The piano accordion of business life

Business is like a piano accordion. Sectors and individual companies expand and grow, then contract, necessarily becoming smaller than they once were. If you keep this metaphor in mind when investing, it can help you understand the business’s stage of life.

There are exceptions, of course – those businesses that rise above the cycle of invention, adoption, scale, saturation, disruption and destruction, but they are few and far between. Most will eventually reach a natural limit to their size, and then they either sit there, churning customers for lower margins, or are disrupted, or their customers move on to the next trend.

Table 1. Typical life cycle

| Stage | Key Characteristics |

| Invention | High R&D, negative cash flow, and “The Pivot.” This is the spark of a new solution. |

| Adoption | Early adopters sign on. Market fit is proven. Growth is exponential but messy. |

| Scale | The business optimizes its operations to capture the mass market. Efficiency and market share are the primary goals. |

| Saturation | Almost everyone who wants the product has it. Growth slows, and the company often shifts toward defending its position and maximizing dividends. |

| Disruption | A new Invention rises, possibly offering a better or cheaper solution or alternative. The incumbent loses relevance. |

| Destruction | The business fails to pivot, is acquired for parts, or fades into obsolescence. |

Technology, Luxury Fashion, Media, and more – all of these sectors have experienced the piano accordion of life.

Accordion expansion

Back in 2021, LVMH was riding a wave of popularity for its many (now 75) brands, which include Louise Vuitton, Veuve Clicquot, Dior, Fendi, Givenchy, Rimowa, Off-White, Tiffany, Hublot, TAG Heur, Bulgari, Sephora, Ruinart, Château d’Yquem, Moncler (indirectly) and many more.

Back in 2021, if you’d strolled along the Champs-Elysees in Paris towards the Arc de Triomphe, you would have passed the famous Louis Vuitton store and outside, every day, forming a neat line, you’d see several hundred Chinese nationals waiting patiently to enter.

While many in the queue were there to avoid the ‘fakes’ back home, 2021 was also a time when conspicuous consumption of luxury goods amongst the wealthy Chinese was on a strongly rising trajectory.

Back then, the luxury sector was expected to record organic sales growth of 24 per cent, implying a full recovery to 2019 levels thanks to the rise of the “Global Affluent” – those with greater than US$62,000 of annual household disposable income, and the “Affluent” – those with US$46,000 to US$62,000.

In 2021, the number of “Global Affluent” and “Affluent” in China was expected to jump 15 fold from 4 million in 2010 to 60 million in 2030. And with high barriers to entry, few digital threats and onerous store rents, it was concluded the strong brands were likely to get stronger.

Consequently, between the end of 2019 and mid 2023, LVMH’s share price rose 117 per cent.

But a store on every street corner is not luxury, and eventually, as LVMH scaled up – rolling out an ever-expanding parade of luxury boutiques – customers cotton on.

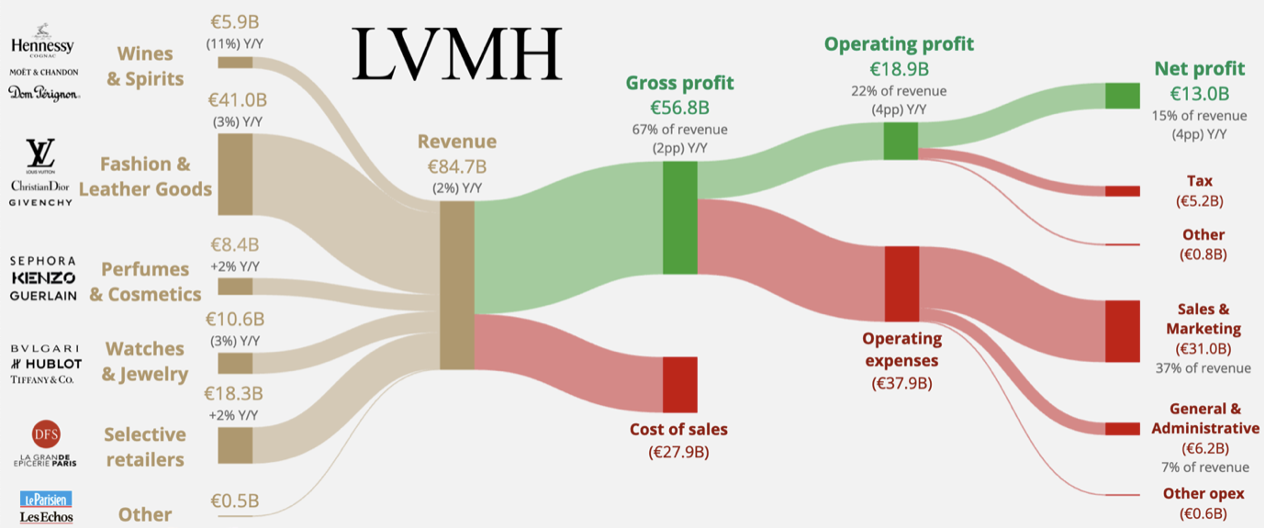

Figure 1. History: LVMH 2024 income statement

Source: App Economy Insights

LVMH’s customers can be divided into three segments. The first is the Entry Level or Occasional customer. They buy one product, usually cosmetics, perfumes or small leather goods. This is LVMH’s highest volume customer segment.

The next segment buys 2-3 products. They’re a smaller segment combining a “classic” piece with accessories or items from another LVMH brand.

The third category are the Very Important Clients – the high frequency, high spending customers buying four or more products.

Each category is populated by fewer and fewer people. There are plenty of people who own one Ferrari, there are a few who have collected 20 or more.

Of course, LVMH segments its customers by a much broader range of characteristics, including demographic (wealth and age), Psychographic (Icon collectors and Stealth Wealthers), Behavioural (frequent and occasional/gift shoppers) and Geographic, but the important thing to note is that eventually each customer reaches a saturation point or they age and simply spend less.

At some point, a company hits a ceiling on the number of customers it will ever reach. Sure, younger generations come through, but unless there are more than in the earlier demographic, the total number of customers flatlines, and the company is forced to spend more to attract the next customer or keep the existing one.

Meanwhile, trends change.

In 2024 LVMH’s revenue declined by €1.5 billion from €86.2 billion to €84.7 billion. In 2025, revenue declined by another €4.7 billion to €80.8 billion.

Accordion contraction

This year, many news outlets are reporting the decade-long era of explosive, logo-driven luxury growth in China has come to an end.

Instead, a sophisticated “pingti” (substitute/dupe) culture has developed among Gen Z consumers there. And it doesn’t seem like the shift is temporary or a response to economic belt-tightening. Instead, it appears to be a cultural shift where savvy shopping becomes the new status symbol, replacing brand prestige.

The consequences for global luxury conglomerates are already being felt. China’s luxury market – once a third of global sales – reportedly contracted 18 per cent to 20 per cent in 2024.

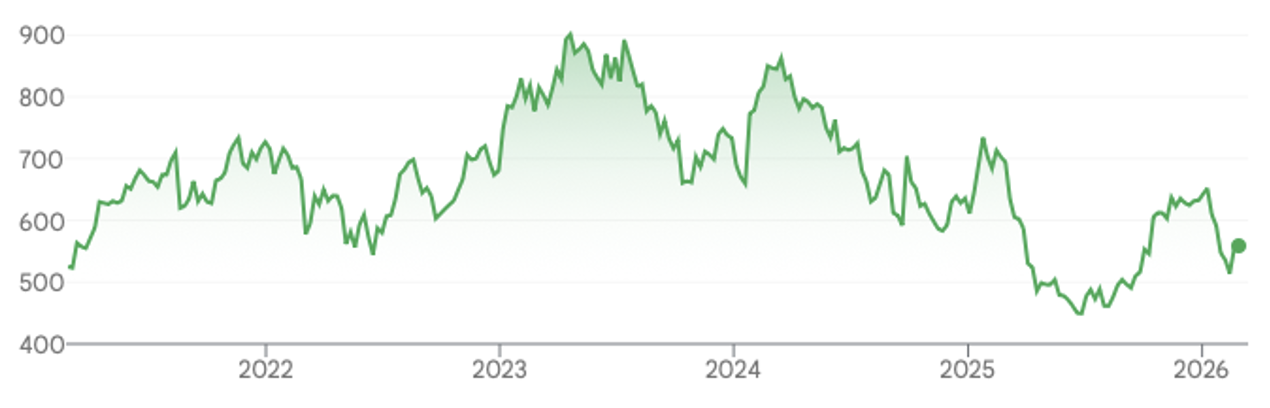

Figure 2. LVMH Share price (€)

Source: Google Finance

Key Share price impacts:

- LVMH: Stock down ~30 per cent from its 2023 peak.

- Kering (Gucci): Stock down circa 60 pe cent since 2021.

- Burberry: Brand value dropped $2.0 billion in 2024; removed from the FTSE 100.

- Estée Lauder: Stock down 70 per cent as sales reached 2020 lows.

The social media-driven “Pingti” phenomenon is unlike traditional “trading down”. Instead, the movement is driven, for example, by consumers actively researching original equipment manufacturers (OEMs) to find products made in the same factories as luxury brands (e.g., Sitoy Group, which produces $100 bags identical to $1,000 Prada/Michael Kors items). Meanwhile, domestic brands are using a “performance benchmarking” strategy to offer high-end specs at a fraction of the cost (e.g., Laifen hair dryers priced at 20 per cent of Dyson’s retail cost), and for many Chinese Gen Z’ers, the social media celebs aren’t those unwrapping an iconic Louis Vuitton bag for the world to see, but those finding a high-quality Chinese alternative manufactured and marketed by brands like Florasis, Li Ning, Anta and Laopu Gold.

Call it disruption, call it a cycle, or call it structural, but either way, I wonder whether, for LVMH and its peers, the accordion has completed its contraction. Will LVMH investors regret the company’s expansion in China? If the contraction is over, the stock could be cheap, but if LVMH has already reached its maximum customer base, it may have already reached its maximum market capitalisation.

Roger Montgomery is the Founder and Chairman of Montgomery Investment Management. Roger has over three decades of experience in funds management and related activities, including equities analysis, equity and derivatives strategy, trading and stockbroking. Prior to establishing Montgomery, Roger held positions at Ord Minnett Jardine Fleming, BT (Australia) Limited and Merrill Lynch.

He is also author of best-selling investment guide-book for the stock market, Value.able – how to value the best stocks and buy them for less than they are worth.

Roger appears regularly on television and radio, and in the press, including ABC radio and TV, The Australian and Ausbiz. View upcoming media appearances.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.