Are Tech Stocks warning you to rebalance your portfolio?

How do you produce a ball of wool? Pull on the thread of a woollen jumper! What was once a fine, handmade piece of clothing can quickly become a jumbled mess on the floor, and all one has to do is pull on the thread.

I wonder whether that’s a fitting metaphor for what’s going on in equity markets right now.

Many are spinning (pun intended) a view that the rotation of money from tech stocks to elsewhere is a natural progression of the boom – a broadening, if you will, of the bull market.

The alternative view questions whether the selloff, which began in bitcoin and is now spreading to U.S. technology stocks, signals the beginning of a major unwinding of risk that could leave the entire stock market in disarray.

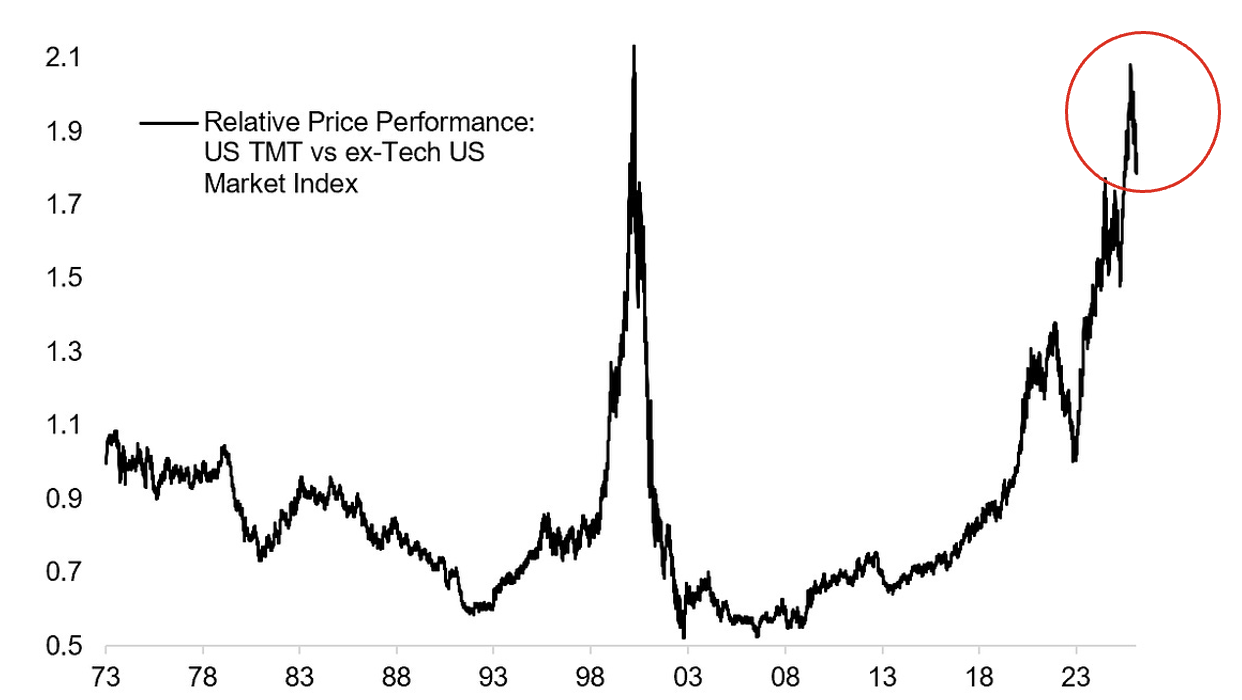

Figure 1. Relative price: U.S. tech vs non-tech.

Source: Topdown Charts, LSEG

As Figure 1., reveals, on a relative basis, it appears U.S. technology stocks have not only peaked but have broken sharply lower vs non-tech stocks, an echo of the shift that occurred prior to the Tech Wreck that began in 2000 and endured until 2003.

Tides are turning: contagion

For years, we at Montgomery Investment Management have emphasised the importance of quality and intrinsic value, the perils of speculation, and the ultimate truth that price eventually follows that value. Mesmerised, however, by the seemingly endless share price ascent of companies with mere hope, few assets and little to no underlying earnings, investors scoffed at the antiquated notion of quality and intrinsic value.

But now, the tides of easy money are receding. The largesse of unconventional monetary policy is giving way to the votes of a younger generation that wants to see wealth redistributed from the Baby Boomers and Generation X through higher taxes and fiscal policy. In turn, the era of ultra-low inflation and the accompanying ultra-low interest rates may also be ending.

What worked for the last two decades may not serve investors well in the next decade.

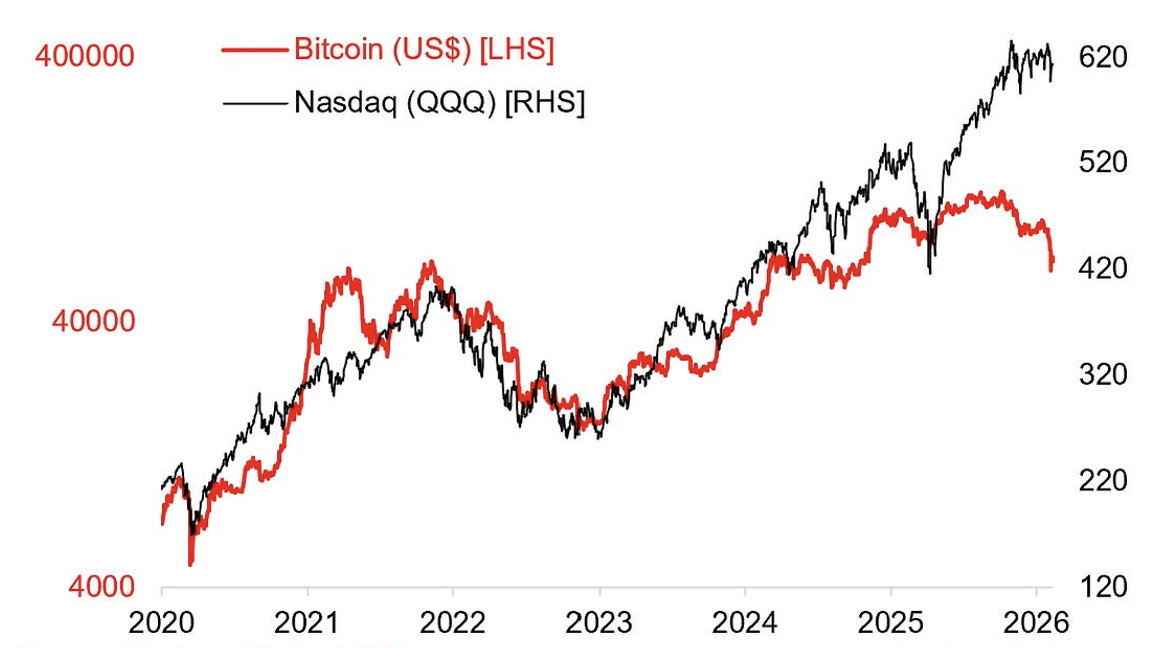

As Figure 2., reveals, we may be witnessing the unsettling beginning of what could be a great unwinding of risk, threatening to derail the retirement plans of countless investors.

Figure 2. Speculative retreat: Bitcoin and Nasdaq

Source: Topdown Charts, LSEG

The first canary in the coal mine may be the reversal of the speculative frenzy in cryptocurrencies. While a sufficient number of use cases convince us that cryptocurrencies will play increasing roles in modern society, Bitcoin has experienced another precipitous decline from its most recent euphoric highs.

Now, the contagion appears to be spreading. The seemingly unassailable fortress of U.S. technology stocks, the Software-as-a-Service (SaaS) darlings of the past decade, and now the artificial intelligence (AI) hyperscalers are displaying cracks.

The renowned economist John Maynard Keynes once observed, “Speculators may do no harm as they are bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation. When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.”

Is the AI infrastructure build out a bubble built on the whirlpool of AI speculation? The majority of U.S. Gross Domestic Product (GDP) can now be attributed to AI infrastructure spending, and trillions are being gambled on it. Keynes warns that this is the definition of casino-generated development, and it could lead to debilitating overcapacity that produces another period of creative destruction.

Other markets already outperforming

While the broader market has wobbled, the underperformance of technology stocks relative to their non-technology counterparts could be a warning. The Nasdaq Composite, heavily weighted towards technology, has declined 0.6 per cent year-to-date (YTD), while the Dow Jones Industrial Average has climbed 4.42 per cent. This divergence highlights a shift in investor sentiment, moving away from growth at any price towards more stable, value-oriented companies.

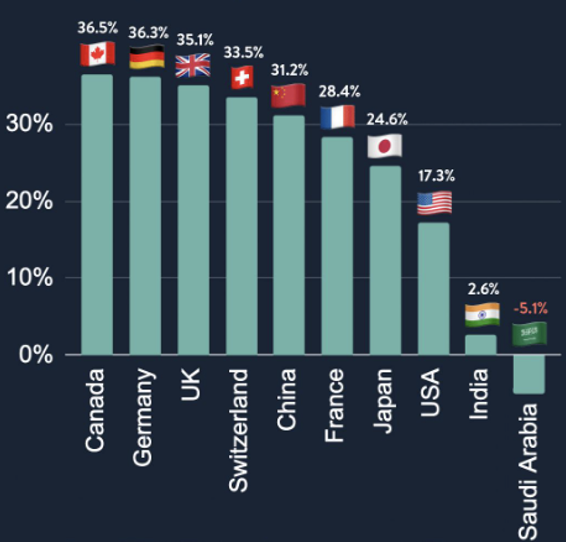

Furthermore, as Figure 3., reveals, a look beyond U.S. borders reveals a similar narrative. While U.S. technology stocks basked in seemingly endless glory, many other global markets, particularly those with a stronger emphasis on tangible assets and traditional industries, have outperformed. This global perspective suggests the recent U.S. Tech volatility isn’t merely a localised or quarantined issue; it’s a potentially systemic recalibration of risk.

Figure 3. 2025 Relative index performance by country

Source: MSCI.org

So, what does this mean for your retirement?

For years, quantitative easing (QE) and historically low interest rates have inflated asset prices across the board, creating an illusion of effortless wealth creation. Many investors, particularly those approaching or in retirement, have become overexposed to risky assets, chasing growth without fully appreciating the underlying risk.

As Benjamin Graham, the father of value investing, sagely noted, in his seminal 1949 book The Intelligent Investor, “The investor’s chief problem – and even his worst enemy – is likely to be himself.” The temptation to follow the crowd, to believe “this time it’s different,” has proven costly throughout history.

The unwinding of this risk, driven by rising inflation and the inevitable normalisation of interest rates, must begin to expose the fragility of portfolios built on shakier foundations. Companies with exorbitant valuations, or priced for certainty, or with little to no profitability, are entering a period of repricing that will ultimately reflect their intrinsic worth – or lack thereof. This process, while painful, is necessary for a healthy market.

The challenge for retirees and those nearing retirement is immense. A significant drawdown in a portfolio at this stage of life can have serious long-term consequences, eroding years of accumulated savings and potentially forcing a drastic reduction in living standards. It’s not merely a paper loss; it’s a very real threat to financial independence.

At Montgomery Investment Management, we believe in prudent, long-term investing based on a thorough understanding of a company’s intrinsic value. This “great unwinding” is not a time for panic, but a time for serious reflection and, for many, a necessary portfolio reassessment.

Have you critically assessed the genuine value of your holdings? Are you overexposed to speculative assets? Is your portfolio sufficiently diversified and resilient to withstand market turbulence in the months and years ahead?

The future remains uncertain, but one thing is clear: the era of easy money, financial tailwinds and effortless gains is ending. Those who have diligently built portfolios based on sound fundamental principles of Goal Setting, Strategic Asset Allocation, Diversification, Risk Management and regular Rebalancing will likely weather the next storm far better than those who succumbed to the siren song of speculation.

If it’s time to ensure your retirement funds aren’t among those caught adrift, speak to Rhodri Taylor or David Buckland about Montgomery’s diversification options on (02) 8046 5000 or by entering your information below:

Disclaimer:

You should read the relevant Product Disclosure Statement (PDS) or Information Memorandum (IM) before deciding to acquire any investment products.

Past performance is not a reliable indicator of future performance. Returns are not guaranteed and so the value of an investment may rise or fall.

This information is provided by Montgomery Investment Management Pty Ltd (ACN 139 161 701 | AFSL 354564) (Montgomery) as authorised distributor of the Aura Core Income Fund (ARSN 658 462 652) (Fund). As authorised distributor, Montgomery is entitled to earn distribution fees paid by the investment manager and may be issued equity in the investment manager or entities associated with the investment manager.

The Aura Core Income Fund (ARSN 658 462 652)(Fund) is issued by One Managed Investment Funds Limited (ACN 117 400 987 | AFSL 297042) (OMIFL) as responsible entity for the Fund. Aura Credit Holdings Pty Ltd (ACN 656 261 200) (ACH) is the investment manager of the Fund and operates as a Corporate Authorised Representative (CAR 1297296) of Aura Capital Pty Ltd (ACN 143 700 887 | AFSL 366230).

You should obtain and carefully consider the Product Disclosure Statement (PDS) and Target Market Determination (TMD) for the Aura Core Income Fund before making any decision about whether to acquire or continue to hold an interest in the Fund. Applications for units in the Fund can only be made through the online application form that accompanies the PDS. The PDS, TMD, continuous disclosure notices and relevant application form may be obtained from www.oneinvestment.com.au/auracoreincomefund or from Montgomery.

The Aura Private Credit Income Fund is an unregistered managed investment scheme for wholesale clients only and is issued under an Information Memorandum by Aura Funds Management Pty Ltd (ABN 96 607 158 814, Authorised Representative No. 1233893 of Aura Capital Pty Ltd AFSL No. 366 230, ABN 48 143 700 887).

Any financial product advice given is of a general nature only. The information has been provided without taking into account the investment objectives, financial situation or needs of any particular investor. Therefore, before acting on the information contained in this report you should seek professional advice and consider whether the information is appropriate in light of your objectives, financial situation and needs.

Montgomery, ACH and OMIFL do not guarantee the performance of the Fund, the repayment of any capital or any rate of return. Investing in any financial product is subject to investment risk including possible loss. Past performance is not a reliable indicator of future performance. Information in this report may be based on information provided by third parties that may not have been verified.

Disclaimer:

The Digital Income Fund is available for wholesale investors only.

Performance of the Digital Income Fund – Digital Asset Class since its inception on 1 May 2021. Net returns after fees and expenses as at 31 January 2026 and assumes reinvestment of distributions.

This is general information and doesn’t take your personal circumstances into account, so seek independent advice before investing. Investing involves risk, including the possible loss of principal. Past performance is not a reliable indicator of future performance.

Diversification does not ensure a profit nor guarantee against a loss. Montgomery Investment Management holds AFSL number 354564.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.