Just how bad will the consumption slowdown be?

Continuing to explore the breadth of the expected slowdown in consumption, granular analysis of the Australian Prudential Regulatory Authority (APRA) monthly deposits and the RBA’s October 2022 Financial Stability Review, the following data is worth highlighting.

In late-2022 Australian household deposits were $175 billion above trend, and this “extra cash” was largely in the hands of the 55+ years of age, especially in the hands of the 65+ years of age cohort. After many years of financial repression, these older Australians will enjoy earning a more reasonable return on their spare cash.

30 per cent of variable-rate borrowers would deplete their liquidity buffer by the June 2023 quarter while a further 15 per cent of variable-rate borrowers would deplete their liquidity buffer eighteen months later, by the December 2024 quarter.

Despite some wealth transfer from the cohort in point 1 above to the cohort in point 2 above, the looming household cashflow crunch is expected to sharply slow consumption from mid-2023, especially when we consider the likelihood of two more increases in the RBA official cash rate to 3.85 per cent in the near-term.

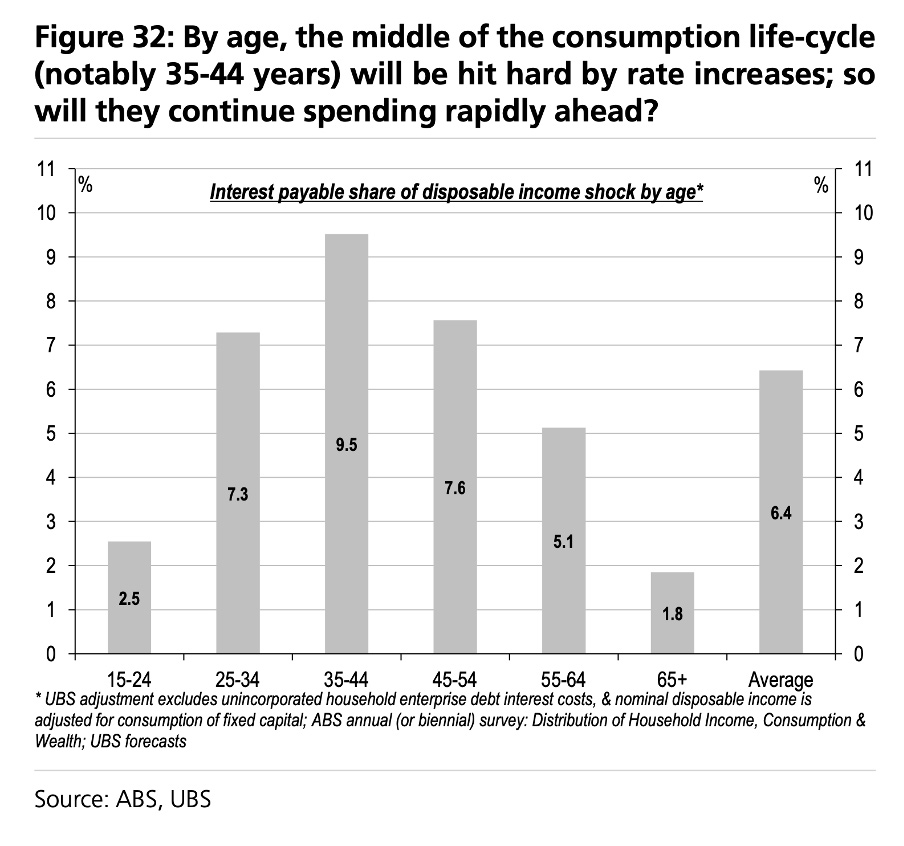

Beware of those businesses most vulnerable to the over-leveraged middle-aged (think 25-44 years of age) households, who account for one-third of total consumption. Think debt to income ratio of 2.3X for the 25-34 cohort, 3.0X for the 35-44 cohort and 2.3X for the 45-54 cohort, and a typical interest payable share of disposable income shock approaching 10 per cent.

Positioning investors’ portfolios for rising cost-of living and interest rate pressures is complex, especially when analysing companies in various sub-sectors, such as grocery, liquor, electronics, household goods, hardware, fashion, discretionary retail and service. We note that where consumer confidence has persisted at similar levels to today (1986, 1989 and 2008), volume growth has, on average, slowed from 4 per cent per annum to around nil.

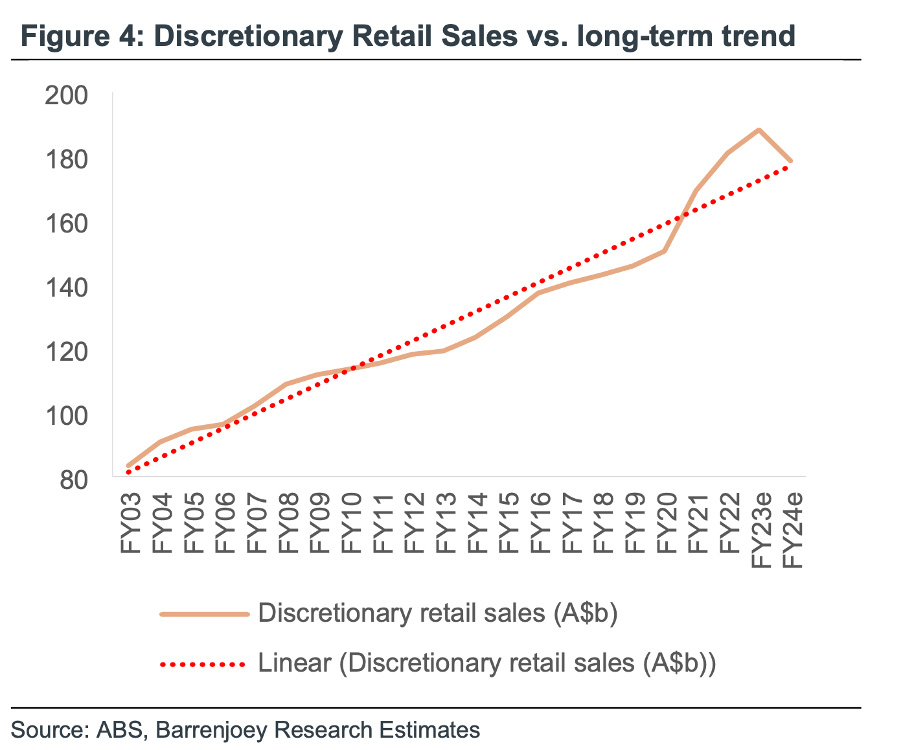

As discretionary retail sales decline below the long-term trend, as per the graph below, earnings in the year to June 2024 for the most exposed of the “discretionary spending” companies are likely to come under pressure. Examples of the more vulnerable companies include Adairs (ASX: ADH), Universal Store (ASX: UNI) and Harvey Norman (ASX: HVN).

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.