The risk of underspending in retirement

I think a lot about how higher-yielding income products, such as the Aura Private Credit Income Fund and the Aura Core Income Fund, might fit in a retiree’s portfolio and how to articulate that.

It’s a challenge to explain, primarily because we don’t know the future. We don’t know how long we’ll live; we don’t know when/if the stock market might crash, and therefore we don’t know how much we can withdraw each year from our retirement savings because we don’t know how much we will spend in retirement, nor how much we’ll actually have left each year.

It leaves many investors paralysed; “I’ll worry about it tomorrow.”

Admittedly, those unknowns are a big reason as to why so many investors are diversifying their portfolios into alternative strategies that have little to no correlation to public markets, like private credit.

Some investors simply want to know the options that are out there so they can make an informed decision on where to invest their money – taking into account their personal situation and objectives, of course.

Take Aura Private Credit Income Fund as an example. A sophisticated or wholesale investor might be interested to know that if they invested in this fund eight and a half years ago, they could have earned a compounded return of 9.47 per cent (as of 31 January 2026) on a monthly distribution reinvestment basis. This exceeds the return of the ASX 200 Accumulation Index (9.42 per cent, compounded over the same period) but without the volatility. Noting that past performance is not an indicator of future performance.

It is also worth noting that this fund offers investors a choice to receive the monthly cash payment rather than engaging in a Distribution Reinvestment Plan (DRP).

The answer is ageing itself.

For a great many others, however, they will say, ‘That was then, but this is now.’ And among those nearing retirement today, many rightly worry they might not have enough to enjoy their best life in retirement.

Beneath that concern lie two risks: One is the risk of outliving one’s assets, and the other is the opposite; the risk of chronic underspending. Yes, many worry about the money running out, and, by doing so, they rob themselves of the enjoyment of the retirement they prepared for.

While I think I can allay many of those concerns with providing information on alternative investment strategies, such as our private credit funds, there are some retirement behaviours we can observe that achieve the same.

Consider, for a moment, the infamous ‘4% Rule’, which underpins retirement plans around the world. It’s praised as a ‘safe’ withdrawal rate for your portfolio and was devised by U.S. financial adviser Bill Bengen after he studied how much his clients could withdraw from conventionally diversified portfolios without running out of money.

Taking into account the largest stock market crashes in history, the 4% Rule was created to protect against the worst-case scenario. Withdraw no more than 4% each year and even after the worst stock market crashes history has thrown at people, you should have enough to last.

Most of the time, however, the worst-case scenario doesn’t happen, so you end up under-spending based on your portfolio’s potential. And if you have less in stocks and bonds and other ‘public’ market securities – perhaps swapping out some of the public market bonds or stocks for private credit, for example, the concerns about stock market crashes reduce meaningfully because the correlations between the assets in the portfolio are lower.

But there’s something else to keep in mind.

While the 4% Rule and similar guidelines assume life is steady and predictable, we all know that’s not an accurate reflection of real life. Life can be unpredictable, and so can spending.

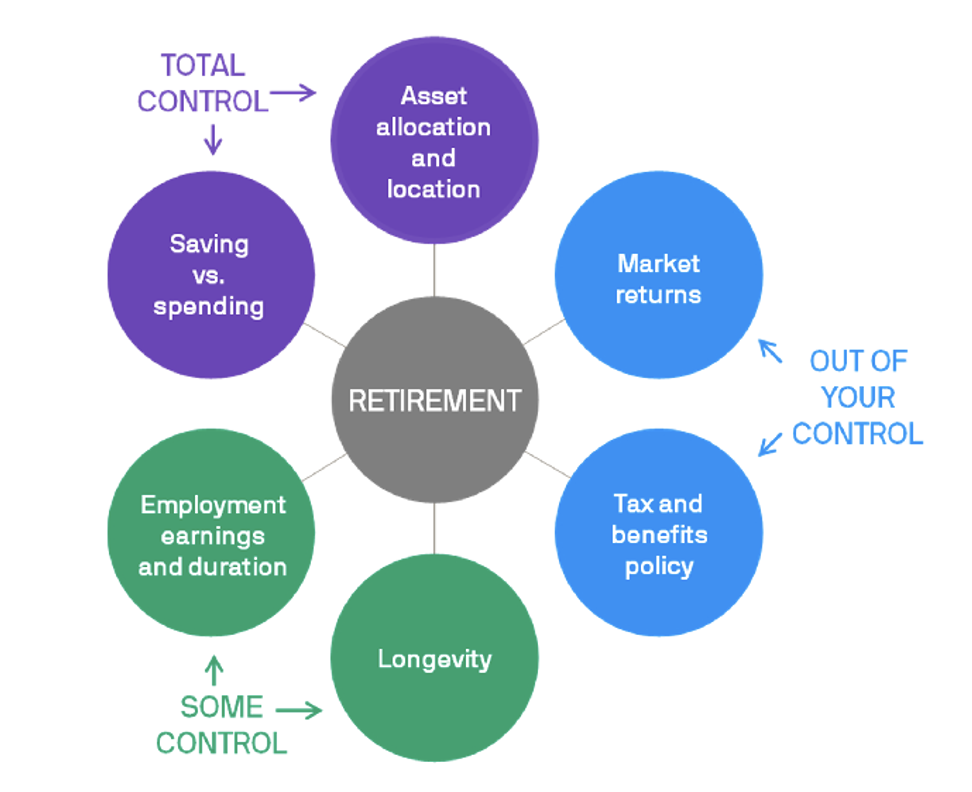

Figure 1. Controllables

Source: JPMorgan Asset Management

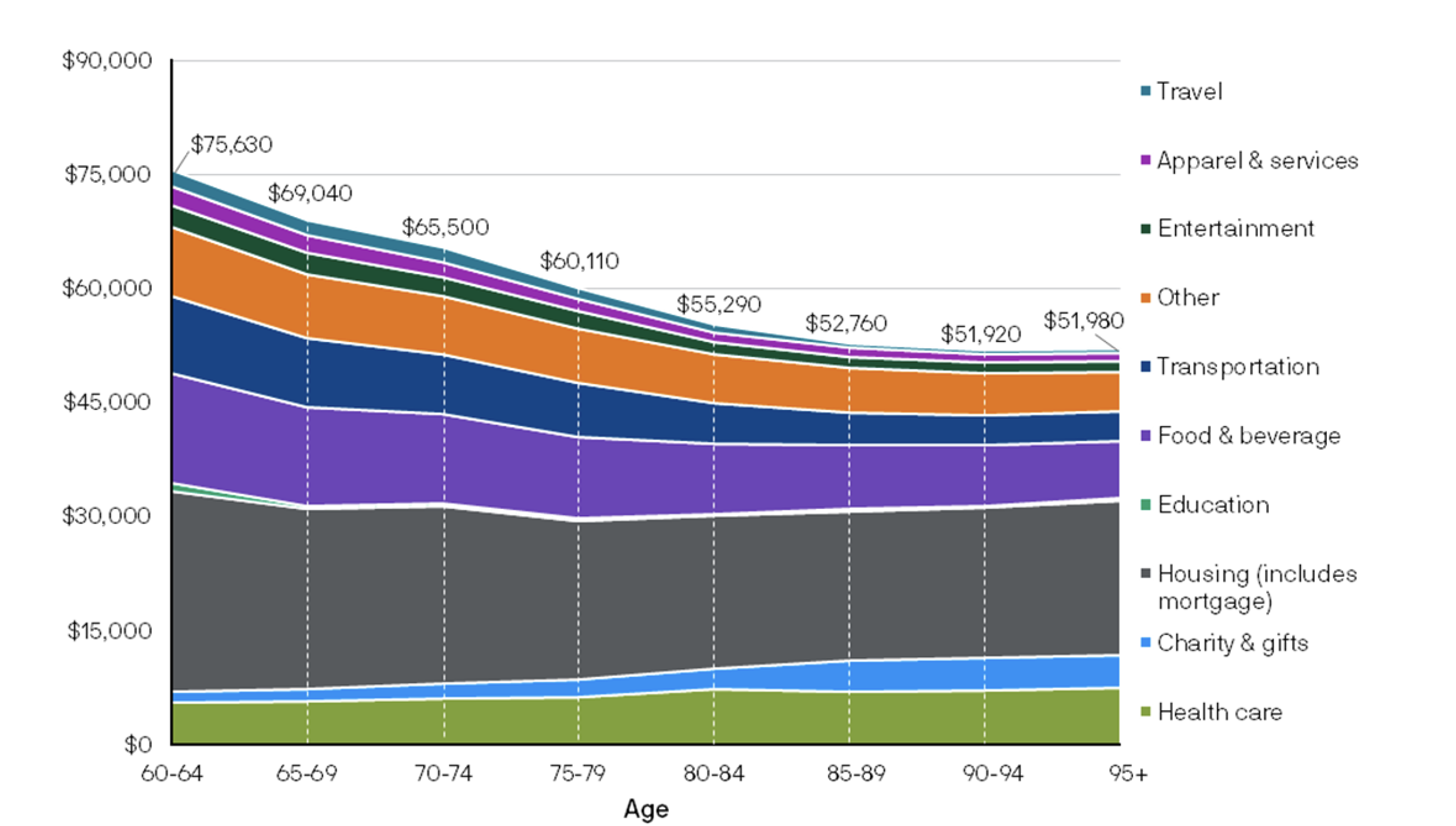

In fact, a 2025 JPMorgan study of retirement found that spending peaks near retirement age and then declines steadily.

Figure 2. Changes in spending: Partially- and fully-retired households with US$250k-US$750k investable wealth

Source: JP Morgan Asset Management.

As Figure 2., reveals, average spending declines from the early part of retirement, then tends to flatten out. JP Morgan demonstrated that at older ages, people tend to spend less on all categories except health care and charitable contributions. And those who live to the oldest ages may have costs related to long-term care.

We all remember asking what Grandma wanted for Christmas, and her reply: “a big hug and a kiss”. As we age, we want less (although we might ‘need’ a little more later).

The good news, then, for those at or near retirement, is that while you might expect to maintain your current spending for many years, those who went before you didn’t.

Your peak spending will probably be right on or near the year you retire.

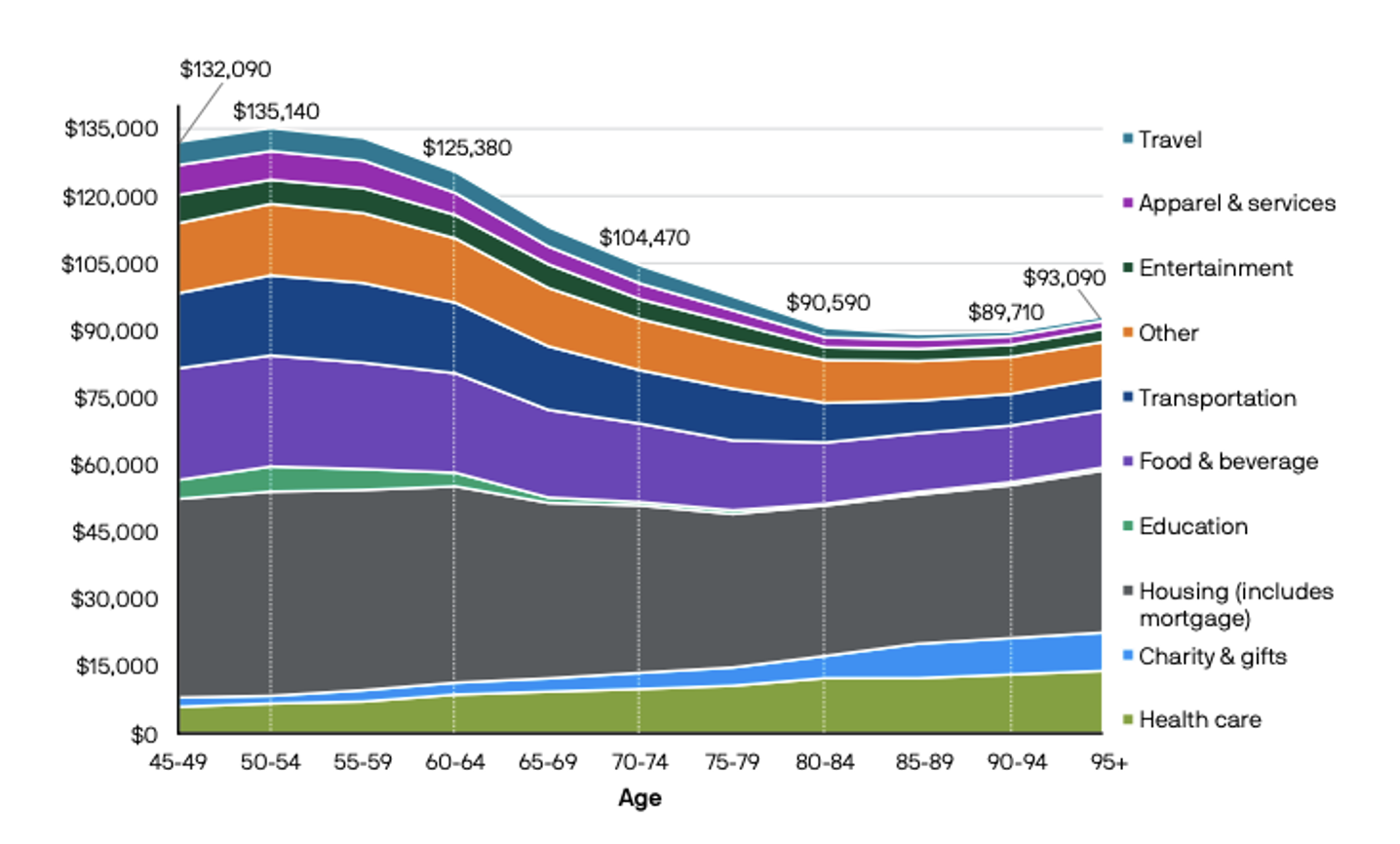

Figure 3. Changes in spending: All households with US$1million-US$3million investable wealth

Source: JP Morgan Asset Management.Figure 3., shows that those with a little more in the kitty at retirement also experience (or orchestrate) lower spending as they age.

According to the data, you will spend less tomorrow than you did today.

The Australian experience

According to the Grattan Institute’s Savings Behaviour of Older Households, a submission to the Labor government’s Inquiry into the implications of removing refundable franking credits, “Australians tend to spend less after they retire. Even the wealthy eat out less, drink less alcohol and replace clothing and furniture less often. Spending tends to slow at around the age of 70, and decreases rapidly after 80,” with the data probably understating the fall in spending because of survivorship bias.

According to the submission, “This fall in overall spending is mainly a result of lower spending on transport, recreation, food and furnishings. Retirees who own a home tend to have paid off their mortgage by retirement and no longer need to spend money on children or on work-related expenses. Pensioners also spend less due to discounts on council rates, motor vehicle registration, electricity and gas bills, public transport fares, and pharmaceuticals. Public transport concessions apply to all retirees – not just those on the pension. Retirees’ spending also tends to be lower because they have more time, and so cook at home more and eat out less.”

That should provide a little extra comfort. All those studies and calculators helping estimate how much you need for retirement assume you will keep spending the same amount you do today. But experience suggests you won’t.

Conclusion

In addition to the desire to reduce uncertainty, a major concern motivating investors to diversify away from the stock market and consider private credit, is the belief that spending will continue at current rates and inflation will cause spending to rise. JPMorgan’s research suggests we exaggerate those concerns.

We also can’t know if or when the stock market will crash, and given that stocks still tend to be a significant part of a conventional portfolio, such an event during retirement can have a material impact on our mindset, forcing us to be frugal, irrespective of what JPMorgan’s data implies.

Rebalancing our portfolios away from stocks as we age, and towards high quality private credit could help reduce the volatility of our returns, and the reality is we are likely to spend less anyway.

In any case, financial solutions, including private credit, now exist which can potentially help ease our retirement concerns, whether we choose to spend less or spend more.

For more information about private credit funds, speak to David Buckland or Rhodri Taylor at Montgomery Investment Management on (02) 8046 5000, or email: investor@montinvest.com

Disclaimer:

You should read the relevant Product Disclosure Statement (PDS) or Information Memorandum (IM) before deciding to acquire any investment products.

Past performance is not a reliable indicator of future performance. Returns are not guaranteed and so the value of an investment may rise or fall.

This information is provided by Montgomery Investment Management Pty Ltd (ACN 139 161 701 | AFSL 354564) (Montgomery) as authorised distributor of the Aura Core Income Fund (ARSN 658 462 652) (Fund). As authorised distributor, Montgomery is entitled to earn distribution fees paid by the investment manager and may be issued equity in the investment manager or entities associated with the investment manager.

The Aura Core Income Fund (ARSN 658 462 652)(Fund) is issued by One Managed Investment Funds Limited (ACN 117 400 987 | AFSL 297042) (OMIFL) as responsible entity for the Fund. Aura Credit Holdings Pty Ltd (ACN 656 261 200) (ACH) is the investment manager of the Fund and operates as a Corporate Authorised Representative (CAR 1297296) of Aura Capital Pty Ltd (ACN 143 700 887 | AFSL 366230).

You should obtain and carefully consider the Product Disclosure Statement (PDS) and Target Market Determination (TMD) for the Aura Core Income Fund before making any decision about whether to acquire or continue to hold an interest in the Fund. Applications for units in the Fund can only be made through the online application form that accompanies the PDS. The PDS, TMD, continuous disclosure notices and relevant application form may be obtained from www.oneinvestment.com.au/auracoreincomefund or from Montgomery.

The Aura Private Credit Income Fund is an unregistered managed investment scheme for wholesale clients only and is issued under an Information Memorandum by Aura Funds Management Pty Ltd (ABN 96 607 158 814, Authorised Representative No. 1233893 of Aura Capital Pty Ltd AFSL No. 366 230, ABN 48 143 700 887).

Any financial product advice given is of a general nature only. The information has been provided without taking into account the investment objectives, financial situation or needs of any particular investor. Therefore, before acting on the information contained in this report you should seek professional advice and consider whether the information is appropriate in light of your objectives, financial situation and needs.

Montgomery, ACH and OMIFL do not guarantee the performance of the Fund, the repayment of any capital or any rate of return. Investing in any financial product is subject to investment risk including possible loss. Past performance is not a reliable indicator of future performance. Information in this report may be based on information provided by third parties that may not have been verified.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.