a 4.37 per cent drop after Pearl Harbour and volatile periods like the fall of France, the Dow gained 50 per cent (7 per cent per year) by the end of the conflict.

Importantly, the United States’ entry into World War II saw equity markets reach their low point in 143 days and return to higher ground within a year.

Combined, equity markets displayed resilience through high volatility, often turning early losses into long-term gains.

Despite these encouraging stats for investors, I think it’s reasonable to ask whether a world war in 2026 or 2027 would result in equally resilient stock markets. Drones, autonomous soldiers, artificial intelligence (AI) and the ever-present threat of nuclear ‘solutions’ make WWIII a far less palatable prospect, even for investors.

But the current conflict in the Middle East is not a world war and doesn’t appear to bear the essential ingredients for one to start. Yet. A defining feature of world wars is the formal commitment of multiple global superpowers to fight on behalf of their allies. And unlike the pre-nuclear era of 1914 or 1939, the presence of nuclear weapons among major powers (the U.S., Israel, Russia, and China) acts as a catastrophic deterrent.

2026 – the year of diversification

We’ve written extensively about the current Middle East conflict, oil, U.S. inflation, AI, the associated Software-as-a-Service (SaaS) apcolypse (also known as: the SaaSpocalypse), U.S. debt, gold and the de-dollarisation trade, and long bond yields. And while many of those topics allude to the need for diversification, we were also much more specific. Beginning in 2025, we explained that 2026 would be the year when investors would benefit from some earlier tactical diversification into investments uncorrelated with public markets.

The arguments were relatively straightforward: an unpredictable U.S. president, mid-term election years tending to be tougher for equities – especially between May and September, weaker equity markets and larger drawdowns during Republican presidencies going back 125 years, a fourth consecutive strong year in equity markets being an exception and very stretched stock market valuations.

With the S&P 500 down 4.3 per cent and the ASX 200 down 2.04 per cent year to date (YTD), there’s not much in returns, so far, worth writing home about.

Recent conflicts and returns

In February 2022, when Russian tanks rolled into Ukraine, the S&P 500 subsequently sold off 16 per cent, bottoming in June before rallying 16.5 per cent and then beginning a more significant decline into October 2022 as interest rates were raised to fight the inflation after-effects of COVID-19.

During that period, the domestic ASX 200 fell three per cent between the 18th and 25th of February, rallied 7.5 per cent over the next two weeks, and then declined 14 per cent to the end of September in sympathy with overseas markets and in reaction to rising interest rates.

Given persistent inflation and the central bank responses globally, we cannot say with certainty how much of the moves were related to the war in Ukraine.

What we can say, however, is that interest rates were also a factor in many other past geopolitical conflicts, and despite this, a pattern emerges that might give investors some encouragement. We can also say that rising or high rates are a familiar factor today as the Middle East conflict devolves.

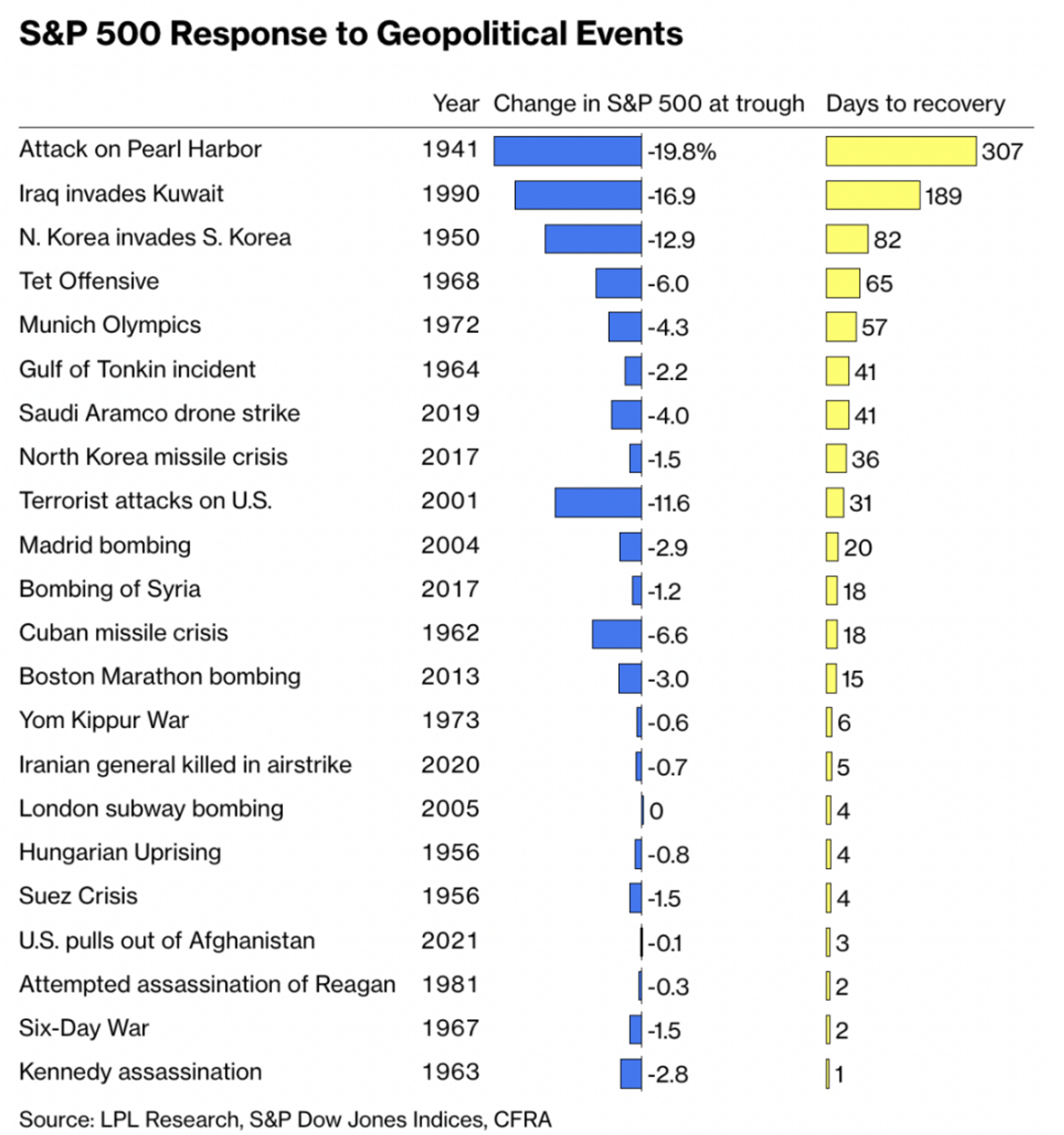

Table 1. S&P 500 Response to geopolitical events

As Table 1., reveals, data provided by market strategist Ryan Detrick at LPL Financial highlight the resilience of equity markets across decades of volatility. In his 2022 analysis of twenty-two major non-financial shocks dating back to the attack on Pearl Harbour, Detrick found that the immediate market reaction was often a brief, sharp dip followed by a swift recovery.

As Table 1., reveals, data provided by market strategist Ryan Detrick at LPL Financial highlight the resilience of equity markets across decades of volatility. In his 2022 analysis of twenty-two major non-financial shocks dating back to the attack on Pearl Harbour, Detrick found that the immediate market reaction was often a brief, sharp dip followed by a swift recovery.

On average, these events triggered a one-day loss of just over 1 per cent, with total drawdowns bottoming out at less than 5 per cent. Of course, that’s already been exceeded in this 2026 conflict, revealing the limitations of averages. Perhaps most surprising, however, is the speed of past rebounds; it typically took fewer than twenty days to hit the floor and only about six weeks to bounce back entirely.

This pattern of resilience is heavily influenced by geography and economic scale. The United States enjoys a unique position as an isolated superpower, making existential threats to its currency or markets relatively low compared with those of more vulnerable nations.

The historical record for smaller or more centrally located countries is grimmer; investors in Poland in 1939 or Russia in 1906 faced catastrophic losses that were not easily erased by a quick market bounce. Furthermore, while a country like Russia has a Gross Domestic Product (GDP) comparable to Canada’s – a relatively small piece of the global pie – the danger lies in how a localised conflict might escalate or disrupt broader supply chains.

It’s worth acknowledging a small economic engine like Iran can still throw a massive spanner into the global works if the war expands beyond its initial borders, adversely impacting supply chains, which the current conflict has already done.

Ultimately, the takeaway for today’s equity investor is not to become callous or complacent, but to recognise the danger of making emotional trades based on the morning’s headlines. Drawing a straight line from a tragic news event to a portfolio strategy is a path fraught with error, as markets have a storied habit of stumbling over the immediate headline only to return to focusing on profit growth and thematics a few weeks later.

Despite the constant hum of geopolitical commentary in our news feeds, successfully trading on these forecasts remains notoriously difficult. Markets are inherently forward-looking, and they tend to prioritise commerce over the temporary, albeit terrifying, noise of conflict.

And history seems to favour investors who consider a five- or ten-year view and take advantage of the chaos, rather than those who react emotionally.

Further encouragement

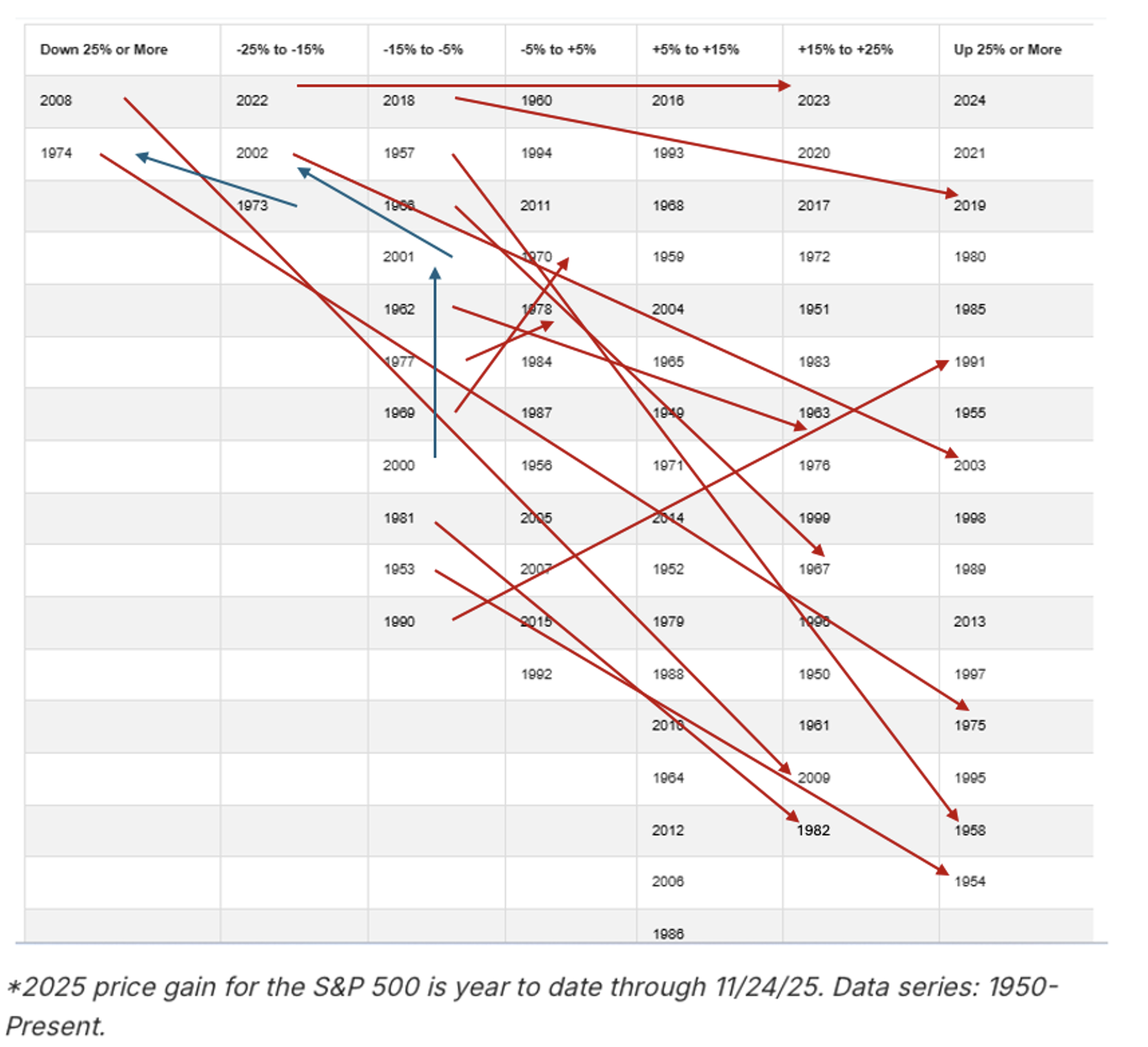

For committed share market investors and those for whom a ‘tactical’ response is anathema, it’s worth knowing the pattern of historic returns, particularly what tends to happen after a very weak year.

As Table 2., shows, very weak years in markets are usually followed by very good years. In fact, since 1950, there have been sixty years that produced returns of greater than -5 per cent. Notably, however, there have been sixteen years in which the S&P 500 has fallen by more than five per cent.

Of those 16 years in which the S&P 500 fell by more than five per cent, only three were followed by another negative year. 81 per cent of all negative years greater than five per cent, were followed by a positive year and all but two produced a return greater than 15 per cent.

Table 2. S&P 500 performance (1950 – 2025)

Source: LPL Research, Montgomery

Source: LPL Research, Montgomery

Conclusion

If this conflict proves to be as temporary as weak stock market years, investors and the conflict’s survivors could be cheering together.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.