Australian consumer confidence to bounce from 54-year low – debt tells the story

In late March 2026, the ANZ Roy Morgan Australian Consumer Confidence Index hit the lowest level since the survey began in the early 1970s.

Last week (5 April 2026), it rallied to the second worst week on record, as motorists received a $0.26 per litre reduction in the fuel excise. And this week, I’m confident it will rally further on the back of the provisional ceasefire between the USA and Iran and the announcement of the reopening of the Strait of Hormuz.

What I find strange is that given the Australian economy has been in far more pain in periods such as, the early 1990s, then why are we recently setting record lows in domestic consumer confidence?

After all, readers around my age or older will remember the Reserve Bank of Australia (RBA) cash rate hitting 17.5 per cent in January 1990. After two 0.25 percentage point cash rate increases in the past two months (to 3.85 per cent on 4 February 2026 and then a further increase on 18 March 2026), the current RBA cash rate is now only 4.1 per cent.

Further, unemployment hit 11.2 per cent in December 1992, and this compares with the current relatively low unemployment rate of 4.3 per cent.

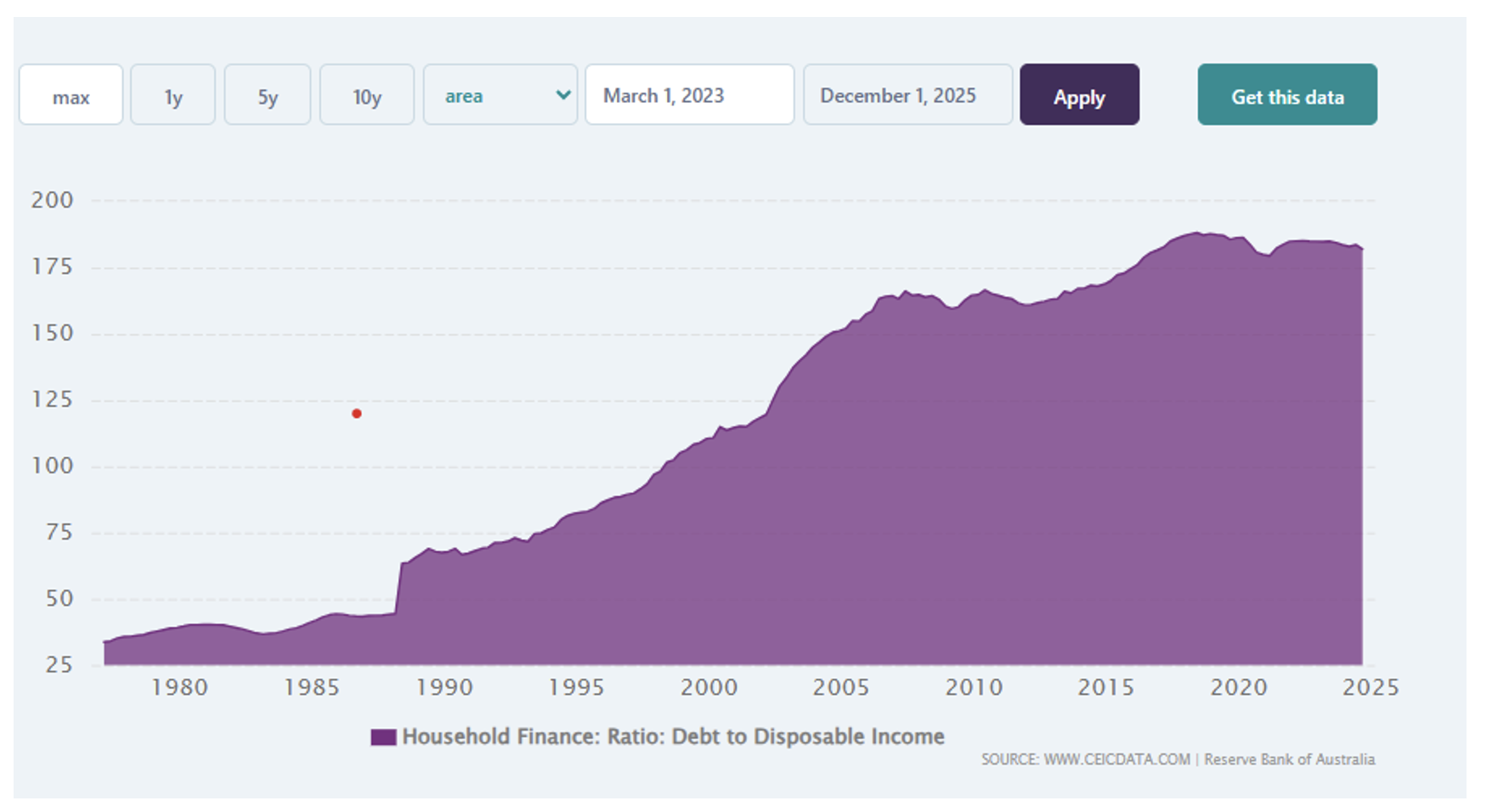

The answer to this conundrum, given cash rates are around one-quarter of the level in 1990, and unemployment is around one-third of the level of 1992, is debt. That is, the Australian household debt to disposable income ratio has effectively quadrupled over the past 50 years from around 45 per cent to 180 per cent.

In short, the average householder had $0.45 of debt for every $1.00 of disposable income. Now we have close to $1.80 of debt for $1.00 of disposable income. We no longer wait for dad to say, “we will get a new colour television when I can afford it” to “let’s put that on the credit card”.

We no longer pay three times pre-tax earnings to purchase a home, but 8 to15 times instead. And the stress attributable to paying over 30 per cent of disposable income on rent, particularly in areas where the vacancy rate is sub 1.5 per cent, and/or paying 10 per cent of disposable income on energy means we have a society in pain.

And with such a highly indebted consumer, we don’t need many external shocks for consumer confidence to take a further beating.

Australia’s household finance: Ratio: Debt to disposable income from March 1977 to December 2025

Source: www.ceicdata.com Reserve Bank of Australia

Chief Executive Officer of Montgomery Investment Management, David Buckland has over 40 years of industry experience.

David is a deeply knowledgeable and highly experienced financial services executive. Prior to joining Montgomery in 2012, David was CEO and Executive Director of Hunter Hall for 11 years, as well as a Director at JP Morgan in Sydney and London for eight years.

This post was contributed by a representative of Montgomery Investment Management Pty Limited (AFSL No. 354564). The principal purpose of this post is to provide factual information and not provide financial product advice. Additionally, the information provided is not intended to provide any recommendation or opinion about any financial product. Any commentary and statements of opinion however may contain general advice only that is prepared without taking into account your personal objectives, financial circumstances or needs. Because of this, before acting on any of the information provided, you should always consider its appropriateness in light of your personal objectives, financial circumstances and needs and should consider seeking independent advice from a financial advisor if necessary before making any decisions. This post specifically excludes personal advice.